登錄

選單

登錄

海擇短評 Haize Comment:

財報月總是不缺市值暴漲暴跌的公司,本次美國旅遊上市公司中的暴跌代表如果是Sabre,那麼暴漲的代表無疑就是Tripadvisor(NASDAQ: TRIP)。Tripadvisor在公告2023Q4與2023全年財報前後,市值最高增長23.4%,總市值達38.9億美元,創下2022年3月以來新高。市值飆漲的主因,來自Tripadvisor公告成立特別委員會,評估控股股東Liberty TripAdvisor Holdings(LTRPA.PK)將可能被收購的相關提案,由於其持有Tripadvisor的56%股份,收購Liberty TripAdvisor Holdings將可能會同時導致收購Tripadvisor的交易。收購歸收購,但是什麼樣的估值模型能給到Tripadvisor高溢價,這只能從其財報中解讀一二。

首先,從淡季的角度來看,Tripadvisor確實有個不錯的Q4,其總收入3.9億美金創歷史Q4新高,不過Adjusted EBITDA則僅創下疫情以來的Q4新高。但值得注意的是,無論是收入或EBITDA,帶動增長的產品線都不是來自酒店,Tripadvisor來自平台的收入2.18億美金,雖然也創下Q4新高,但住宿部分貢獻的收入僅1.35億美金,仍低於2019年的1.55億美金,官方的說法是競爭激烈導致。總計本期Tripadvisor的收入,已有2.38億美元與玩樂體驗及餐飲相關,若與住宿部分的1.35億美金相比,超過約75%,更像是Tripadvisor的本業。也因此,2023年下半年以來,Tripadvisor的品牌宣傳語(Slogan)已經從"We are a global travel guidance company(全球旅遊指南)"改為"The world’s most trusted source for travel and experiences(世界上最值得信賴的旅行和體驗資源)",更強調了體驗類產品,同時也淡化了內容網站的色彩。

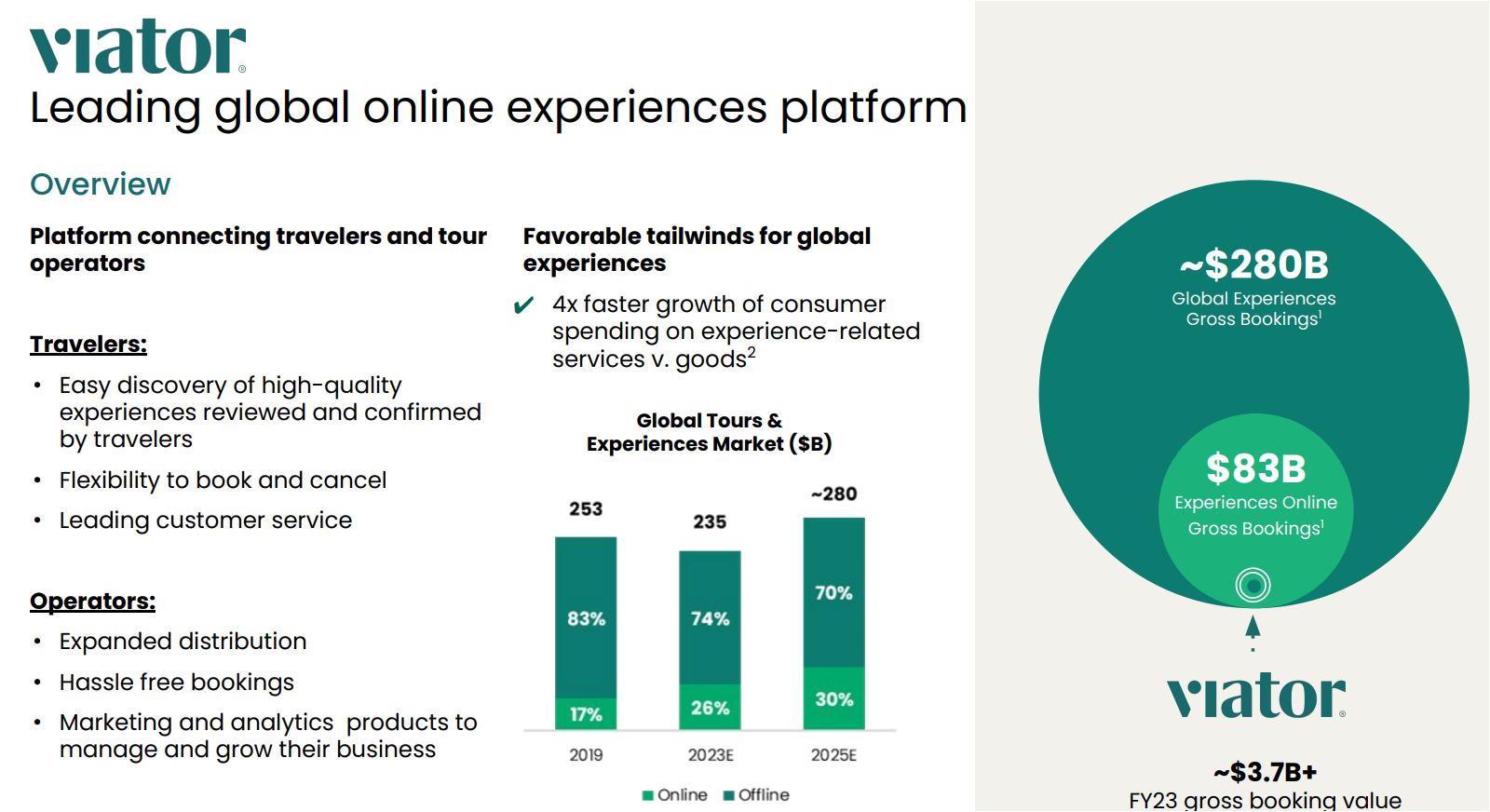

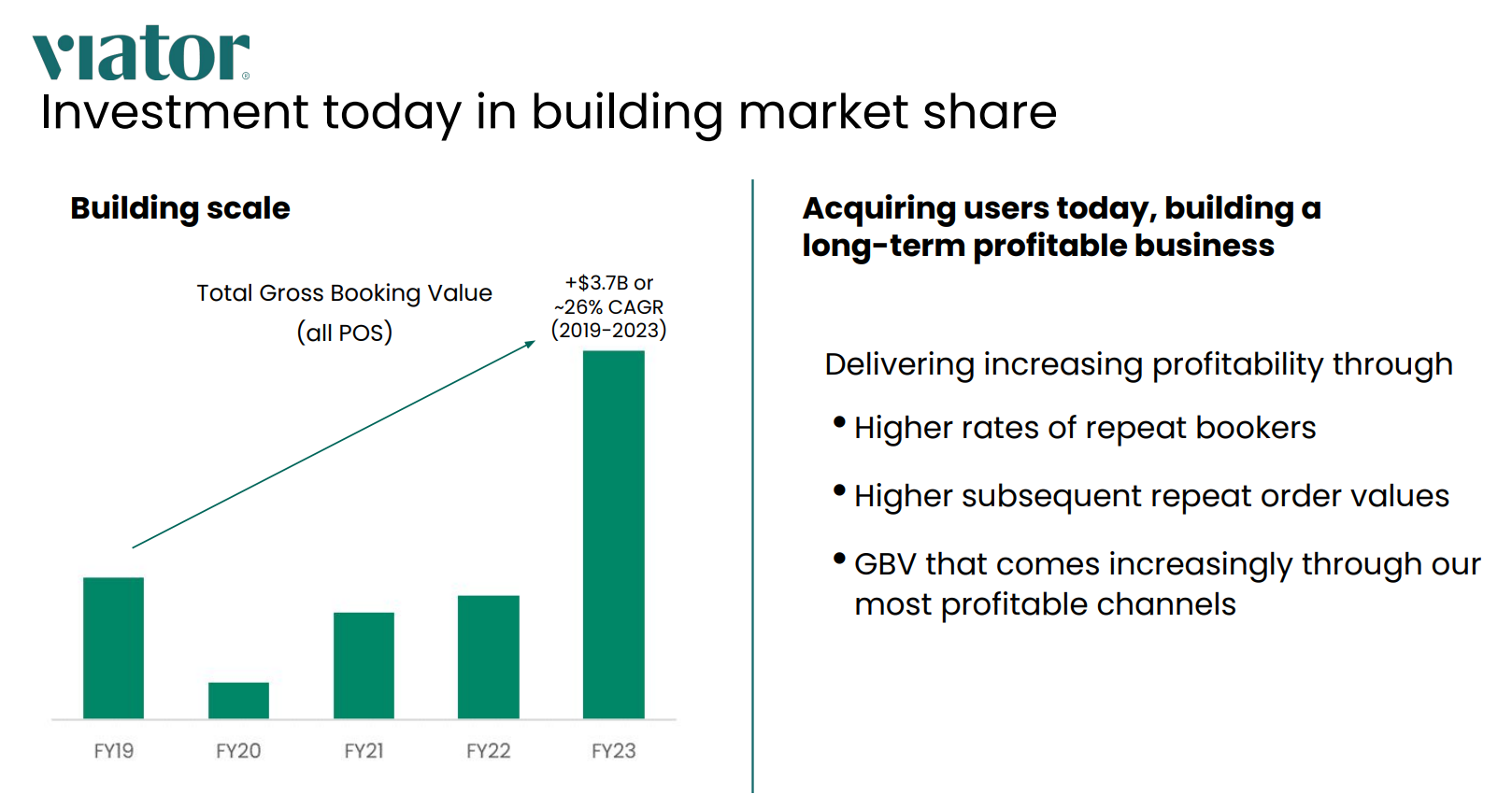

海擇資本認為,投資人對Tripadvisor的估值模型雖然不得而知,但明顯玩樂體驗領域是很重要的一部分。按照其說法,玩樂體驗領域擁有廣大的潛在市場,在2025年市場總值將達2,800億美金,而其中線上市場的占比將達到30%。而在市場的競爭格局中,Tripadvisor旗下的Viator具有高度優勢,從財務表現來看,其2023年交易額達37億美金,YoY增長約2X;全年收入達7.37億美金,YoY增長49%;若從Adjusted EBITDA看,Q4盈利1,500 萬美金,全年已損益兩平。

在當前的地緣政治態勢下,真正能參與競標的買家也許不多,說不定最後還是只有Expedia(NASDAQ: EXPE)有競標到底的能力,這也會影響收購的可能性與市值。影響更大的或許是,Viator在2023年已全年盈利,這意味著各洲際的領先公司如GetYourGuide與Klook,很可能也進入了全年盈利狀態,玩樂體驗或將成為下一個成群走向IPO的旅遊細分領域。

----------

Earnings months always see companies with significant market value increases and decreases. In the case of U.S. listed travel companies, Sabre represents a sharp decline, while Tripadvisor (NASDAQ: TRIP) undoubtedly represents a sharp increase. Before and after announcing its Q4 2023 and full-year 2023 financial results, Tripadvisor's market value peaked at a 23.4% increase, reaching $3.89 billion, the highest since March 2022. The surge in market value is primarily due to Tripadvisor announcing the formation of a special committee to evaluate potential acquisition proposals for its controlling shareholder, Liberty TripAdvisor Holdings (LTRPA.PK), which owns 56% of Tripadvisor. An acquisition of Liberty TripAdvisor Holdings could potentially lead to the acquisition of Tripadvisor. However, the valuation models that justify a premium for Tripadvisor can only be inferred from its financial statements.

From an off-peak perspective, Tripadvisor had a strong Q4, with total revenue reaching a record $390 million for Q4, although its Adjusted EBITDA only hit a post-pandemic high for Q4. Notably, neither revenue nor EBITDA growth was driven by the hotel sector. Tripadvisor's platform revenue was $218 million, a Q4 record, yet accommodation revenue contributed only $135 million, still below the $155 million in 2019, attributed to fierce competition. In total, $238 million of Tripadvisor's revenue was related to experiences and dining, over 75% more than the accommodation segment's $135 million, suggesting that experiences are becoming Tripadvisor's core business. Consequently, since the second half of 2023, Tripadvisor's slogan has changed from "We are a global travel guidance company" to "The world's most trusted source for travel and experiences," emphasizing experiences and moving away from being solely a content website.

Haize Capital believes that while investors may not fully understand the valuation model for Tripadvisor, it's clear that the experience sector is a crucial component. According to them, this sector has a vast potential market, projected to reach a total value of $280 billion by 2025, with the online segment accounting for 30% of this. Within this competitive landscape, Tripadvisor's Viator has a significant advantage. Financially, Viator's 2023 transaction volume reached $3.7 billion, with a year-on-year growth of about 2X; its annual revenue hit $737 million, up 49% year-on-year; and its Adjusted EBITDA showed a Q4 profit of $15 million, achieving breakeven for the year.

Given the current geopolitical climate, there might be few buyers able to compete in a bid, possibly leaving only Expedia (NASDAQ: EXPE) with the capacity to bid to the end, which could affect the acquisition's likelihood and market value. Perhaps more significantly, Viator's profitability throughout 2023 suggests that other leading companies in different continents, like GetYourGuide and Klook, might also have achieved annual profitability, indicating that experiences could become the next travel niche to trend towards IPOs.

----------

각 회사의 실적이 속속 발표됨에 따라 어떤 회사는 시가총액이 증가하고 어떤 회사는 시가총액이 하락하는 것을 볼 수 있다. 예를 들어 미국에 상장된 여행사 중 Sabre의 시가총액은 하락한 반면 Tripadvisor(NASDAQ: TRIP)의 시가총액은 크게 증가했다. 트립어드바이저의 시가총액은 2023년 4분기와 2023년 연간 실적 발표를 전후해 최고 23.4% 증가한 38억9,000만달러로 2022년 3월 이후 가장 높았다. 시가 급등의 주요 원인은 트립어드바이저가 지배주주인 리버티 트립어드바이저 홀딩스(Liberty TripAdvisor Holdings, LTRPA.PK)가 인수될 수 있다는 관련 제안을 평가하기 위한 특별위원회 설립을 발표했기 때문이다. 리버티 트립어드바이저는 트립어드바이저 지분 56%를 보유하고 있다. 리버티 트립어드바이저 홀딩스의 인수는 트립어드바이저의 동시 인수로 이어질 수 있다. 그러나 트립어드바이저 프리미엄의 합리성을 증명하는 평가 모델은 재무제표에서만 추정할 수 있다.

비수기 관점에서 트립어드바이저는 4분기에 강세를 보여 총수입이 기록적인 3억 9천만 달러에 달했다. 비록 그 Adjusted EBITDA는 4분기에 코로나 발생 후 최고치를 기록하는 데 그쳤다. 특히 영업수익과 EBITDA의 성장은 호텔 부문에서 추진되지 않았다. 트립어드바이저의 플랫폼 수익은 2억1,800만달러로 4분기 신기록을 세웠다. 그러나 경쟁이 치열해 숙박의 수익은 1억3,500만달러에 그쳐 2019년의 1억5,500만달러보다 여전히 낮았다. 트립어드바이저의 총수익 중 2억3,800만달러는 액비티비티와 음식 관련으로 숙박 부문의 1억3,500만달러보다 75% 이상 많다. 이는 액비티비티가 트립어드바이저의 핵심 사업이 되고 있음을 보여준다. 이에 따라 2023년 하반기부터 트립어드바이저의 브랜드 홍보 슬로건은 '우리는 글로벌 여행 가이드 회사입니다(We are a global travel guidance company)'에서 '세계에서 가장 신뢰할 수 있는 여행과 체험의 원천입니다(The world’s most trusted source for travel and experiences)'이 됐다. 상품을 강조하여 더 이상 콘텐츠 사이트가 아니다.

하이저 캐피털은 투자자들이 트립어드바이저의 평가 모델을 완전히 알지 못할 수도 있지만 액비티비티 분야가 중요한 구성 요소라는 것은 분명하다고 생각한다. 그들의 말에 따르면, 이 분야는 2025년까지 총 2,800억달러의 가치가 있을 것으로 예상되는 거대한 잠재 시장을 가지고 있으며, 그 중 온라인 부분이 30%를 차지할 것이다. 경쟁이 치열한 이 환경에서 트립어드바이저의 Viator는 상당한 이점을 가지고 있다. 재무면에서 Viator의 2023년 거래액은 37억달러에 달해 전년 동기 대비 약 2배 증가했다. 그 연간 수익은 7억3,700만달러에 달해 전년 동기 대비 49% 증가했다. Adjusted EBITDA는 4 분기 1,500만달러의 이익을 달성하여 연간 손익 균형을 달성했다.

현재의 지연정치학적 환경을 고려할 때 입찰에 참여할 수있는 구매자는 거의 없을 수 있으며 Expedia(NASDAQ: EXPE)만이 끝까지 입찰 할 수있는 능력이 있을 수 있다. 이는 인수 가능성과 시장 가치에 영향을 미칠 수 있다. 아마도 더 중요한 것은 Viator의 2023 년 연간 수익성이 GetYourGuide와 Klook과 같은 다른 선두 회사들도 연간 이익을 달성했을 수 있음을 보여준다는 것이다. 이는 액비티비티가 다음 IPO로 가는 여행시장이 될 수 있다는것을 보여준다.

標籤 Label: TRIP Viator GetYourGuide Klook Activity Experience Acquisition