登錄

選單

登錄

海擇短評 Haize Comment:

全球最大的OTA平台Booking(NASDAQ: BKNG)近期公告2023Q4年報,同時也給到對2024年的預期。本季運營數據不意外的,多項指標創下歷史Q4新高,全年間夜數也首次破10億間夜;不過更被投資人注意的是,公司罕見的對Q1的間夜數低標給到僅4%的增速預期,令投資人大失所望。無論Booking的成長是否接近了極限,所謂Connected Trip是否能接下下一波的成長動能,歐洲的監管是否更趨嚴謹,其做為世界霸者的影響力與為股東創造投資收益的能力,短中期其實都不會受到影響。

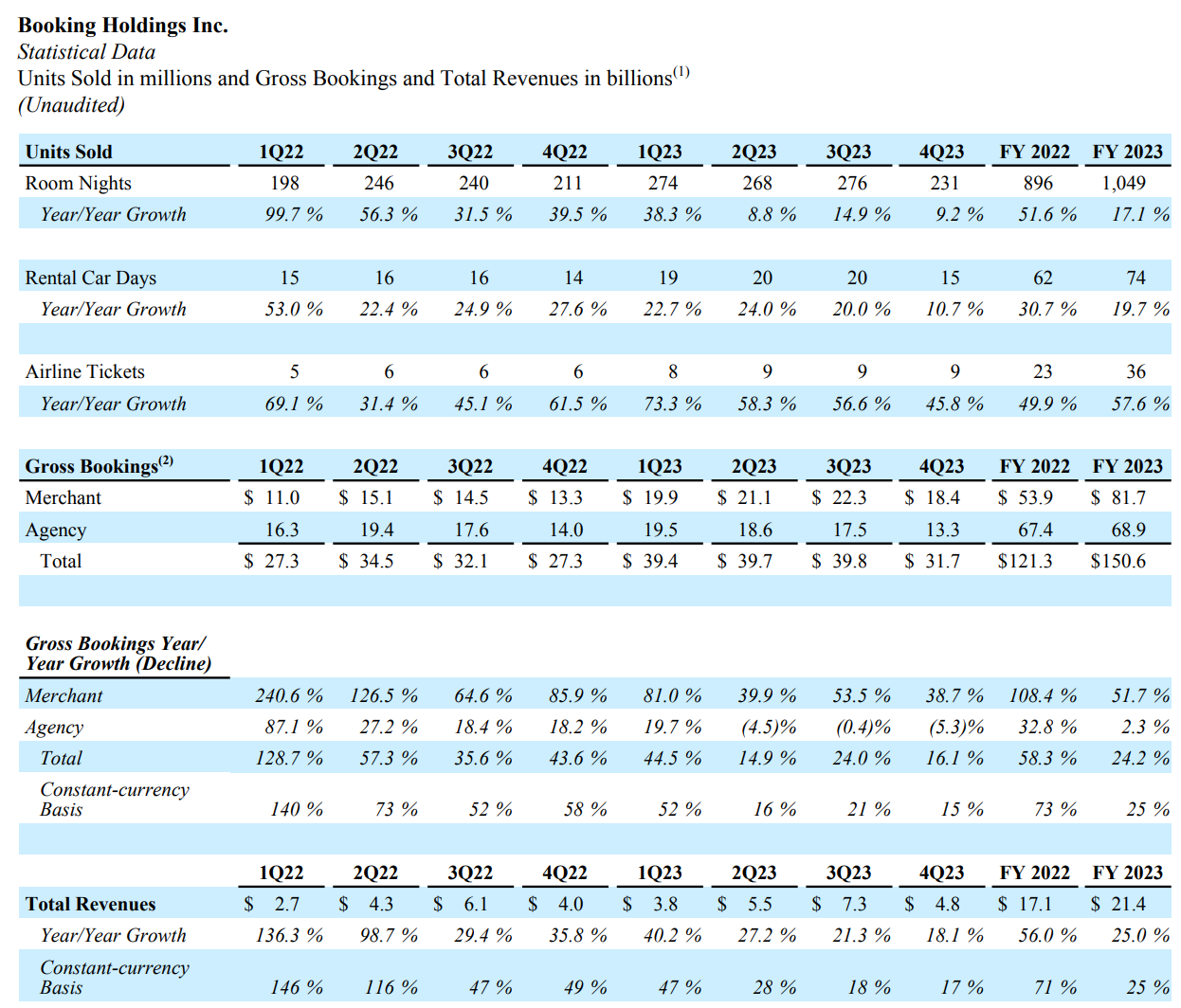

本季Booking的間夜數與交易額分別為2.31億間夜與317億美元,雙雙再創歷史Q4新高,全年間夜數也首次破10億間夜,可說是前無古人,後來者要居上也很不容易。不過,公司所預期今年Q1間夜成長率4%至6%,則是歷史以來首次(疫情期不計)間夜增速可能低於5%,雖然以Booking龐大的間夜基數看,4%的增速也對應著超過1,000萬間夜的絕對值增量,而且盈利預期也不錯,但顯然還是無法緩解市場投資人心中的震撼。

海擇資本認為,從結果看,Booking面對成長極限所外顯的症狀,在於,除了住宿,沒有任何能跟主業並提的第二成長曲線。無論是機票,或是本季電話會議中對Connected Trip更新的定義(保險、景點、租車和其他地面交通產品),住宿本業獨大意味著其他產品要嘛是為了幫住宿事業拉新而存在,要嘛為了"住+X"搭售而存在,公司基於ROI不會考慮建立一個龐大而有全面產品庫的第二本業。但從相反的角度看,即便Booking遇到了成長極限,他的住宿本業依然無比強悍,良好的銷貨能力、對各部門嚴格的ROI要求,讓它能持續取得最優的佣金率與保留房,光是庫存達人Booking加殺價狂人Agoda的輔弼整合,就足以把全球大部分的住宿中介殺得丟盔棄甲,猶如為公司與股東貢獻收益的永動機。

值得好奇的是,Booking在資本市場的策略一直是,給一個相對低的預期,再超越預期得到資本市場肯定,這次還是相同的策略嗎?海擇資本認為,當然不無可能。不過,近期Booking在資本支出上與過往有很大的不同,股票回購Booking一直在做,僅Q4就用了24億美金做股票回購;還安排在3月28日首次派發季度股息紅利每股8.75美元,依Q4季末稀釋後股數推估約3.1億美金;同時,Q4提撥的員工股期權支出還創下了歷史新高,達10.32億美金,依全公司員工21,600人計,平均每人Q4股期權收益就接近4.8萬美金(全年約11.4萬美金),堪稱世界最幸福旅遊公司。這些措施,大體都指出,資本支出沒有其他更必要與更具ROI的運用方式。這其實也沒什麼不好,疫情以來,Booking股價已從1,107美金漲到近期峰值3,918美元歷史新高,漲幅達254%,投資人也沒什麼好不滿意的。

----------

Booking (NASDAQ: BKNG), the world's largest OTA platform, announced its Q4 2023 report, along with expectations for 2024. This quarter's operational data unsurprisingly set new historical highs for Q4, with the annual room nights surpassing 1 billion for the first time. However, investors paid more attention to the company's rare low guidance for Q1 room nights, projecting only a 4% growth rate, which was disappointing. Regardless of whether Booking's growth is nearing its limit, whether the so-called Connected Trip can drive the next wave of growth, or whether European regulations become stricter, its influence as a global leader and its ability to generate investment returns for shareholders are unlikely to be affected in the short to medium term.

This quarter, Booking's room nights and GMV reached 231 million and $31.7 billion respectively, both setting new historical highs for Q4, with the annual number of room nights breaking 1 billion for the first time—a precedent that will be challenging for successors to surpass. However, the company's projected growth rate of 4% to 6% for Q1 room nights marks the first time (excluding the pandemic period) that growth could potentially fall below 5%. Even though a 4% growth means an increase of over 10 million room nights, considering Booking's large base number, and despite positive profit expectations, it still fails to mitigate the shock felt by market investors.

Haize Capital believes that the concern of Booking facing its growth limits is the absence of a secondary growth curve that can match its main business in accommodations. Whether it's flights, or the updated definition of Connected Trip discussed in this quarter's earnings call (insurance, attractions, car rentals, and other ground transportation products), the dominance of the accommodation sector implies that other products exist either to attract new users for accommodations or to be bundled with accommodations in "Stay+X" offers. The company, based on ROI considerations, is unlikely to invest in building a second main business with a vast and comprehensive product portfolio. However, from the opposite perspective, even if Booking has reached a growth limit, its core business in accommodations remains incredibly strong. With excellent sales capabilities and strict ROI requirements for all departments, Booking continues to secure the best commission rates and room stocks. The combination of Booking's inventory with Agoda's pricing strategy is enough to outcompete most global accommodation intermediaries, acting like a perpetual motion machine contributing profits to the company and its shareholders.

Additionally, Booking likes to set a relatively low expectation and then surpass it to gain affirmation from the capital market. Is this the same strategy this time? Haize Capital believes it's certainly possible. However, Booking's recent capital expenditure differs significantly from the past. The company has consistently conducted stock buybacks, spending $2.4 billion on them in Q4 alone; it also plans to distribute its first quarterly dividend of $8.75 per share on March 28, estimated to be about $310 million based on the diluted share count at the end of Q4. Moreover, Q4 saw a record high in employee stock option expenses, reaching $1.032 billion. With 21,600 employees, the average stock option benefit per employee in Q4 is nearly $48,000 (about $114,000 annually), making it arguably the happiest travel company in the world. These measures generally indicate that there are no other necessary or more ROI-effective uses for the capital expenditure. This isn't necessarily a bad thing; since the pandemic, Booking's stock price has risen from $1,107 to a recent peak of $3,918, a 254% increase, leaving investors with little to complain about.

----------

세계 최대 OTA 플랫폼인 부킹(NASDAQ: BKNG)은 2023년 4분기 실적과 2024년 전망치를 발표했다. 이번 분기의 실적은 예상대로 4분기 사상 최고치를 기록했고, 연간 객실 이용 박수는 처음으로 10억개를 넘어섰다. 그러나 2024년 1분기 객실 이용 박수에 대한 이 회사의 기대는 4% 증가에 그칠 것으로 예상된다. 이것은 투자자들을 실망시켰다. 부킹의 성장이 한계에 근접하든, 소위 Connected Trip이 다음 성장을 추진할 수 있든, 유럽의 규제가 더욱 엄격해질 수 있든, 글로벌 리더로서의 영향력과 주주를 위한 투자 수익을 창출하는 능력은 중단기 내에 영향을 받을 수 없다.

이번 분기에 부킹의 객실 이용 박수는 2억3,100만개, GMV는 317억달러로 모두 4분기에 사상 최고치를 기록했다. 연간 객실 이용 박수는 처음으로 10억개를 돌파했다. 다른 경쟁자들이 따라잡기 힘든 수치다. 그러나 이 회사는 1분기 객실 이용 박수 증가율을 4~6%로 예상했는데, 이는 처음으로 (코로나 기간 제외) 성장률이 5%를 밑돌 수 있다는 예상이다. 4%의 성장은 1,000만개가 넘는 방야를 늘렸다는 것을 의미하지만 부킹의 방대한 기수와 적극적인 이익 전밍을 고려할 때 시장 투자자들의 마음속에서 그 지위를 흔들 수 없다.

하이저 캐피털은 부킹이 성장 한계에 직면했다는 우려는 숙박 사업에 걸맞은 2차 성장 곡선이 부족하다는 데 있다고 보고 있다. 항공권이나 이번 분기 실적 컨퍼런스콜에서 논의된 Connected Trip의 최신 정의(보험, 관광지, 렌터카 및 기타 지상 교통 상품)를 막론하고, 숙박 사업의 주도적 지위는 다른 상품이 새로운 숙박 사용자를 유치하기 위한 것이거나 'Stay + X'의 숙박 상품과 함께 묶여 판매하기 위한 것임을 의미한다. 투자 수익률을 고려할 때, 이 회사는 거대하고 전면적인 상품 조합을 가진 두 번째 주요 사업을 설립하는 데 투자할 가능성이 거의 없다. 반대로 보면 부킹이 성장 한계에 도달했음에도 그 핵심인 숙박사업은 여전히 강하다. 뛰어난 영업 능력과 모든 부문에 대한 엄격한 투자 수익률 요구 사항으로 부킹은 최상의 수수료율과 객실 재고를 계속 확보할 수 있다. 부킹의 재고는 Agoda의 가격 책정 전략과 결합하여 영원한 동기처럼 회사와 주주에게 끊임없는 이익을 가져다 줄 수 있는 대부분의 글로벌 숙박 중개인을 물리치기에 충분한다.

또한 부킹은 자본 시장의 인정을 얻기 위해 상대적으로 낮은 전망을 설정하고 추월하는 것을 좋아한다. 이번 전략도 같은 건가? 하이저 캐피털은 이것이 충분히 가능하다고 생각한다. 그러나 부킹의 최근 자본 지출은 과거와 크게 다르다. 이 회사는 주식 환매를 계속해 4분기에만 24억달러를 썼다. 보킹은 또 3월 28일 처음으로 주당 8.75달러의 분기 배당금을 지급할 예정이다. 4분기 말 상각된 주식 수에 따르면 예상 배당금은 약 3억1,000만달러다. 또 4분기 직원 스톡옵션 지출은 사상 최대인 10억3,200만달러를 기록했다. 부킹은 2만1,600명의 직원을 두고 있으며 4분기 직원 1인당 평균 스톡옵션 혜택은 4만8,000달러(연간 약 11만4,000달러)에 육박해 세계에서 가장 행복한 여행사라고 할 수 있다. 이러한 조치는 일반적으로 자본 지출이 더 필요하거나 더 효과적인 투자 수익 용도가 없음을 의미한다. 이것이 반드시 나쁜 일은 아니다. 코로나 사태 이후 부킹의 주가는 1,107달러에서 최근 3,918달러로 254% 올랐다. 이에 대해 투자자들은 불평할 것이 거의 없다.

標籤 Label: OTA Accommodation NASDAQ: BKNG Connected Trip Agoda