登錄

選單

登錄

海擇短評 Haize Comment:

Expedia(NASDAQ: EXPE)近期公告2024Q1季報,由於管理層在電話會議時,將全年收入成長率的財測降低到個位數,即便公司宣稱將繼續從公開市場回購股票,今年迄今也已回購約570萬股,市值再次迎來了超過10%的大跌。對此,海擇資本認為,在Expedia從基本面得到投資市場認同之前,投資人可以觀察三個領域的進展,亦即,B2B事業能否再創Expedia的下一程、One Key的整合效益能否突顯、B2C事業的價值能否被內部重視。海擇資本整合並分析電話會議的相關表述如下:

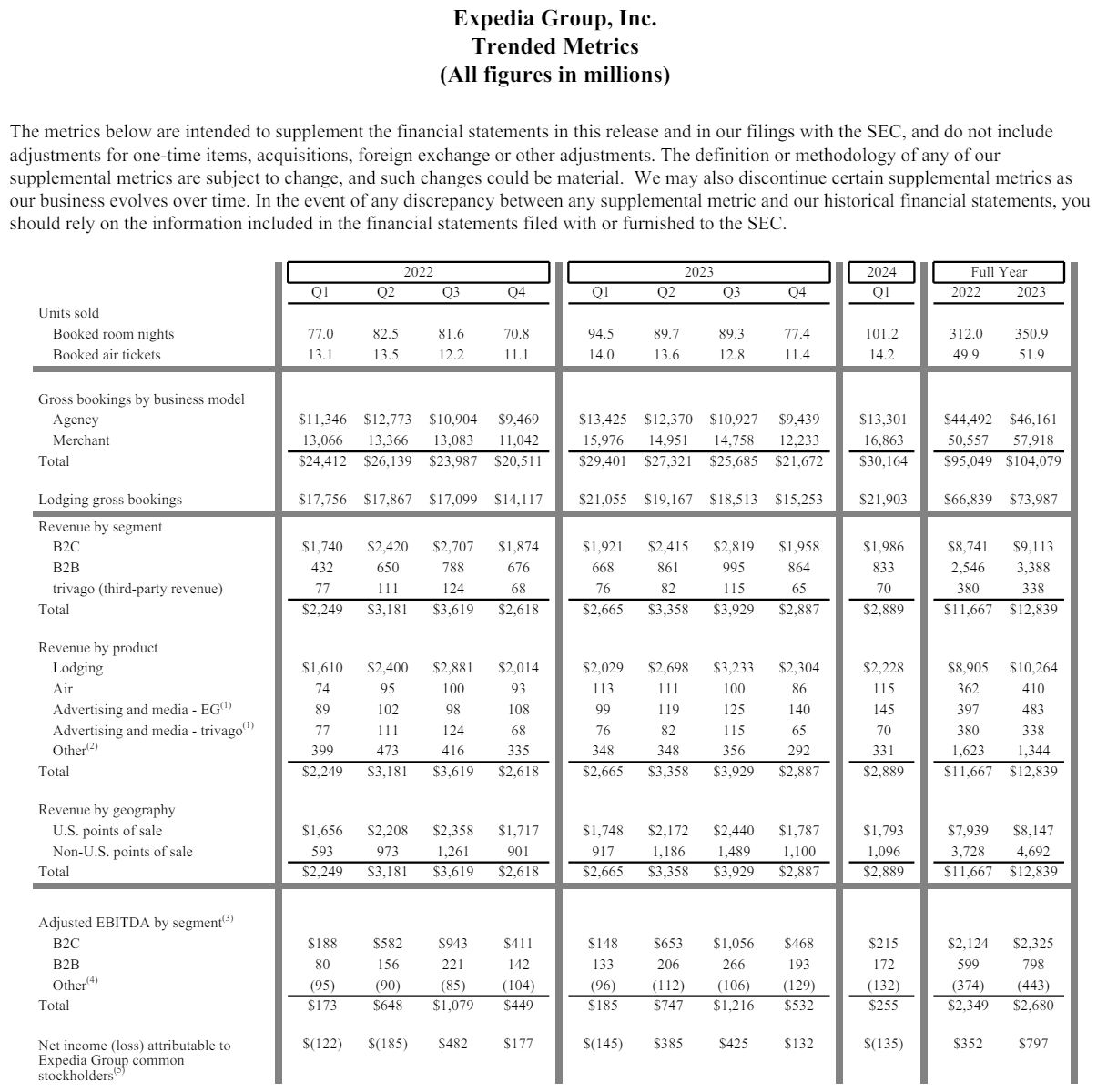

1. B2B事業仍難超越B2C:5月將上任的新CEO將由現有的"Expedia for Business"的負責人Ariane Gorin接任。海擇資本此前談過,公司自疫情以來,將B2B視為Expedia的第二成長曲線,除了認為潛在市場巨大,也有個考慮是,雖然B2B在直接行銷要支付的行銷費用(給分銷商的佣金)佔收入的百分比較B2C更昂貴,但B2B要成交才需要支付佣金,B2C則要考慮轉化率。雖然從收入的YoY增速看,B2B相對於B2C是增長的,近五季B2C增速分別為10%、0%、4%、4%、3%,而B2B則分別為55%、32%、26%、28%、25%,增速明顯較高;但從絕對值看,現在B2B的收入僅為B2C的35%-40%間,若B2B要超過B2C成為Expedia的核心本業,推估至少要五年,並不是馬上能超越B2C的產品線。

2. One Key效益不如預期:被公司寄託為"新Expedia"最大殺手鐧的"One Key"功能,在功能整合完成後,目前效益尚不如預期。原本公司認為當用戶能用One Key累積不同Expedia系的消費積分,同時降低新客戶獲取成本與增加老客戶留存率,用一次性的技術投入取代例行的行銷投入是很划算的。但目前來看,整體效益尚不如預期,舉例來說,Hotels.com或Expedia上積累積分的會員,雖有25%成為Vrbo的新客,但Vrbo客戶出行頻次不高,他們可能每一年甚至兩年才旅行一次。目前來看,最糟糕的狀況是,Expedia雖然用了一年多時間與龐大成本整合One Key,但為了獲取新客,未來可能B2C行銷費用仍然得加回,除非B2B的增速非常好,導致Expedia能把B2C的行銷ROI定到非常高,比如2或是更高。

3. B2C競爭待新切入點:疫情以來Expedia更重視盈利,而非市場份額(間夜產量),雖然每季的EBITDA從年化來看都再創新高,但每季的間夜數也從疫情前能做到Booking(NASDAQ: BKNG)的一半,到現在固定只有Booking的三分之一。目前看來,Expedia死守毛利不降,在美國本土的酒店產量仍能不錯,但其他領域受創就大了;首先國際化程度較高的Hotels.com,面對Booking旗下的Agoda在低價上積極搶攻;其次是非標準住宿領域,Airbnb(NASDAQ: ABNB)和Booking在低客低價產品的布局都很積極,但Vrbo還停留在疫情期的高客單價領域。Expedia仍然預計2024年B2C業務會廣泛出現改善,我們則認為改善還仰賴公司願意在國際市場進行多大產品與行銷層面的投入。

-------

Expedia (NASDAQ: EXPE) recently released its Q1 2024 earnings report. Despite plans to continue buying back shares from the open market, having repurchased approximately 5.7 million shares this year, the stock fell over 10% after management lowered the full-year revenue growth forecast to single digits during the earnings call. In response, Haize Capital suggests that investors should monitor progress in three areas before Expedia gains market confidence: the potential of its B2B segment to drive the next growth phase, the integration benefits of One Key, and the internal valuation of the B2C business. Haize Capital has summarized and analyzed statements from the earnings call as follows:

1. B2B still trails B2C: The incoming CEO, Ariane Gorin, currently heading "Expedia for Business," will take over in May. Haize Capital has noted that since the pandemic, the company has viewed B2B as Expedia's second growth curve due to its large potential market. Although B2B's direct marketing costs (commissions to distributors) are a higher percentage of revenue compared to B2C, commissions are only paid upon transactions in B2B, whereas B2C must consider conversion rates. While B2B has shown higher growth rates YoY relative to B2C—with B2B growth rates in the last five quarters at 55%, 32%, 26%, 28%, and 25%, compared to B2C’s 10%, 0%, 4%, 4%, and 3%—in absolute terms, B2B's revenue is currently only 35%-40% of B2C's. To surpass B2C as Expedia's core business, it is estimated that it would take at least five years, and it is not immediately positioned to overtake the B2C product line.

2. One Key benefits below expectations: The "One Key" feature, touted as the trump card for the "new Expedia," has underperformed following its integration. Initially, the company believed that allowing users to accumulate points across different Expedia services while reducing acquisition costs for new customers and increasing retention rates for existing ones would be cost-effective, replacing routine marketing expenditures with a one-time tech investment. However, the overall benefits have not met expectations. For instance, although 25% of members accumulating points on Hotels.com or Expedia became new customers for Vrbo, these customers do not travel frequently—often only once every year or two. Currently, the worst-case scenario is that despite spending over a year and significant resources integrating One Key, Expedia may still need to increase B2C marketing expenses to attract new customers unless B2B grows substantially, allowing Expedia to achieve a very high marketing ROI.

3. B2C competition seeks new entry points: Since the pandemic, Expedia has prioritized profitability over market share (measured by room nights). While quarterly EBITDA has consistently reached new highs annually, room nights have dropped from half of Booking's (NASDAQ: BKNG) pre-pandemic levels to just one-third now. Currently, Expedia maintains its gross margin without compromising its strong performance in U.S. domestic hotel bookings, but struggles more in other areas. First, Hotels.com, which has a higher degree of internationalization, faces aggressive low-price competition from Booking's Agoda. Secondly, in the non-standard accommodations sector, both Airbnb (NASDAQ: ABNB) and Booking are actively expanding their low-cost offerings, whereas Vrbo remains focused on the high-cost niche from the pandemic period. Although Expedia anticipates widespread improvements in B2C operations in 2024, we believe any significant improvement will depend on how much the company is willing to invest in product and marketing efforts in international markets.

標籤 Label: EXPE One Key B2B B2C BKNG ABNB