登錄

選單

登錄

海擇短評 Haize Comment:

近期Grab(NASDAQ: GRAB)公告2023Q4與2023全年財報,隨著財報確認轉盈,轉盈後的Grab在各地域各產品線的戰略也受到重視。Grab想必希望市值增長能像Uber(NYSE: UBER)一樣高歌猛進,但顯然兩者的護城河與戰略有很大的不同,注定Grab的路可能會更坎坷些;不過,良好的資產負債表體質,讓Grab能有更多的戰略彈性,要完成2024年的盈利指標應該不難,也許回購股票的措施,還能為市場投資人帶來意外之喜。

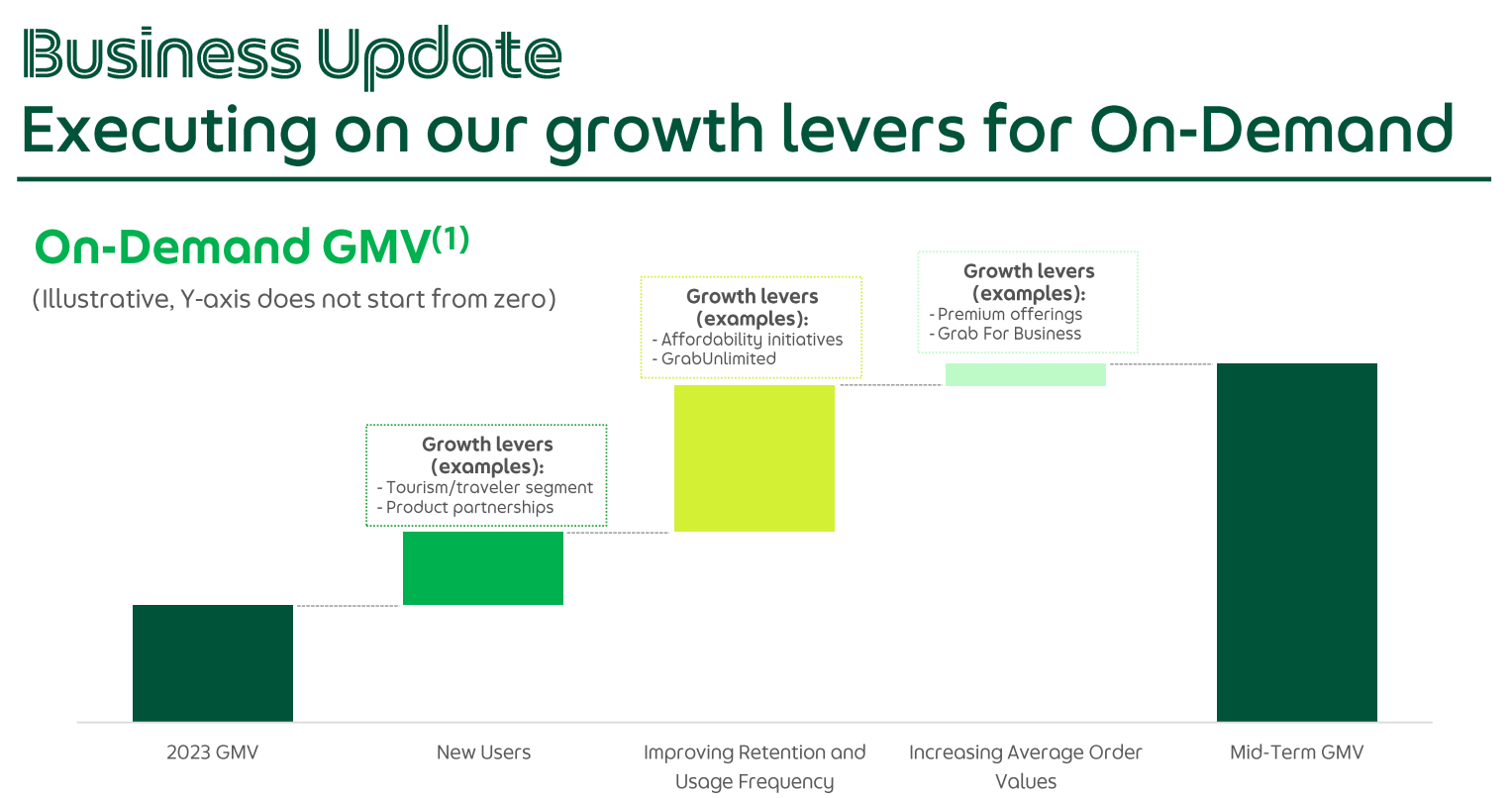

根據Grab的Q4財報,本季交易額首次超過百億美金,達110億美元;收入YoY增長30%,達6.5億美元;此前預告的轉盈目標也順利達成,除了Adjusted EBITDA轉盈達3,500萬美元外,在GAAP會計準則下也同步轉盈,達1,100萬美元,這意味著公司的股權激勵費用並不大,也沒有過高的債務利息支出。具體看Grab旗下的移動與配送兩大事業,Q2交易額分別為14.7億美元與26.5億美元,雖然兩者的YoY增速都達兩位數,但從QoQ的角度看,則有陷入瓶頸之勢,增速僅分別為4.8%與1.5%。公司本季交易活躍用戶數也僅季增170萬(4.7%),由於生活服務類公司理應相對沒有季節性效應,在減少激勵衝刺盈利之際,要維持增速似仍為挑戰。

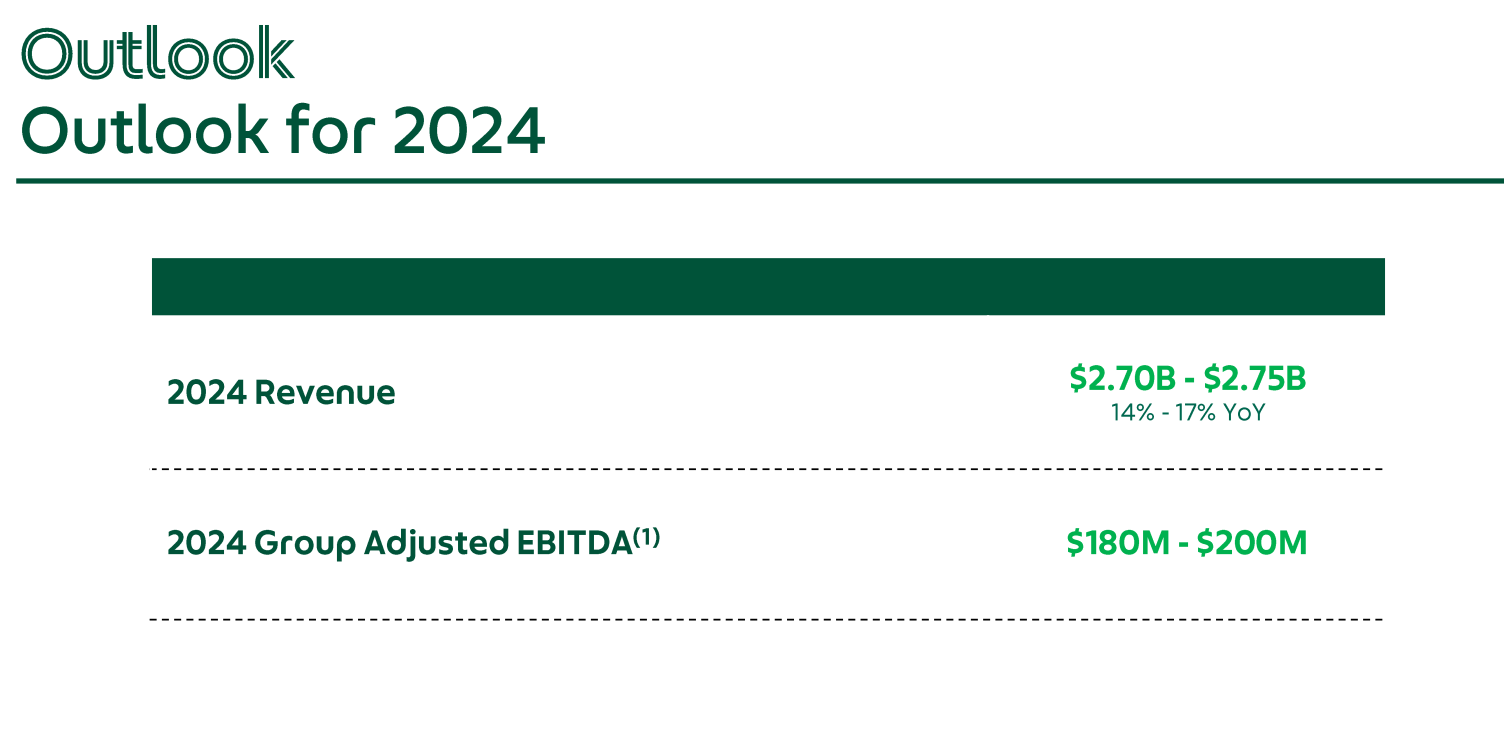

Grab對2024年的預期算差強人意,收入年增速預期為14%-17%,Adjusted EBITDA為1.8億美元-2億美元之間,對應當前P/E比超過60倍。Grab想必很希望市場投資人看待Uber的標準來看待Grab,但Uber在全球超過70個國家、超過1萬個城市都進行布局,也充分運用已開發國家閒置人力;相對來看,Grab死守東南亞開發中國家的市場,目前還不斷有進入者,較令人擔心。此外,Uber主要圍繞各個用車場景與人群深化,Grab則另外增添了在金融事業的投入,金融事業目前也還沒有明確的盈利時間表,從直播電商TikTok在印尼面對的政策紛擾來看,東南亞政策變迭快速,金融事業的水深也是個問題。

即便如此,Grab還是有個多數燒錢的互聯網公司都沒有的優勢,就是它的資產負債表體質非常穩健良好,總負債共23.2億美元,而僅現金+短期投資就有50.4億美元,這讓Grab有更好的戰略布局機會,就算沒有更好的用途,至少也能先還負債降低利息成本。本季公司公告將先清償4.97億美元貸款,同時並在5億美元的額度內進行股票回購,公司閒置資金不少,這樣的運用不會影響資本支出,但是否最後市值能比照Booking(NASDAQ: BKNG)、Expedia(NASDAQ: EXPE),為市場投資人帶來意外之喜,尚在未定之天。

----------

Grab (NASDAQ: GRAB) announced its Q4 and full-year 2023 financial reports, confirming its profitability. The strategic direction of Grab, now profitable, across various regions and product lines has garnered attention. While Grab probably aspires for market value growth akin to Uber's (NYSE: UBER), the significant differences in their moats and strategies suggest a potentially more challenging path for Grab. However, a solid balance sheet provides Grab with strategic flexibility, making it feasible to meet its 2024 profitability targets. Additionally, stock buyback measures could pleasantly surprise investors.

According to Grab's Q4 financial report, the company GMV surpassed $10 billion for the first time, reaching $11 billion. Revenue grew 30% year-over-year to $650 million. The company also achieved its previously announced profitability targets, with an Adjusted EBITDA of $35 million and a GAAP profit of $11 million. This indicates modest stock-based compensation expenses and low debt interest costs. Specifically, Grab's mobility and delivery segments posted GMV of $1.47 billion and $2.65 billion, respectively, with both segments achieving double-digit year-over-year growth. However, quarter-over-quarter growth slowed to 4.8% and 1.5%, respectively. The company's quarterly active user count only grew by 1.7 million (4.7%). As a lifestyle services company, which should theoretically be less affected by seasonal variations, maintaining growth momentum while reducing incentives for profitability appears to be a challenge.

The 2024 guidance of Grab is just passable, with revenue growth expected to be between 14%-17% and Adjusted EBITDA projected to be between $180 million and $200 million, corresponding to a P/E ratio of over 60 times. Grab likely wishes for investors to apply the same standards to it as they do to Uber. However, Uber operates in over 70 countries and more than 10,000 cities, making efficient use of idle labor in developed nations. In contrast, Grab focuses on developing markets in Southeast Asia, where competition continues to enter, raising concerns. Moreover, while Uber concentrates on deepening its services across various transportation scenarios and demographics, Grab has expanded into the financial sector, which has yet to show a clear path to profitability. Considering the policy turmoil faced by live e-commerce platforms like TikTok in Indonesia, the rapid policy changes in Southeast Asia and the complexities of the financial sector present additional challenges for Grab.

Despite its challenges, Grab possesses a significant advantage that many cash-burning internet companies lack: a robust and healthy balance sheet. With total debt at $2.32 billion and cash plus short-term investments amounting to $5.04 billion, Grab is in a strong position for strategic opportunities. Even without better uses for its funds, the company can at least reduce interest costs by paying off debt. This quarter, Grab announced it would pay off $497 million in loans and also conduct a stock buyback within a $500 million limit. With substantial idle funds, such maneuvers won't affect capital expenditure. However, whether these actions can ultimately surprise investors and match the market value success of companies like Booking (NASDAQ: BKNG) and Expedia (NASDAQ: EXPE) remains to be seen.

----------

그랩(NASDAQ: GRAB)은 2023년 4분기와 2023년 연간 재무실적을 발표했다. Grab은 각 지역 및 상품 라인의 전략적 방향으로 수익을 창출했다. 이것은 사람들의 관심을 끌었다. 그랩은 우버(NYSE: UBER)처럼 시가총액이 성장하기를 바랄 수도 있지만, 해자와 전략에서 두 회사의 현저한 차이는 그랩의 성장길이 더 도전적일 수 있음을 보여준다. 그러나 좋은 대차대조표는 그랩에게 전략적 유연성을 제공하기 때문에 그랩이 2024년의 흑자 목표를 달성하는 것은 어려운 일이 아니다. 또 주식 환매 조치는 투자자들에게 예상치 못한 놀라움을 줄 수 있다.

그랩이 발표한 4분기 실적에 따르면 GMV는 처음으로 100억달러를 돌파해 110억달러를 기록했다. 영업수익은 전년 동기 대비 30% 증가한 6억5,000만달러였다. 이 회사는 또한 Adjusted EBITDA가 3,500만달러, GAAP 이익이 1,100만달러로 흑자 전망을 달성했다. 이는 그랩의 주식 기반 임금 지출이 적정하고 부채 이자 비용이 낮다는 것을 보여준다. 구체적으로 그랩의 모바일과 배송 사업의 GMV는 각각 14억7,000만달러, 26억5,000만달러로 두 사업 모두 두 자릿수 YoY 성장을 기록했다. 그러나 QoQ 성장은 각각 4.8% 와 1.5%로 둔화되었다. 이 회사의 분기 활성 사용자 수는 170만명(4.7%) 증가하는 데 그쳤다. 이론적으로 계절 변화의 영향을 덜 받는 라이프 서비스 회사로서 수익 인센티브를 줄이면서 성장세를 유지하는 것은 도전인 것 같다.

그랩의 2024년 전망에 따라 영업수익 증가율은 14~17%, Adjusted EBITDA는 1억8,000만달러~2억달러 사이, 수익률은 60배를 넘을 것으로 예상된다. 그랩은 투자자들이 우버와 같은 기준을 적용하기를 원할 수도 있다. 그러나 우버는 70여개국 1만여개 도시에서 사업을 하며 선진국의 유휴 노동력을 효과적으로 활용했다. 이에 비해 그랩은 동남아시아의 발전 중인 시장에 집중하고 있으며, 그곳의 경쟁은 끊임없이 심화되어 그랩 사업의 미래 발전을 걱정하게 한다. 이밖에 우버는 각종 교통장면과 객군을 심화하는데 전념했다. 반면 그랩은 금융 사업 분야로 확장되었지만, 이 분야는 아직 명확한 수익 일정을 보여주지 못하고 있다. 틱톡 등 인도네시아 전자상거래가 생방송 플랫폼에서 직면한 정책 불안, 동남아 정책의 빠른 변화 및 금융 분야의 복잡성을 고려할 때 그랩에 추가적인 도전을 가져왔다.

도전에도 불구하고 그랩은 돈을 태우는 많은 인터넷 회사들이 부족한 뚜렷한 장점, 즉 안정적인 대차대조표를 가지고 있다. 총 부채금액은 23억2,000만달러, 현금에 단기투자까지 합치면 총 50억4,000만달러로 그랩을 전략적 기회의 강세로 이끌었다. 더 나은 자금 용도가 없더라도 그랩은 적어도 부채를 상환함으로써 이자 비용을 줄일 수 있다. 이번 분기에 그랩은 4억9,700만달러의 대출금을 상환하고 5억달러의 상한선 내에서 주식 환매를 할 것이라고 발표했다. 대량의 유휴자금이 있는 상황에서 이런 조치는 자본지출에 영향을 주지 않는다. 그러나 이러한 조치는 결국 그랩 시가가 부킹(NASDAQ: BKNG)과 익스피디아(NASDAQ: EXPE) 등의 시가를 따라잡고 투자자들에게 놀라움을 줄 수 있을지는 지켜봐야 한다.

標籤 Label: NASDAQ: GRAB Food Delivery Ride-Hailing Southeast Asia Gojek GOTO Uber