登錄

選單

登錄

海擇短評 Haize Comment:

同程旅行:規模與影響力已達攜程25%-30%

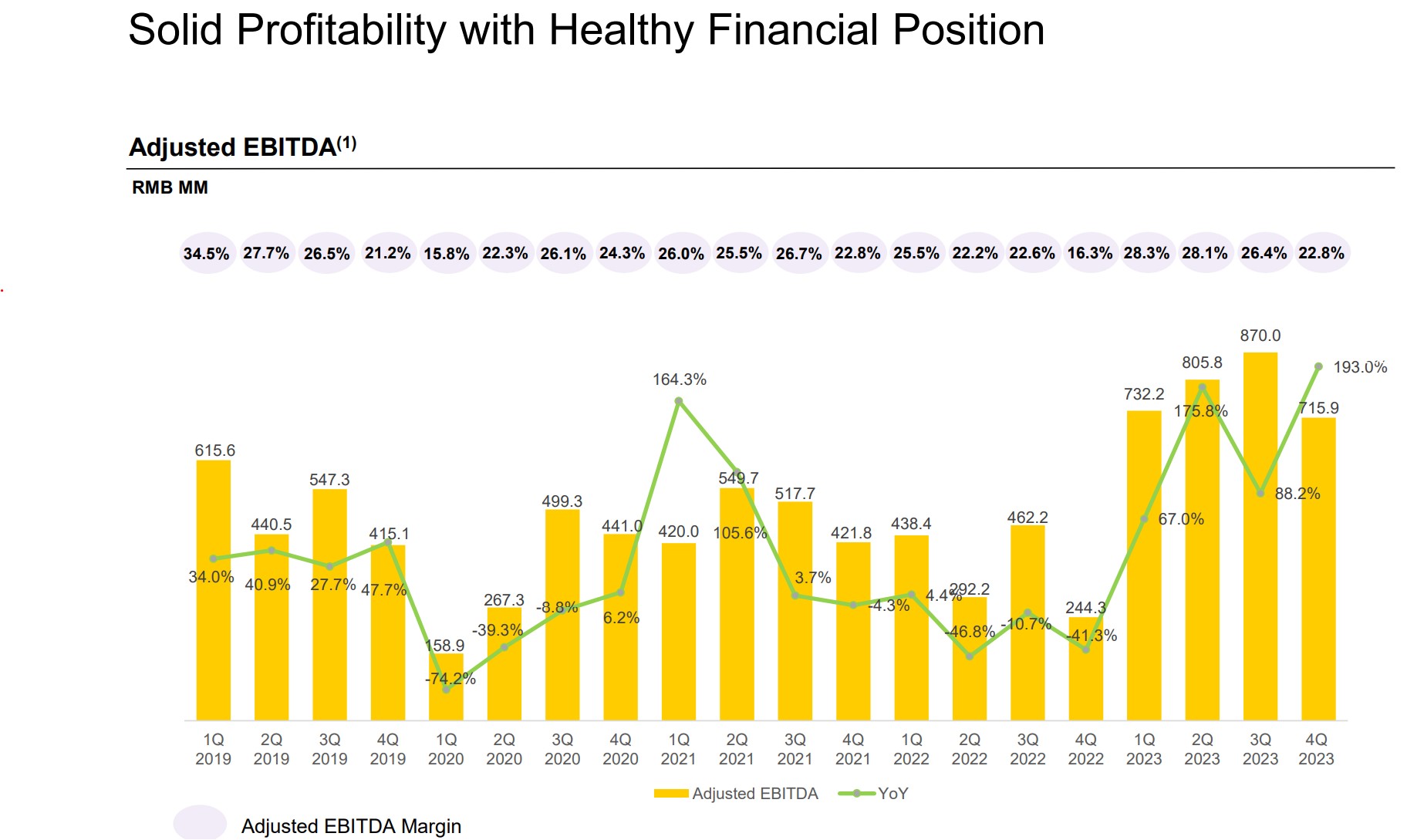

同程旅行(HK: 0780)近期公告2023Q4與2023全年財報,公司如預期般有著大幅優於行業與2019年的成績,Q4收入與Adjusted EBITDA分別為31.4億人民幣、7.1億人民幣,YoY分別增長24%、48%,較2019年同期分別增長60%、73%。隨著規模成長與併入產品線增加,同程與攜程(NASDAQ: TCOM)的可比性越來越接近,也將會值得比較,相比兩者本次財報,收入上同程約是攜程的30%,Adjusted EBITDA則約為25%,顯見其規模與影響力已經不小。

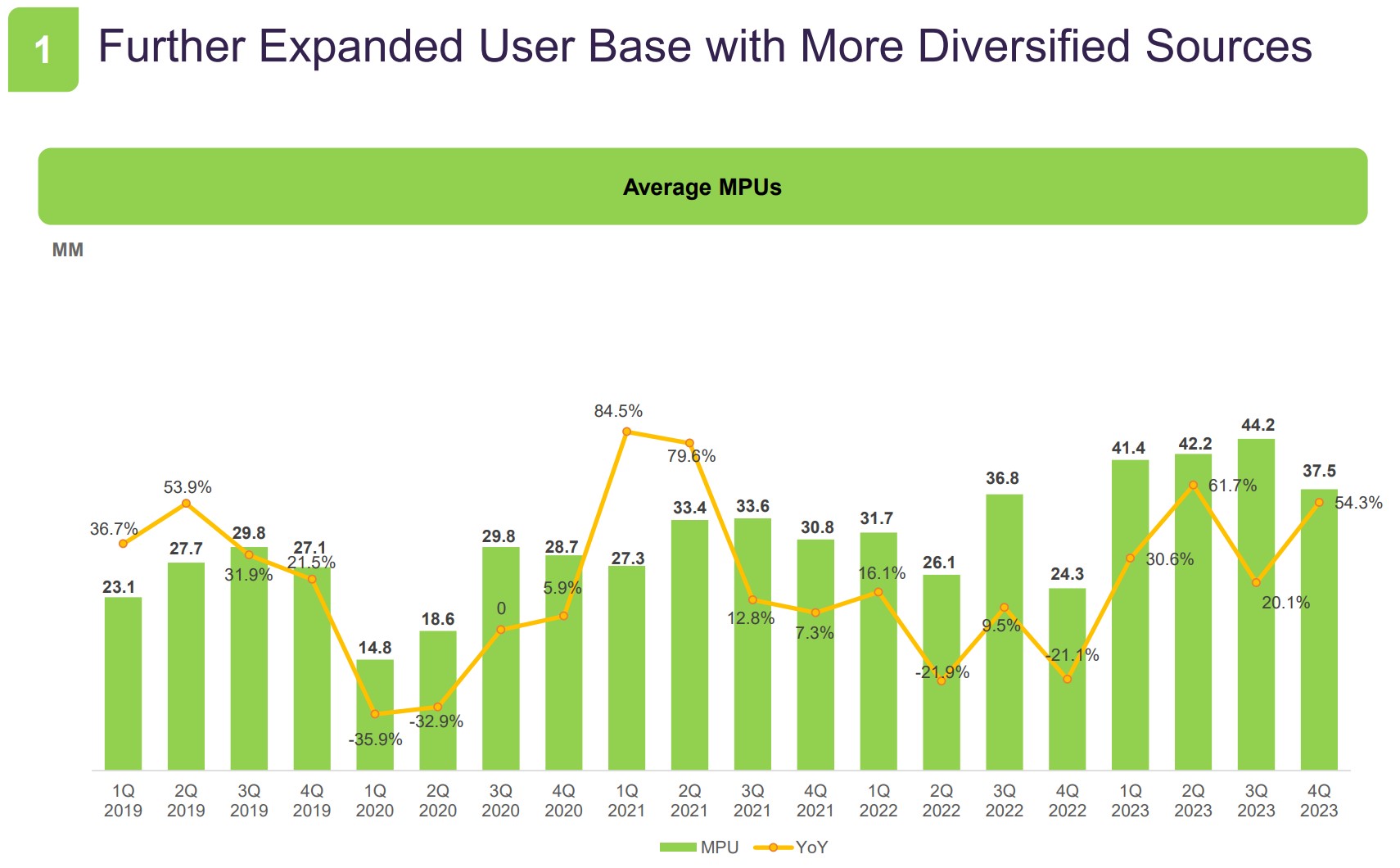

本季同程在下沉市場的運營數據透露出警訊。目前,下沉市場仍是同程自我定位的戰略重點,但Q4同程在中國非一線城市的註冊用戶為總註冊用戶總數86.9%,相比於Q3的87.0%,首次出現下滑;雖然下滑數據極微小,但也意味著同程現有的用戶增長通路出現警訊,亟待在其他目標市場出現突破。

海擇資本認為,從各產品線運營現況來看,Q4相對於Q3有季節性衰退很正常,唯以交通票務及住宿預訂兩項主業來說,前者的收入14.7億元人民幣,季衰減約12%,後者則為8.8億元人民幣,季衰減約22%,看來交通票務更為堅韌穩定些。此外,本季其他事業的收入為7.9億元人民幣,QoQ增長60%,YoY增長136%,較2019年同期增長416%,成長曲線增速良好;就細節組成來看,該事業涵蓋旅遊服務(包括線上線下旅遊平台)、廣告服務、酒店管理服務、會員服務、配套增值用戶服務、商務旅遊服務,這部分取得高增長的原因,可能是基於存量增長,可能來自增量收購,其中增量收購也許一部分來自於併入原同程控股的線下服務,這樣的可控性更高。

------

Tongcheng Travel: Scale and Influence Reach 25%-30% of Ctrip's

Tongcheng Travel (HK: 0780) recently announced its Q4 and full-year financial results for 2023. As expected, the company significantly outperformed the industry and its 2019 results. Q4 revenue and Adjusted EBITDA were RMB 3.14 billion and RMB 710 million, respectively, representing YoY increases of 24% and 48%, and growth of 60% and 73% compared to the same period in 2019. As the company grows and expands its product lines, its comparability with Trip.com (NASDAQ: TCOM) is increasing and worth noting. Compared to Trip.com in this financial report, Tongcheng's revenue is about 30% of Trip.com's, and its Adjusted EBITDA is about 25%, indicating significant scale and influence.

This quarter, Tongcheng's operational data in the lower-tier markets has shown warning signs. Although these markets remain a strategic focus for Tongcheng's self-positioning, Q4 saw a slight decline in the proportion of registered users from non-first-tier cities in China, accounting for 86.9% of total registrations, down from 87.0% in Q3. Although the decline is very small, it signals potential issues in Tongcheng's current user growth channels, indicating an urgent need for breakthroughs in other target markets.

Haize Capital believes that looking at the operation of various product lines, it's normal for Q4 to show a seasonal decline compared to Q3. Specifically, for the main businesses of transportation ticketing and accommodation booking, the former generated revenue of RMB 1.47 billion, with a seasonal decline of about 12%, while the latter saw RMB 880 million in revenue, with a decline of about 22%, indicating that transportation ticketing is relatively more resilient and stable. Additionally, revenue from other businesses this quarter was RMB 790 million, showing a QoQ growth of 60%, YoY growth of 136%, and an increase of 416% compared to the same period in 2019, indicating a strong growth curve. These businesses include travel services (both online and offline platforms), advertising services, hotel management, membership services, supporting value-added customer services, and corporate travel services. The high growth in this segment may be due to organic growth and possibly from incremental acquisitions, some of which may have involved integrating offline services from the original Tongcheng holdings, thus offering greater control.

標籤 Label: 0780 3690 TCOM Trip.com