登錄

選單

登錄

海擇短評 Haize Comment:

當前是否是"去全球化年代",這件事容有質疑,不過可以確定的是,能真正以互聯網模式擴張、並以盈利取得市值增長的公司,已是鳳毛麟角,而無疑的,Uber(NYSE: UBER)是經得起質疑的公司。2023年,Uber在全球25個國家/地區擁有1,900萬名會員,並證明了能以規模化得實現獲利成長;Q4,Uber共成立了26.0億張付費訂單,YoY增長24%,QoQ增長1%;Adjusted EBITDA取得12.8億美金盈利,YoY增長93%,QoQ增長17%,除了跨越了季節性因素的影響,並在GAAP角度連續盈利,超過1,500億美金的市值也成為全球互聯網公司的指標。

這次Uber各事業線的強勁財務數據我們就不展開談,海擇資本更想提及的是,Uber核心"網約車"本業的盈利只是結果,算法是輔助它更有效率的方式,能盈利的核心要素之一是對司機的控制力。若將2023Q4與2021Q4相比,從需求層面看,Uber"網約車"事業的司機供應量增長了75%,登錄車輛增長了56%;而相同時間內,從需求層面看,用戶數增長量為39%。即便僅將2023Q4對比2022Q4,平台上的司機數量也年增30%,這表示Uber對司機的控制力是事業的核心驅動力,也是平台維持健康的主要原因,而大量的司機資源除了與全球經濟不景氣有關,也與旅遊行業業者常抱怨的缺工問題有部分因果關係。

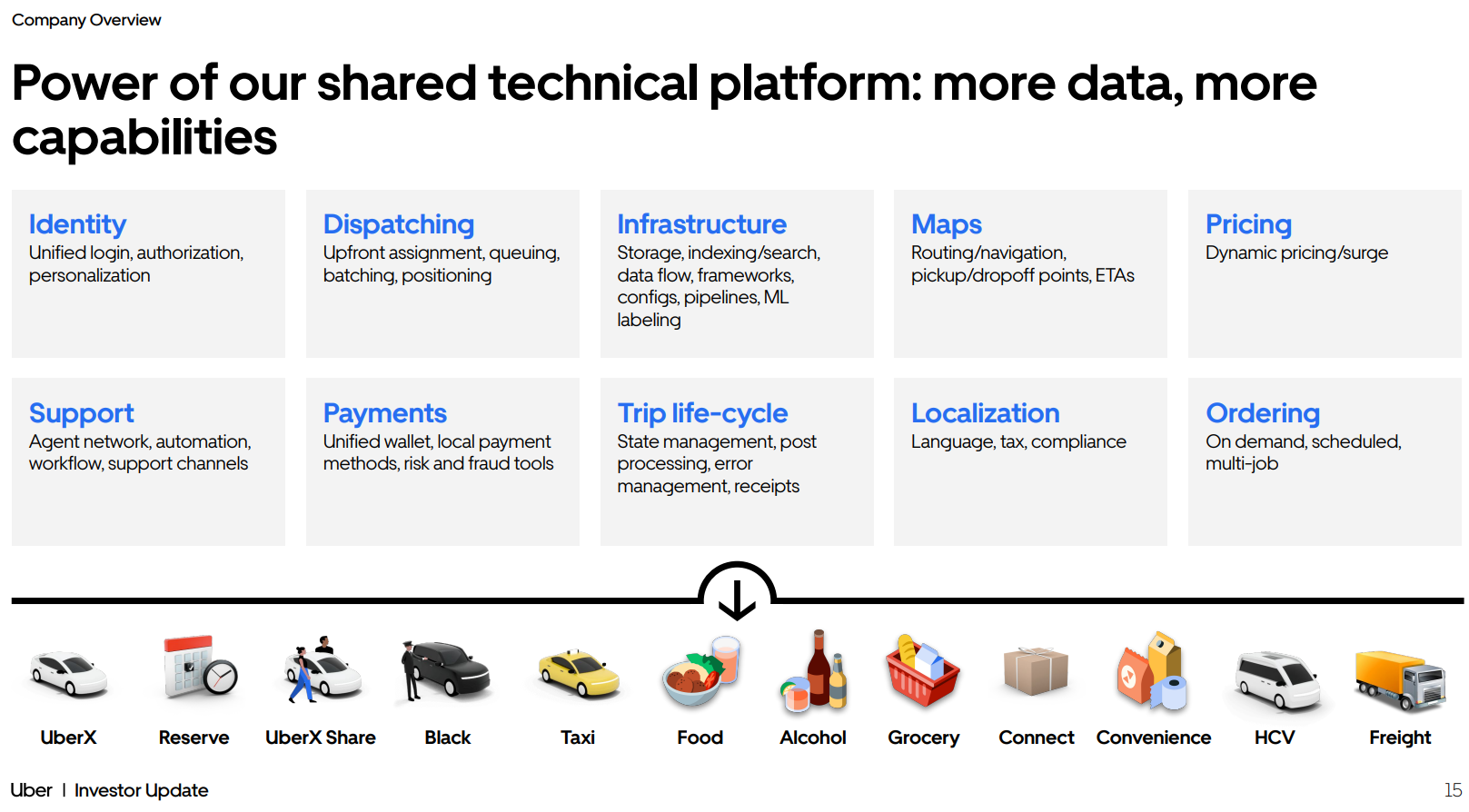

根據Uber公告的戰略,其針對不同人群所細分的產品線已更為多樣,有"Uber for Business"、"Uber Health"、"Uber Direct"、"Uber Connect"、"Advertising"等等;而僅僅網約車事業,就針對注重成本的消費者,提供"UberX Share"和兩輪車及三輪車;針對願意為更好的汽車支付溢價的消費者,也提供各類禮賓用車;甚至也對司機提供汽車責任險,而從Uber的運營數據與技術能力來看,海擇資本不會認為這些新品類不適合。本季財報時,Uber也同步給到了3年的預期,認為3年交易額的CAGR能做到15%-19%間,3年Adjusted EBITDA CAGR能做到30%-40%之間,即便對應Uber過去的預期,這也都略顯激進了,特別是EBITDA的部分,不過比起我們此前也談過的Sabre(NASDAQ: SABR),它似乎可靠得多。

----------

Whether we are in an era of "de-globalization" is debatable, but what's certain is that companies capable of expanding through the internet model and achieving market value growth through profitability are rare. Undoubtedly, Uber (NYSE: UBER) is one company that stands up to scrutiny. In 2023, Uber had 19 million members across 25 countries/regions, demonstrating its ability to achieve profit growth at scale. In Q4, Uber processed 2.6 billion paid orders, with a year-over-year (YoY) increase of 24% and quarter-over-quarter (QoQ) increase of 1%. Its Adjusted EBITDA reached a profit of $1.28 billion, with a YoY increase of 93% and QoQ increase of 17%, overcoming seasonal factors and achieving continuous profitability from a GAAP perspective. With a market value exceeding $150 billion, it has become a benchmark among global internet companies.

This time, we won't delve into the strong financial data across Uber's various business lines. Instead, Haize Capital wants to highlight that the profitability of Uber's core ride-hailing business is merely a result; algorithms assist in enhancing efficiency, but one of the core elements of profitability is control over drivers. Comparing Q4 2023 with Q4 2021, from the demand side, the supply of drivers for Uber's ride-hailing service increased by 75%, and the number of registered vehicles grew by 56%; meanwhile, customer numbers saw a 39% increase during the same period. Even when comparing Q4 2023 to Q4 2022, the number of drivers on the platform increased by 30% annually. This indicates that control over drivers is a central driving force of the business and a primary reason for maintaining platform health. The abundance of driver resources is related not only to the global economic downturn but also partly to the labor shortage issues frequently lamented by the tourism industry.

According to Uber's announced strategy, its product lines tailored to different demographics have become more diverse, including "Uber for Business," "Uber Health," "Uber Direct," "Uber Connect," "Advertising," and more. Specifically for the ride-hailing business, for cost-conscious consumers, it offers "UberX Share" along with motorcycle and tricycle services. For those willing to pay a premium for better vehicles, it provides various luxury car services. It even offers auto liability insurance for drivers. Given Uber's operational data and technical capabilities, Haize Capital does not consider these new categories unsuitable. In its quarterly financial report, Uber also provided a 3-year forecast, projecting a 15%-19% CAGR in transaction volume and a 30%-40% CAGR in Adjusted EBITDA over the next three years. Even by Uber's past projections, these targets are somewhat aggressive, especially for EBITDA. However, compared to Sabre (NASDAQ: SABR), which we've also discussed before, Uber seems much more reliable.

----------

우리가 "탈세계화"의 시대에 처해있는지는 아직 검토해야 하지만 분명한 것은 인터넷 모델을 통해 확장하고 이익을 통해 시가 성장을 실현할 수 있는 회사가 이미 매우 적다는 것이다. Uber(NYSE: UBER)는 의심의 여지가 없는 회사다. 2023년 우버는 25개국에서 1,900만명의 회원을 보유하여 대규모 이익 성장을 달성 할 수 있는 능력을 입증했다. 전년 4분기에 우버는 전년 동기 대비 24%, 분기 대비 1% 증가한 26억건의 유료 주문을 처리했다. Adjusted EBITDA는 12억8,000만달러로 전년 동기 대비 93%, 분기 대비 17% 증가하며 계절적 요인을 극복하고 GAAP 회계기준에서 지속적인 흑자를 달성했다. 현재 시가가 1,500억달러를 넘어 전 세계 인터넷 회사의 벤치마킹이 되었다.

이번에 우리는 우버의 각 사업 라인의 강력한 재무 데이터를 깊이 연구하지 않을 것이다. 하이저 캐피털이 강조하고자 하는 것은 우버의 핵심 '온라인 예약차' 사업의 이익은 하나의 결과일 뿐이며, 알고리즘이야말로 효율을 높이는 데 도움이 되는 관건이라는 것이다. 수익성의 핵심 요소 중 하나는 운전자에 대한 통제다. 2023년 4분기와 2021년 4분기를 비교했을 때 수요 측면에서 우버 온라인 예약차 서비스의 운전자 수는 75%, 등록 차량 수는 56% 증가했다. 이와 함께 고객 수는 동기 대비 39% 증가했다. 2023년 4분기와 2022년 4분기 데이터를 비교해도 이 플랫폼의 운전자 수는 매년 30% 증가하고 있다. 이는 운전자에 대한 통제가 사업의 핵심 추진력이자 플랫폼의 건강을 유지하는 주요 원인임을 보여준다. 성장한 운전기사 자원은 글로벌 경기 침체뿐만 아니라 여행업이 자주 불평하는 노동력 부족 문제와도 관련이 있다.

우버가 발표한 전략에 따르면 'Uber for Business', 'Uber Health', 'Uber Direct', 'Uber Connect', 'Advertising'등 다양한 사람들을 위한 제품 라인이 더욱 다양해졌다. 온라인 예약차 사업을 예로 들면, 비용을 중시하는 소비자를 대상으로 "UberX Share"와 오토바이 및 삼륜차 서비스를 제공한다. 더 나은 자동차에 프리미엄을 지불하려는 사람들에게, 그것은 각종 호화 자동차 서비스를 제공한다. 그것은 심지어 운전자에게 자동차 책임 보험을 제공한다. 우버의 운영 데이터와 기술력으로 볼 때 하이저 캐피털은 이런 새로운 카테고리가 적합하지 않다고 생각하지 않는다. 분기 실적에서 우버는 향후 3년간의 전망도 제공했다. 향후 3년간 거래량은 CAGR이 15%~19%, Adjusted EBITDA CAGR이 30%~40%로 예상된다. 우버의 과거 전망대로라도 이런 목표들은 다소 급진적이다. 특히 EBITDA다. 그러나 우리가 이전에 논의 한 Sabre(NASDAQ: SABR)에 비해 Uber는 훨씬 더 신뢰할 수 있는 것으로 보인다.

標籤 Label: NYSE: UBER Food Delivery Ride-hailing Sharing Economy