登錄

選單

登錄

海擇短評 Haize Comment:

嘉年華郵輪集團(NYSE: CCL)近期公告了2023Q4與2023全年財報,Q4大體上在各項運營指標都取得優於2019年同期的成績,不過基於龐大債務,在GAAP會計準則下仍處於虧損。目前來看,2024年對嘉年華郵輪集團,甚至對頭部的郵輪集團來說,仍然是個客流量暢旺的一年,但在供需關係有本質上的轉變之前,嘉年華郵輪集團要想全年在GAAP會計準則下盈利,仍是個巨大的難題。

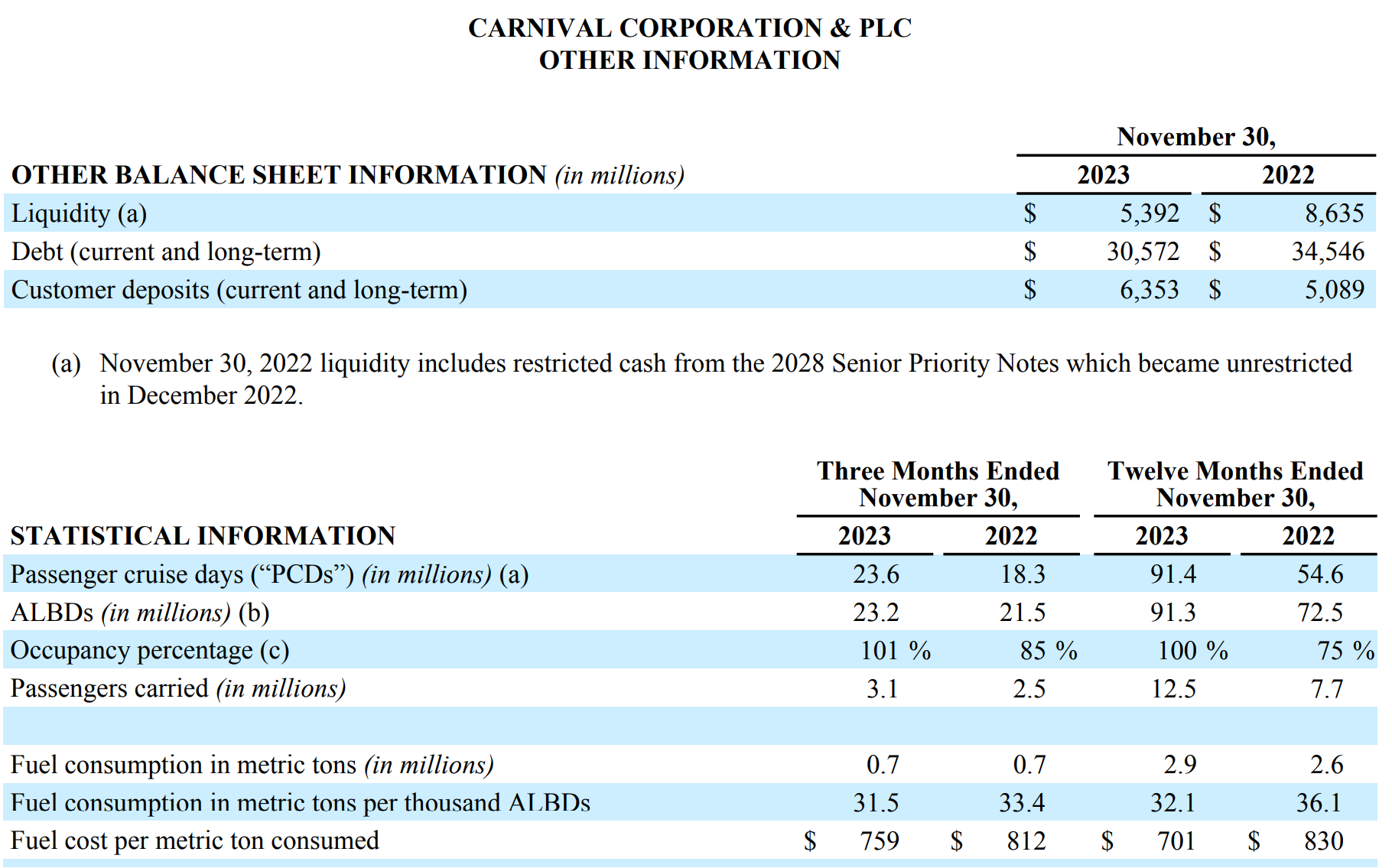

嘉年華郵輪集團在Q4取得不錯的運營成績,收入與ALBDs(Available Lower Berth Days)分別為54.0億美元與2,320萬,較2019年同期增長13%與7%;Adjusted EBITDA也不錯,創下9.5億美元的佳績。除此之外,公司也披露了不少2024年運營面的正向資訊,比如入住率將能維持100%左右的歷史高位、總運力將增加5%、約有30%的運力屬於新交付的船支(新船更有競爭力)、預估2024到2026年的船票定價都能有5%的成長、整體收入能有10%以上的增長、可控的運營費用增長將低於4%...等等。

不過,嘉年華郵輪集團在Q4雖有著9.5億美元的Adjusted EBITDA,但若依GAAP會計準則結算,卻仍虧損4,800萬美金,原因來自於以債務利息為主的業外支出就達4.2億美金。這意味著,雖然嘉年華郵輪集團的運營比2019年好,但比2019年還龐大多倍的債務,已大到足以抵銷所有的正向優勢,門票定價更高、運力增加更多、新船佔比更高、入住率維持高位,實際上都無關勝敗。公司在2023年還了60億美元的債務,但年底債務仍略高於300億美元,說嘉年華郵輪集團主要是在幫銀行團打工也不為過。

從上述的角度看,郵輪集團並不容易盈利。海擇資本覺得郵輪旅遊的體驗很好,員工旅遊也常選擇歐洲郵輪出行,但顯然消費市場並沒有認同到認為船票能有比2019年同期翻倍或增長50%的程度,主要原因應該是供給仍大,需求也沒有巨幅增長,而且臨期的艙位很難賺錢,雖然機票跟住宿也相同,但是郵輪行業的彈性更差,反倒是任何預期之外的風險(高油價、重要目的地國家發生戰爭、公司繼續增發股票籌資...等等),都可能影響郵輪集團的每股盈利。不過,從好處看,去年還了60億美元,至少今年的利息可以比去年少些了,不是嗎?

----------

Carnival Cruise Line (NYSE: CCL) released its Q4 and full-year 2023 financial reports, with Q4 performance generally exceeding operational metrics from the same period in 2019. However, due to substantial debt, the company still reported a loss under GAAP accounting standards. Looking ahead to 2024, it appears to be a year of strong passenger flow for Carnival Cruise Line and other leading cruise operators. Yet, turning a full-year profit under GAAP standards remains a significant challenge until there is a fundamental shift in the supply-demand dynamic.

CCL achieved solid operational results in Q4, with revenue and Available Lower Berth Days (ALBDs) reaching $5.4 billion and 23.2 million, respectively, marking a 13% and 7% increase over the same period in 2019. The Adjusted EBITDA was also impressive, at $950 million. Furthermore, the company disclosed positive operational outlook for 2024, including occupancy rates expected to maintain around 100% historical highs, total capacity increasing by 5%, about 30% of capacity from newly delivered ships (which are more competitive), ticket pricing estimated to grow by 5% from 2024 to 2026, overall revenue expected to increase by more than 10%, and controllable operational cost growth to be below 4%, among other aspects.

Despite CCL achieving an Adjusted EBITDA of $950 million in Q4, it still incurred a loss of $48 million under GAAP accounting standards, primarily due to interest expenses on debt reaching $420 million. This indicates that while Carnival's operations have improved since 2019, its significantly larger debt load has effectively neutralized all positive gains, despite higher ticket pricing, increased capacity, a higher proportion of new ships, and sustained high occupancy rates. The company repaid $6 billion in debt in 2023, but its year-end debt level remained just over $30 billion, suggesting that Carnival is essentially working for its lenders.

From the perspective mentioned above, it's not easy for cruise lines to be profitable. Haize Capital believes that cruise travel offers a great experience, and its employees often choose European cruises for trips. However, it's clear that the consumer market does not agree to the extent that ticket prices could double or increase by 50% compared to the same period in 2019. The primary reason is likely that supply still exceeds demand, which hasn't grown significantly. Additionally, last-minute bookings are hard to profit from. While the airline and hotel industries face similar challenges, the cruise industry has less flexibility. Unexpected risks such as high fuel costs, wars in key destination countries, or companies issuing more stock to raise funds can all impact cruise lines' earnings per share. However, on the bright side, repaying $6 billion last year means at least this year's interest expenses should be lower than last year's, right?

----------

카니발 크루즈(NYSE: CCL)는 2023년 4분기와 2023년 연간 재무 실적을 발표했다. 4분기 실적은 보편적으로 2019년 동기를 초과했다. 그러나 막대한 부채 때문에 카니발 크루즈의 실적은 GAAP 회계 준칙 하에서 여전히 적자를 내고 있다. 2024년을 내다보면 카니발 크루즈와 다른 선도적인 크루즈 운영사들에게는 여객 흐름이 강한 한 해로 보인다. 그러나 공급과 수요의 동태에 근본적인 전환이 일어나기 전에 공인회계준칙(GAAP)에 따라 연간 이윤을 실현하는 것은 여전히 중대한 도전이다.

카니발 크루즈는 4분기에 견조한 운항 실적을 거둬 수익과 ALBDs(Available Lower Berth Days)가 각각 54억달러와 2,320만달러로 2019년 동기보다 13%, 7% 증가했다. Adjusted EBITDA도 9억5,000만달러로 선전했다. 또한 카니발 크루즈는 긍정적인 2024년 운항 전망을 밝혔다. 입주율이 100% 내외로 사상 최고치를 유지할 것으로 예상된다. 총 수송력이 5% 증가할 것으로 예상된다. 새로 도입되는 선박 수송력이 약 30%(더욱 경쟁력 있음), 2024년부터 2026년까지 운임이 5% 증가할 것으로 예상된다. 전체 수익은 10% 이상 증가할 것으로 예상되며, 운영비 증가는 4% 미만일 것으로 예상된다.

카니발 크루즈는 4분기에 9억5,000만달러의 Adjusted EBITDA를 달성했지만 GAAP 회계준칙에 따르면 4,800만달러의 손실을 기록했다. 부채 이자 지출이 4억2,000만 달러에 달한 것이 주요 원인이다. 이는 2019년 이후 카니발의 운영이 개선됐음에도 불구하고, 운임 상승, 수송력 증가, 신규 선박 비율 증가, 높은 입주율 지속에도 불구하고, 현저하게 증가한 채무 부담이 모든 긍정적인 수익을 상쇄했음을 보여준다. 카니발 크루즈는 2023년에 60억달러의 부채를 상환했지만 연말 부채 수준은 여전히 300억달러를 약간 초과했다. 이는 카니발이 실제로 은행을 위해 일하고 있음을 보여준다.

위에서 언급한 관점에서 볼 때, 크루즈 회사가 이익을 내기는 쉽지 않다. 하이저 캐피털은 크루즈 여행이 훌륭한 체험을 제공한다고 생각한다. 예를 들어 직원 여행은 종종 유럽 크루즈 여행을 선택한다. 그러나 소비자 시장은 티켓 가격이 2019년 동기보다 두 배 또는 50% 상승했다는 것에 동의하지 않는 것이 분명한다. 주요 원인은 공급이 수요를 초과했기 때문일 수 있지만 수요는 크게 증가하지 않았다. 게다가 임박한 배표 예약은 이득을 보기 어렵다. 항공권과 호텔 숙박도 비슷한 도전에 직면했지만 크루즈 업계의 유연성은 더 낮았다. 연료 비용이 높고, 주요 목적지 국가의 전쟁이나 회사가 자금을 조달하기 위해 더 많은 주식을 발행하는 등 예기치 못한 위험은 크루즈 회사의 주당 수익에 영향을 미칠 수 있다. 그러나 좋은 면에서 볼 때, 작년 카니발 크루즈가 60억 달러를 상환한 것은 적어도 올해 이자 지출이 작년보다 낮아야 한다는 것을 의미하지 않을까?

標籤 Label: NYSE: CCL NYSE:RCL NASDAQ:NCLH Cruise