登錄

選單

登錄

海擇短評 Haize Comment:

近期第三方APP數據服務商data.ai發布總結2023年的"移動市場報告",有部分數據值得參考與借鑑,海擇資本整理如下:

1. 全球應用商店進入"準存量爭奪"年代。根據其調研,2023年,全球應用商店的用戶支出和企業的廣告移動支出分別為1,710億美元與3,620億美元,雖然再創歷史新高,但YoY僅剩3%與8%,相對於2022年時的-2%與14%的年增率,可確認已進入準存量競爭年代。應用下載量統計了iOS、Google Play的數據(中國地區加計了Android數據),成長也不高,全年共2,570億次,YoY增長1%,看來2024年就會下滑,而這部分的數量主要由遊戲帶動,可以理解為其他品類新應用下載變少,更偏向大者恆大。

2. 應用間競爭為"5小時"爭奪戰。在數據調研的TOP 10中,2022年的用戶平均使用時長為5小時2分鐘,比2021年增加3%,比2020年增加9%;而2023年則比2022年增加6%,也就是5小時20分。亦即,平均來看,所有APP主要在爭奪用戶每日5小時左右的使用時長,這部分可能社交、視訊與遊戲佔絕大多數的時間,對新進入業者的拉新獲客挑戰比過去更為艱鉅。

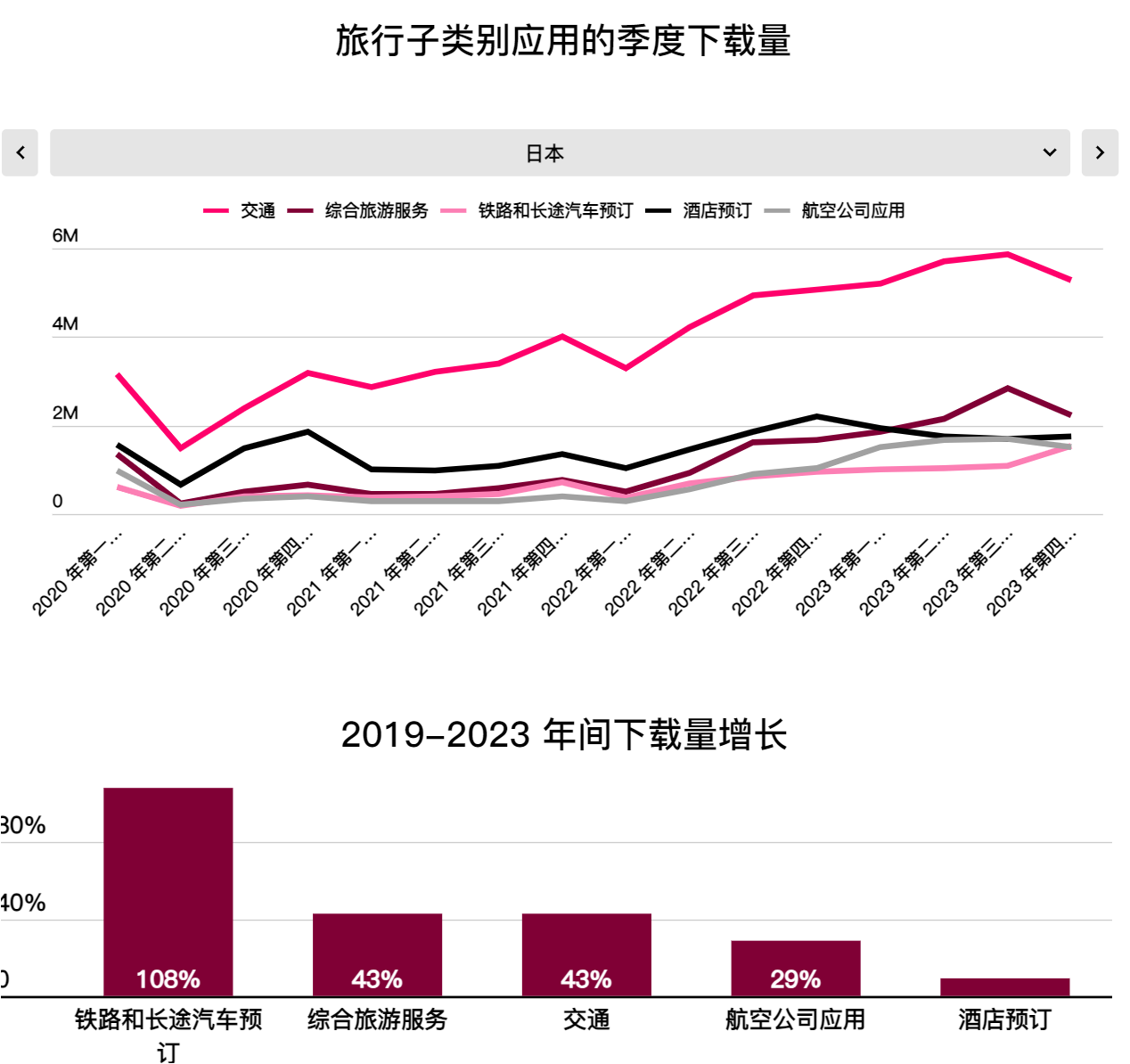

3. 旅遊應用使用時間增速較整體為高。2023年旅行類應用的使用時間與下載量,都遠超於過往,與2020年疫情期低點相比,全球下載量接近翻倍,使用時長增長超85%;與2022年相比,全球下載量增長13%,使用時長增長24%,海擇資本認為,這可以理解為,被壓抑的需求因為各種原因尚未完全釋放,特別是亞洲。從亞洲各公司的財報來看,海擇資本也發現多數公司盈利超過2019年的原因,可能來自於裁員與缺工,而非用戶訂單數超過2019年同期。

4. 交通類應用為各國旅遊用戶下載熱點。疫情間大浪掏沙,讓許多此前重金拉新的旅遊APP成果歸零重練;而後疫情時期盈利重於增長,從結果看,最後能出線只有兩類旅遊應用:網約車、火車這些交通類應用與基於酒店的一站式OTA應用。目前看亞洲,Uber(NYSE: UBER)、Gojek(ID: GOTO)、inDrive、maxim及各國local最強的網約車公司,挾龐大流量,必將成為各品類商戶商務合作的對象,也有能力走向一站式服務;而既有的OTA則恢復國際化征戰,看起來Trip.com(NASDAQ: TCOM)、Traveloka、Klook的發展速度都很快。

----------

data.ai released its "Mobile Market Report" for 2023, highlighting key data for reference and learning, summarized by Hai Ze Capital as follows:

1. The global app store has entered an era of quasi "fight for existing resources". According to the report, in 2023, global app store user spending and corporate mobile advertising expenditures were $171 billion and $362 billion respectively, setting new historical highs. However, the year-over-year (YoY) growth rates were only 3% and 8%, compared to -2% and 14% in 2022, indicating the onset of quasi stock competition. The total number of app downloads, including data from iOS, Google Play, and Android in China, also showed modest growth, totaling 257 billion for the year, a 1% increase YoY. This suggests a potential decline in 2024. Notably, this growth was primarily driven by gaming apps, implying a decrease in new downloads for other categories and a trend towards dominance by larger players.

2. APP competition revolves around a "5-hour" battle for user attention. Research shows that in 2022, the average daily usage time for users was 5 hours and 2 minutes, a 3% increase from 2021 and 9% from 2020. In 2023, this increased by 6% to approximately 5 hours and 20 minutes. Essentially, on average, all apps are competing for around 5 hours of a user's daily attention, with social media, video streaming, and gaming likely dominating most of this time. This presents a significant challenge for new entrants in acquiring and attracting new customers, as the competition is tougher than before.

3. Travel app usage and downloads have grown faster than average. In 2023, the usage time and download volume for travel apps significantly exceeded past figures. Compared to the low during the 2020 pandemic, global downloads nearly doubled, and usage time increased by over 85%. Compared to 2022, global downloads grew by 13%, and usage time by 24%. Haize Capital believes this indicates that suppressed demand has not been fully released yet, especially in Asia. From the financial reports of Asian companies, Haize Capital also notes that many companies' profits exceeded those of 2019, likely due to staff reductions and labor shortages, rather than an increase in user orders compared to the same period in 2019.

4. Transportation apps have become hotspots for tourist downloads in various countries. The pandemic's impact reset many heavily invested travel apps, requiring them to start from scratch. In the post-pandemic era, profitability has become more important than growth. As a result, only two types of travel apps have emerged successfully: transportation apps like ride-sharing and trains, and one-stop OTA apps based on hotels. In Asia, companies like Uber (NYSE: UBER), Gojek (ID: GOTO), inDrive, maxim, and the strongest local ride-sharing companies, with their significant traffic, are poised to become key partners for various merchants and have the potential to offer one-stop services. Existing OTAs are resuming their international expansion. Trip.com (NASDAQ: TCOM), Traveloka, and Klook, for instance, are all developing rapidly.

----------

data.ai는 "2023년 모바일 시장 보고서"를 발표하여 참고할 수 있는 핵심 데이터를 중점적으로 소개했으며, 하이저 캐피털은 다음과 같이 요약했다.

1. 글로벌 앱스토어는 이미 "기존 자원을 쟁탈하는" 시대에 들어섰다. 보고서에 따르면 2023년 전 세계 앱스토어 사용자 지출과 기업 모바일 광고 지출은 각각 1,710억달러와 3,620억달러로 사상 최고치를 기록했다. 그러나 2022년의 -2%와 14%에 비해 연간 성장률은 3%와 8%에 불과하다. 이것은 기존 자원을 쟁탈하는 시대가 시작되었음을 보여준다. iOS, Google Play, Android를 포함한 중국 앱의 총 다운로드 수도 연간 총 2,570억건으로 전년 대비 1%만 증가했다. 이 추세에 따라 2024년에는 감소할 수 있을 것으로 예상된다. 주목할 만한 것은, 이 성장은 주로 게임 앱에 의해 추진되었는데, 이는 다른 카테고리 앱의 다운로드 수가 감소하고 대기업이 주도적인 위치를 차지하고 있다는 것을 의미한다.

2. 앱 경쟁은 "5시간" 사용자의 사용 시간을 쟁탈한 것이다. 연구에 따르면 2022년까지 사용자의 하루 평균 사용 시간은 5시간 2분으로 2021년보다 3%, 2020년보다 9% 증가했다. 이는 2023년까지 약 5시간 20분까지, 6% 증가한 수치다. 기본적으로 모든 앱은 하루 5시간 정도 사용자의 사용 시간을 쟁탈해야 한다. 이 중 소셜미디어, 동영상 스트리밍, 게임이 대부분을 차지했다. 이는 신규 진입자들이 이전보다 경쟁이 치열해졌기 때문에 신규 고객을 확보하고 유치하는 데 중대한 도전을 던졌다.

3. 여행 앱의 사용 시간과 다운로드 증가 속도가 평균 수치보다 높다. 2023년에는 여행 앱의 사용 시간과 다운로드 수가 과거 데이터를 크게 앞질렀다. 2020년 코로나 기간의 저점에 비해 전 세계 다운로드 수는 거의 두 배, 사용 시간은 85% 이상 증가했다. 2022년에 비해 전 세계 다운로드 수는 13%, 사용 시간은 24% 증가했다. 하이저 캐피털은 특히 아시아에서 억제된 수요가 아직 완전히 방출되지 않았음을 보여준다고 보고 있다. 아시아 회사의 실적 발표에서 하이저 캐피털은 또한 많은 회사의 이익이 2019년을 초과했으며, 이는 사용자 주문이 2019년 동기간보다 증가했기 때문이 아니라 감원과 노동력 부족 때문일 수 있다는 점에 주목했다.

4. 교통류 응용은 이미 각국 여행객이 다운로드하는 열점으로 되였다. 코로나의 영향은 거액을 투입한 많은 여행 앱을 재조정하여 제로베이스에서 시작하도록 하였다. 포스트 코로나 시대에는 성장보다 수익성이 더 중요해졌다. 따라서 인터넷 렌트카와 기차와 같은 교통 앱과 호텔 기반의 원스톱 OTA 앱이라는 두 가지 유형의 여행 앱만이 성공적으로 이길 수 있다. 아시아에서 Uber(NYSE: UBER), Gojek(ID: GOTO), inDrive, maxim 등 회사와 현지에서 가장 강력한 인터넷 렌트카 회사는 방대한 트래픽으로 각 사업자의 중요한 파트너가 될 것이며 원스톱 서비스를 제공할 잠재력이 있다. 기존 온라인 여행사들은 국제적 확장을 회복하고 있다. 예를 들어, Trip.com(NASDAQ: TCOM), Traveloka, Klook은 빠르게 성장하고 있다.

標籤 Label: data.ai App Travel Transport NYSE: UBER NASDAQ: TCOM