登錄

選單

登錄

海擇短評 Haize Comment:

此前海擇觀點談過美國紐約聯邦儲備銀行(Federal Reserve Bank of New York)所披露的"美國家庭債務與信用報告",談到美國家庭節節上升的各項債務總額與拖欠率。疫情以來,美國與東亞家庭的消費意願與存款率背道而馳,一般將此歸類為文化,也認定是不證自明的事實,這次我們通過更新數據,也思考看看是否有其他的因素的影響。

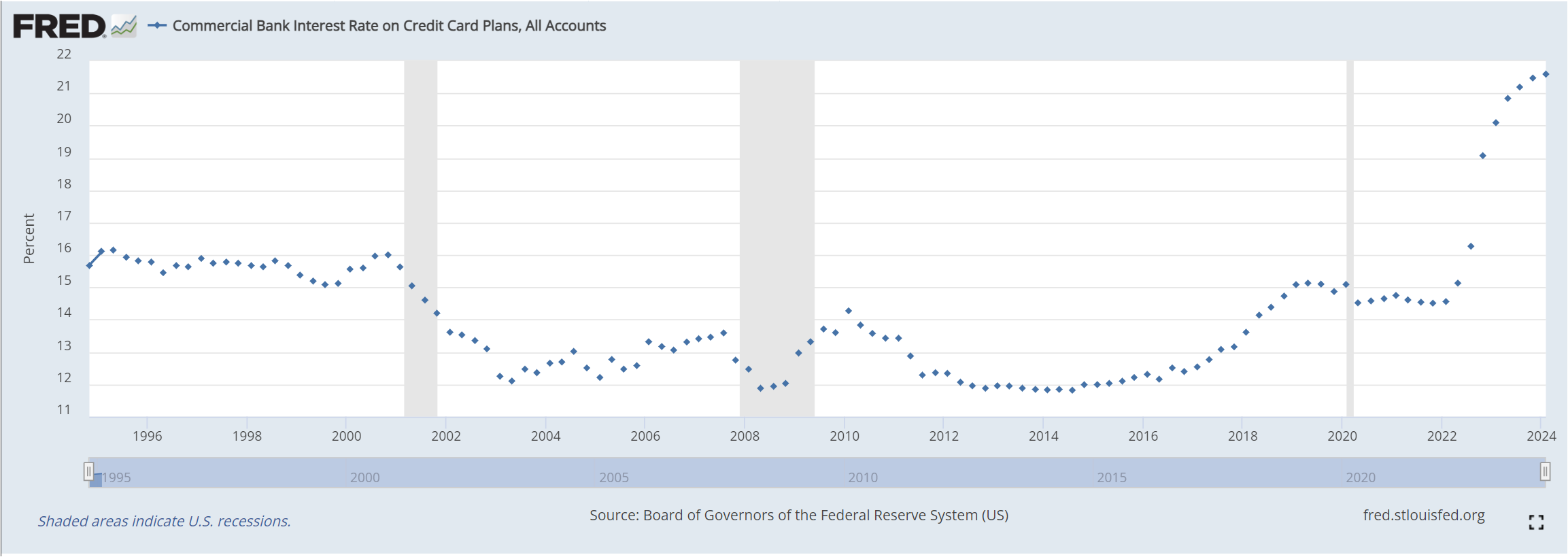

根據美聯儲備最新公告的2月數據,美國家庭的消費仍然在高信用卡循環信貸總額與高信用卡循環利率的方向越走越遠。雖然在兩個月前(2023年12月底),我們見證了美國前所未有的債務增長停滯,亦即,循環信貸(即信用卡)僅增長10億美元(後來修正為40億美元),以及非循環信貸(即汽車貸款和學生貸款)縮減接近10億美元;但是1月份又回歸了美國常態,消費者總信貸單月激增195億美元,2月份消費者總信貸又增加了141億美元,而在循環信貸總額不斷創歷史新高的過程中,2月的信用卡循環信貸利率也增長到21.59%,再創歷史新高。與此同時,美國人的儲蓄率也從疫情期超過36%的高點,萎縮為1/10到3.6%,創下歷史新低。從美國人在信貸與儲蓄不斷創下歷史紀錄的相關數據,我們大致可以描繪出美國社會蓬勃的消費動能。

過往我們已習於用文化的刻板印象,解釋美國消費者的超前消費行為,也認定東亞國家民族性就是高儲蓄率,愛存錢,並把這些刻板印象肇因於對經濟前景的信心,而歸咎到信心就很難以科學數據看待了。但從另一個角度看,這其實也跟信用卡公司的風控嚴格程度及風險轉嫁能力相關,違約壞帳不會消失,但是可以通過衍生性商品轉嫁到其他產品,甚至分散到其他國家的購買者甚至貨幣體系承擔,歸根究底,這是金融體制帶給美國家庭的優勢。如果有學術研究探討這一點,倒應該是有很多量化數據可供分析。

-------

Previously, Haize Capital discussed the "Household Debt and Credit Report" released by the Federal Reserve Bank of New York, which talked about the rising total debt and delinquency rates of American households. Since the pandemic, the consumption tendencies and savings rates of families in the US and East Asia have diverged, commonly attributed to cultural reasons and considered self-evident facts. In this update, we also consider whether there are other influencing factors.

According to the latest data from the Federal Reserve for February, American household consumption continues to move away from high credit card revolving balances and interest rates. Although we witnessed an unprecedented stagnation in debt growth at the end of December 2023, with revolving credit (i.e., credit cards) increasing only by $1 billion (later revised to $4 billion), and non-revolving credit (i.e., auto and student loans) shrinking by nearly $1 billion, January saw a return to the usual American pattern with a surge of $19.5 billion in total consumer credit, followed by an additional $14.1 billion in February. During this period of record highs in revolving credit totals, the credit card revolving interest rate also reached a new historical peak at 21.59% in February. Concurrently, the American savings rate plummeted from a pandemic high of over 36% to a historic low of one-tenth to 3.6%. From these data on credit and savings continually setting new records, we can roughly outline the vigorous consumer momentum in American society.

We have traditionally used cultural stereotypes to explain the aggressive spending behavior of American consumers and have attributed high savings rates and frugality to East Asian national characteristics, associating these stereotypes with confidence in economic prospects, which is hard to measure with scientific data. However, another perspective links this also to the strict risk control and risk transfer abilities of credit card companies. Defaults and bad debts do not disappear but can be transferred to other products through derivatives, or even dispersed to buyers in other countries and absorbed by their currency systems. Ultimately, this represents a financial advantage provided by the system to American households. If academic research were to explore this, there would likely be ample quantitative data available for analysis.

標籤 Label: Federal Reserve Bank of New York Consumption Debt Saving