登錄

選單

登錄

海擇短評 Haize Comment:

途牛(NASDAQ: TOUR)近期公告2023Q4與2024全年財報,全年創下歷史首次nonGAAP盈利,雖然目前看來2024年沒有優於行業與爆發式好轉的跡象,但從財務層面看終於已接近上岸。

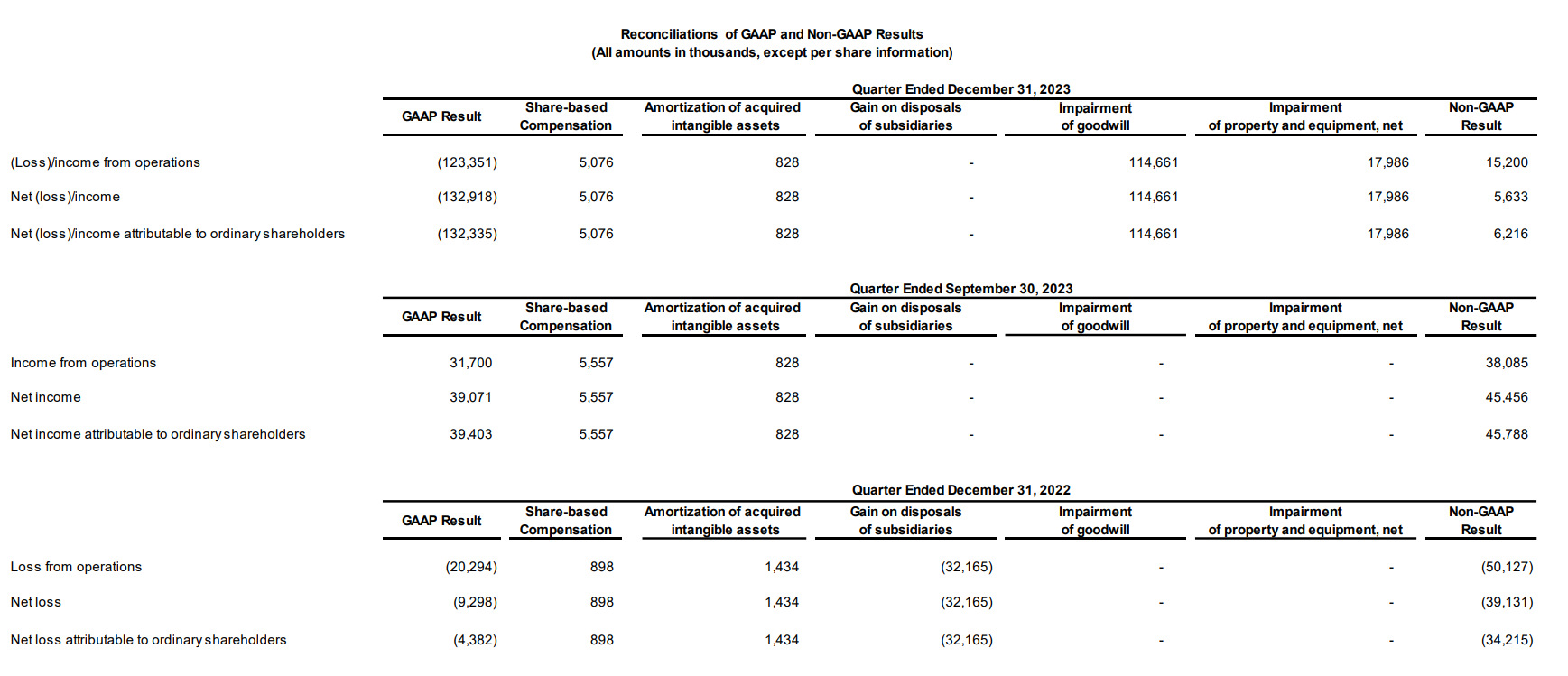

根據途牛財報,公司Q4收入為9,990萬人民幣,YoY增長266%,惟若與2019年相比,僅為同期的22%;公司本季運營虧損1.2億人民幣,全年虧損1.0億人民幣。雖然收入與2019年相差頗巨,但由於成本與費用的控制更為嚴格,因此若以nonGAAP會計準則結算,Q4與全年均屬轉虧為盈,Q4運營利潤為1,520萬人民幣,全年運營利潤達5,003萬人民幣;此外,不同會計準則間的盈虧差異主要為Q4認列一筆1.1億人民幣的商譽減損,這並非基於實際交易產生的虧損,我們判定途牛的盈利是屬於比較紮實穩健的盈利。

本季途牛也公告了對2024Q1的收入預期,公司預計Q1的收入在10.11億人民幣至10.74億人民幣之間,亦即較2023Q1增長60%至70%;若與2019Q1相比,則介於衰退76%至78%之間,與Q4相比,衰退規模相仿,雖無爆發式好轉,但也沒有更差。若將IATA發布的中國國際旅客輸送量數據,做為出境團隊遊行業的復甦參照,途牛的復甦約比中國出境旅客的復甦弱一半左右;考慮到途牛以團隊遊為主,而疫情後很多國家在團隊遊領域的復甦在比FIT弱很多,途牛的數據也算合理。海擇資本認為,公司如果要有優於行業的表現,一個方法是增加非團隊遊產品的投入,一個是爭取新旅遊銷售渠道的紅利,比如抖音,這兩部分目前途牛都有做,重點還是在於投資報酬率。

依目前公告中國的攜程(NASDAQ: TCOM)、同程(HK: 0780)、途牛三家旅遊公司的疫後財報來看,若不談三者在行銷與獲客上的ROI,其復甦與盈利潛力的主要分野,在於國際化布局深度與FIT產品廣度,攜程的國際化已能有正向回報,同程的境外投資/運營才剛開始,途牛是大病初癒,病去若抽絲,還需要更長的時間與投入厚積實力。

----------

Tuniu (NASDAQ: TOUR) recently announced its Q4 2023 and full-year 2024 financial results, marking the company's first non-GAAP profit in history. Although there are no signs of significant improvement or outperformance compared to the industry for 2024, the financial perspective suggests it is finally nearing recovery.

According to Tuniu's financial report, the company's Q4 revenue was 99.9 million RMB, a 266% YoY increase, yet only 22% of the same period in 2019. The quarterly operating loss was 120 million RMB, with an annual loss of 100 million RMB. Despite the significant revenue gap compared to 2019, stricter cost and expense control led to a non-GAAP profit for both Q4 and the full year. Q4 operating profit was 15.2 million RMB, with an annual operating profit of 50.03 million RMB. The difference in profit and loss under different accounting standards mainly comes from a one-time goodwill impairment of 110 million RMB in Q4, which is not a loss from actual transactions. We assess Tuniu's earnings as relatively solid and robust.

This quarter, Tuniu also announced its revenue forecast for Q1 2024, expecting revenue to be between 1.011 billion and 1.074 billion RMB, a 60% to 70% increase from Q1 2023. Compared to Q1 2019, this represents a 76% to 78% decline, similar to the decline from Q4, indicating no explosive improvement but also no further deterioration. Using IATA's data on China's international passenger traffic as a reference for the recovery of outbound group travel, Tuniu's recovery is about half that of Chinese outbound travelers. Given Tuniu's focus on group tours and the slower recovery of group travel post-pandemic in many countries compared to FIT, Tuniu's performance is considered reasonable. Haize Capital suggests that to outperform the industry, Tuniu could increase investment in non-group tour products and seek new sales channels, such as Douyin. Tuniu is currently doing both, with the focus on investment return.

Based on the post-pandemic financial reports of Chinese travel companies Ctrip (NASDAQ: TCOM), Tongcheng (HK: 0780), and Tuniu as announced, without discussing the ROI in marketing and customer acquisition, the main differences in their recovery and profit potential lie in the depth of internationalization and the breadth of FIT products. Ctrip has already seen positive returns from its internationalization efforts, Tongcheng is just beginning its overseas investments/operations, and Tuniu, still recovering from a severe setback, will need more time and investment to build its strength.

----------

투뉴(Tuniu, NASDAQ: TOUR)는 2023년 4분기와 2024년 연간 재무 실적을 발표했다. 이는 투뉴가 역사상 처음으로 nonGAAP 이익을 달성했다. 2024년과 비교했을 때 이 업종이 눈에 띄게 개선되거나 선전하는 추세를 보이고 있다는 징후는 없지만 재무적으로 회복에 거의 근접해 있다.

투뉴의 재무실적에 따르면 4분기 수익은 9,990만위안으로 전년동기대비 266% 증가했지만 2019년 동기의 22%에 그쳤다. 분기별 경영손실은 1억2,000만위안, 연간 손실은 1억위안이다. 2019년에 비해 소득 격차가 크지만 원가와 비용 통제가 상당히 엄격해 실제로 4분기와 연간은 nonGAAP 이익을 달성했다. 4분기 영업이익은 1,520만위안, 연간 영업이익은 5,003만위안이다. 부동한 회계준칙하의 손익차이는 주로 4분기 영업권감액 1억1,000만위안에서 온것이지 실제거래손실이 아니다. 그래서 우리는 투뉴의 수익이 상대적으로 안정적이라고 생각한다.

이번 분기에 투뉴는 2024년 1분기 수익 전망도 발표했다. 수익은 2023년 1분기보다 60%~70% 증가한 10억1,100만~10억7,400만위안 사이가 될 것으로 예상된다. 2019년 1분기와 비교하면 감소 비율은 76%~78% 사이다. 4분기 실적과 비슷한 수준으로 폭발적인 개선도, 추가 악화도 없었다. IATA가 발표한 중국 국제 여객 수송량 데이터를 참조로 패키지 해외여행 회복의 참조로 삼는다면 투뉴의 회복 폭은 중국 해외여행 회복폭의 약 절반이다. 투뉴의 업무 중점이 단체여행이고 코로나 이후 많은 나라의 단체여행 회복 속도가 FIT에 비해 느리다는 점을 감안하면 투뉴의 데이터도 합리적인 범위 내에 있다. 하이저 캐피털은 업계를 이기기 위해 투뉴가 비패키지 여행상품에 대한 투입을 확대하고 틱톡과 같은 새로운 판매 채널을 모색할 수 있다고 제안했다. 투뉴는 현재 상술한 두 방면에서 모두 모색하고 있는데, 중점은 투자 수익률이다.

씨트립(NASDAQ: TCOM), 퉁청여행(HK: 0780)과 투뉴가 발표한 코로나 이후의 재무실적에 따르면 마케팅과 고객 투자 수익률을 논의하지 않는 상황에서 이들의 회복과 수익 잠재력의 주요 차이는 국제화의 깊이와 FIT 상품의 넓이에 있다. 씨트립은 이미 국제화 노력에서 적극적인 보답을 받았다. 퉁청여행은 해외 투자 / 운영을 막 시작했다. 투뉴는 여전히 심각한 좌절에서 회복되고 있으며, 자신의 실력을 쌓기 위해 더 많은 시간과 투자가 필요할 것이다.

標籤 Label: NASDAQ: TOUR China NASDAQ: TCOM HK: 0780