登錄

選單

登錄

海擇短評 Haize Comment:

美團:組織調整是面對宏觀環境及競爭格局的歷史性總結

美團(HK: 3690)此前發布2023Q4與2023全年年報,年報創下2021年以來首次轉盈,也可以理解為因應2月組織變動的歷史總結。當前中美地緣政治現況影響重大,也導致美團用戶生命周期的購買力已與2019年時的假設有極大差異,這也是多數與中國消費有關公司所遇到的重大挑戰,面對新的宏觀環境及競爭格局,美團組織調整的思路與資源投入的方式將比本次財報數據本身更為重要。海擇資本解讀本期財報部份重點如下:

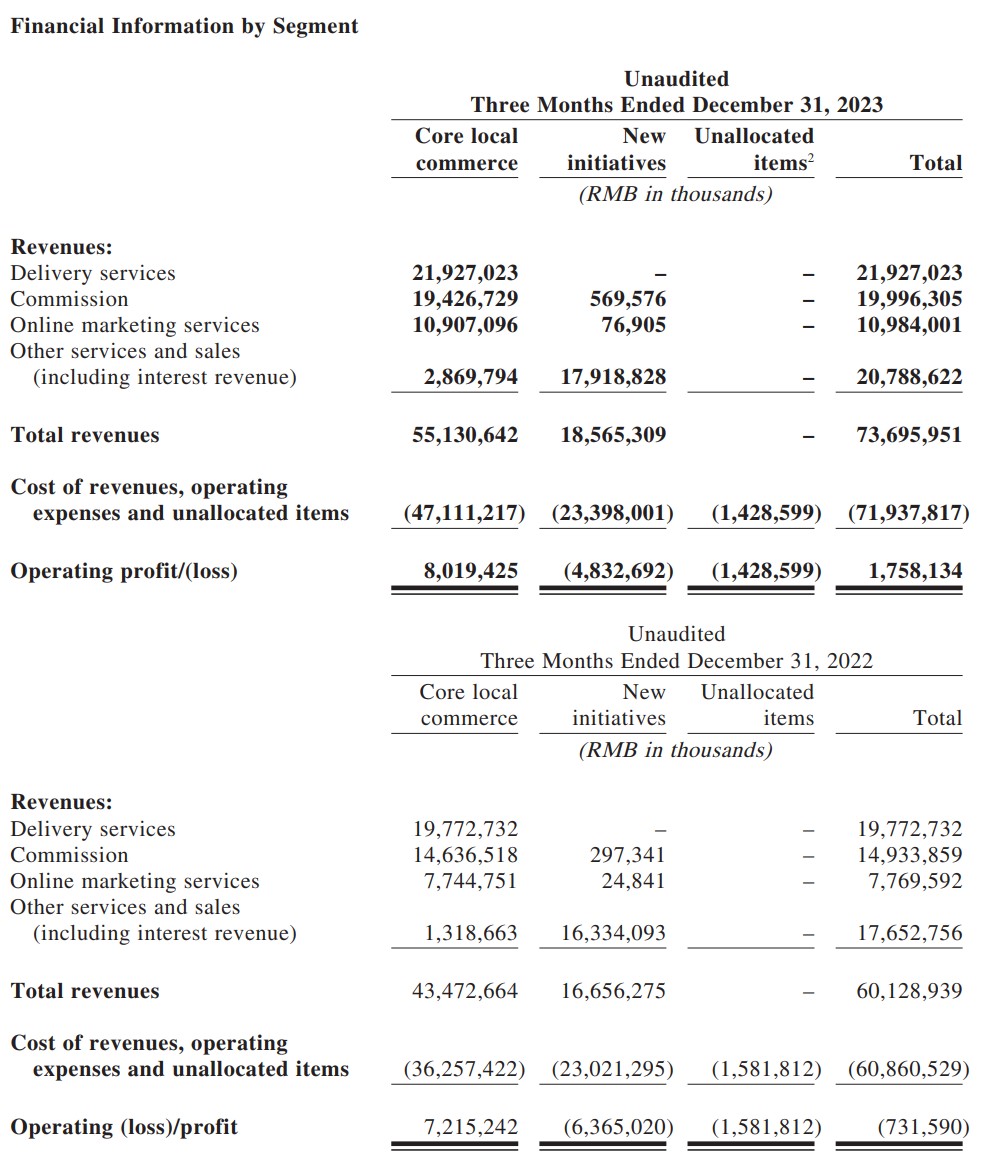

1. 從打天下到治天下:美團在Q4的營業收入為737億人民幣,YoY增長23%;Adjusted EBITDA為37億人民幣。美團在中國目前已覆蓋超過2,800個縣市、數百萬商家與7億位消費者,反映在即時配送交易(餐飲外賣+閃購)的訂單數上,Q4共60.5億筆,YoY增長達25%,若與Uber的Q4總訂單數26.0億筆相比,若假設Uber的網約車訂單數與配送訂單各佔一半,美團的配送訂單約為Uber的3.6倍,已屬全球級別的規模。而從其與抖音在到店業務的競爭來看,去年底以來,抖音組織架構頻繁調整,美團則在今年2月大幅變動組織架構,從組織變動的內容來看,這兩家互為競爭的公司已開始有了不同的做法,這或許意味著行業將趨於穩定,行業最緊張的時期已不再;而美團到家事業群、到店事業群、美團平台、基礎研發等單位整合,並向王莆中匯報(而非各自向王興匯報)這點,可以理解為美團的用人重心從韓信(打天下)到蕭何(治天下)的重大轉變。

2. 酒旅增速估與攜程接近:依公告,2023年到店酒旅交易金額YoY增長超過100%,其中境內酒店交易額YoY增長也超過100%。美團未單獨公告酒旅部分人的交易額、收入與間夜量,不過若將美團交易額增速100%與攜程在Q4的整體收入增速100%相比,我們認為兩者的增速較為接近,也都優於行業平均增速。

3. 承認新業務拓展艱難:美團的新業務Q4收入186億,YoY增速12%;運營虧損減少至48億。新業務可理解為創新事業,涵蓋美團優選、美團買菜、餐飲供應鏈快驢、網約車、共享單車、共享電單車、共享充電寶、餐廳管理系統等等。其中最被投資人重視、虧損最大、也最貼近美團願景”30分鐘萬物到家”的,自然是美團優選;公司在財報中承認,規模增長低於預期,導致難以大幅降低件均履約成本,且激烈競爭使得提高商品加價率和降低補貼的難度加大,將進行戰略調整,以大幅減少經營虧損。海擇資本認為,公司沒有說的是,基於當前地緣政治變動引發的中國宏觀經濟變局,用戶生命周期的購買力已與過往假設不同,這導致通過大額補貼淘汰競品,再通過加價賺回虧損的原有競爭模型已不再適用,未來美團提升商品加價率並降低補貼的舉措,未必會讓客源大幅流失,但整個線上食雜甚至生活服務市場版圖的潛在市場都已大幅下滑,這會衝擊公司的估值上限(儘管已經反映)。

4. 無人配送屬長期戰略價值:本次電話會議也說明了無人機與無人車事業直接向CEO王興匯報的原因。固然如電話會議所說,無人配送技術可能將線上產品滲透提高2-3倍甚至10倍,但完成"30分鐘萬物到家"時代趨勢的載體,肯定還是以人工為主;做為公司的自主式投資,無人配送技術的完善,還需要更多的實驗,時間長度甚至可能以10年為單位,CEO直接領導固然是基於靈活與效率的考慮,從另一個角度看,也唯有CEO能為時間長度達到10年的投資負責,這與攜程梁建章主持投資超音速客機製造商Boom Supersonic的邏輯一致。

------

Meituan: Organizational restructuring is a historic summary in response to the macro environment and competitive landscape.

Meituan (HK: 3690) previously released its Q4 and full-year 2023 financial reports, marking its first return to profitability since 2021, which can be seen as a response to organizational changes in February. The current geopolitical tensions between China and the USA significantly impact Meituan's user lifecycle purchasing power, which has greatly diverged from assumptions made in 2019. This represents a significant challenge faced by most companies tied to Chinese consumer markets. In light of the new macroeconomic environment and competitive landscape, Meituan's organizational adjustments and resource allocation are more crucial than the financial data itself. Haize Capital has highlighted the following key points from this financial report:

1. From Expansion to Management: In Q4, Meituan's revenue was 73.7 billion RMB, a 23% year-over-year increase, with an Adjusted EBITDA of 3.7 billion RMB. Meituan currently serves over 2,800 cities and counties, millions of merchants, and 700 million consumers in China. The volume of instant delivery transactions (food delivery + quick purchases) in Q4 totaled 6.05 billion orders, a 25% increase year-over-year. Assuming Uber's Q4 total orders were split evenly between ride-hailing and delivery, Meituan's delivery orders would be approximately 3.6 times that of Uber's, reaching a global scale. Since the end of last year, Douyin has frequently adjusted its organizational structure while Meituan significantly restructured in February, signaling a possible stabilization within the industry.

2. Hotel and Travel Growth Comparable to Trip.com: According to the announcement, the transaction amount for Meituan's in-store hotel and travel services grew over 100% year-over-year in 2023, with domestic hotel transactions also increasing by more than 100%. Although specific transaction volumes and revenues for the hotel and travel segment were not disclosed separately, comparing Meituan's growth rate with Trip.com's 100% revenue increase in Q4 suggests similar performance, outpacing the industry average.

3. Acknowledging Challenges in New Business Ventures: In Q4, Meituan's new business segments generated revenue of 18.6 billion RMB, with a 12% year-over-year increase, and operational losses reduced to 4.8 billion RMB. These segments include various innovations such as Meituan Select, Meituan Grocery, the restaurant supply chain service Kuailv, ride-hailing, shared bikes, shared electric bikes, shared power banks, and restaurant management systems. The report admits that scaling challenges have hindered the reduction of per-unit fulfillment costs and that intense competition makes it difficult to increase mark-up rates and reduce subsidies, leading to strategic adjustments to significantly cut losses. Haize Capital notes that the changing geopolitical landscape affecting China's macroeconomic conditions has shifted consumer purchasing power away from previous assumptions, making the previous competitive model of eliminating competitors through subsidies and recovering losses through price increases less applicable. Future strategies to increase mark-up rates and reduce subsidies may not necessarily lead to significant customer loss, but the potential market for online groceries and even broader lifestyle services has significantly declined, impacting the company’s valuation ceiling (although already reflected).

4. Long-term Strategic Value of Autonomous Delivery: The earnings call also explained why drone and autonomous vehicle projects report directly to CEO Wang Xing. As stated, autonomous delivery technology could potentially increase online product penetration by 2-3 times or even 10 times, but the primary delivery method will still be human-driven. As a proprietary investment, perfecting autonomous delivery technology requires extensive experimentation, potentially spanning a decade. Direct leadership by the CEO ensures flexibility and efficiency, and only the CEO can be accountable for investments spanning such a long period, similar to Trip.com's Liang Jianzhang overseeing investments in supersonic aircraft manufacturer Boom Supersonic.

標籤 Label: HK: 3690 Meituan TikTok Trip.com Uber