登錄

選單

登錄

海擇短評 Haize Comment:

中國在線旅遊公司途牛(NASDAQ: TOUR)近期公告2024Q1財報,公司首次達到GAPP會計準則下的盈利,並在以直播為核心銷售通路的路上繼續前進,雖然銷售規模的恢復速度弱於同業,但後疫情時代途牛的新常態已與疫情前不同。海擇資本節選觀察要點如下:

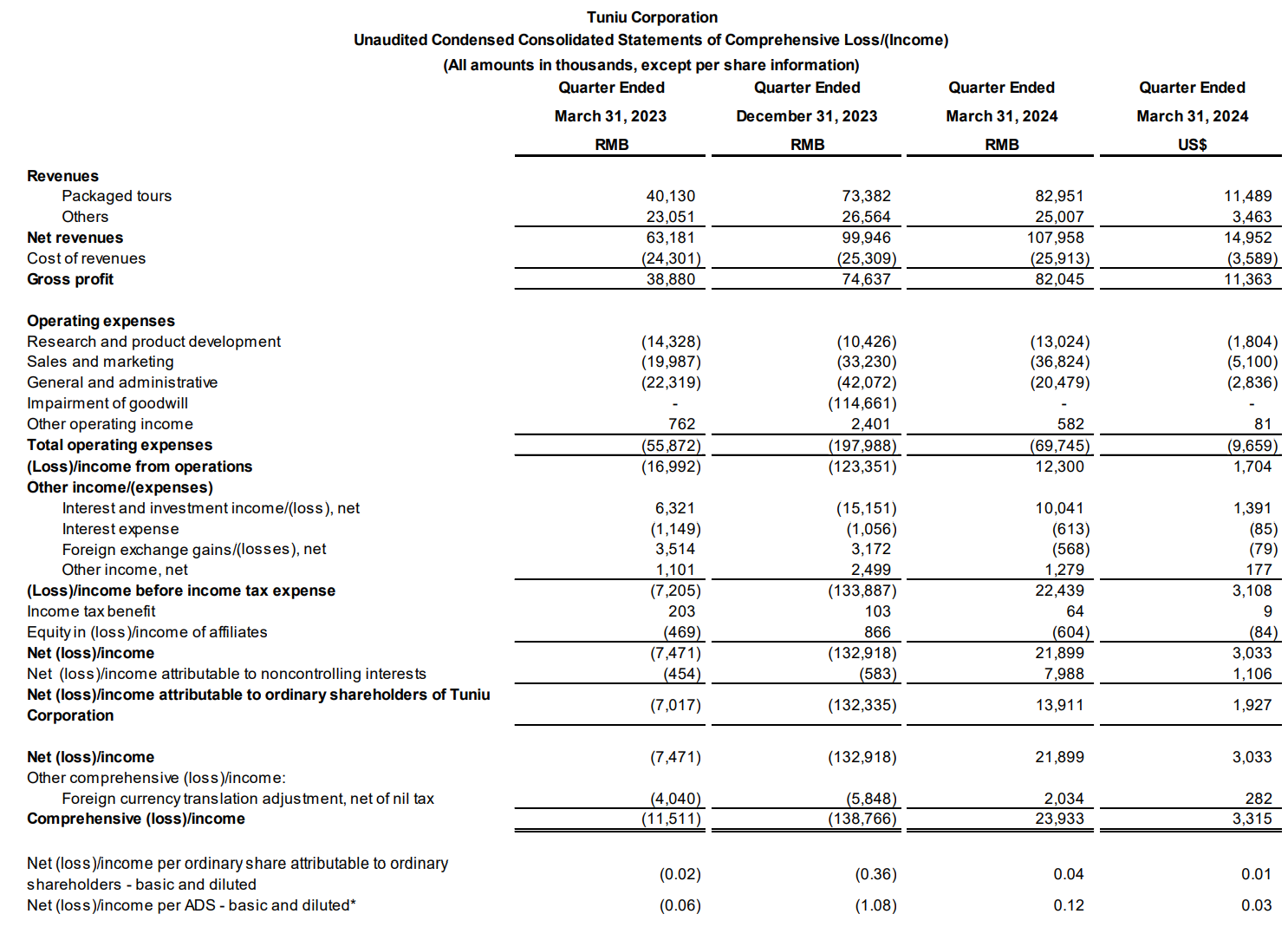

1. 途牛首次GAPP轉盈:Q1途牛首度在GAPP會計準則下,運營利潤與淨利雙雙虧轉盈,分別為1,230萬人民幣與2,190萬人民幣。由於本季收入1.08億人民幣僅為2019年同期的24%,從財務看,盈利的主因還是在費用上控制得宜,研發、行銷與管理費用,分別只有2019年同期的14%、17%、15%。公司說明五一假期出境旅遊產品的交易額較去年同期成長超過200%,但考慮到2022年的基數相對於2019年已經很小,未來重點還是看公司能用什麼方式放大團隊遊產品的盈利能力。

2. 積極聚焦直播通路:途牛目前雖仍經營約200家線下門市,也開發各類通路,比方也是支付寶交通的旅遊供應商之一,但是在直播上最為積極,可以理解為首家以直播為核心銷售通路的OTA。途牛的MCN機構在抖音上擁有60個內部直播帳號,與超過1000名網紅合作;公司針對直播形式增加了團隊遊與目的地產品的靈活性,比如機票實施了非捆綁政策,讓客人可以選擇適合與偏好的交通和住宿。今年1-5月,途牛直播通路支付總額年增超過200%,訂單核銷量增加400%。不過,直播的真實成本不低,抖音的算法傾斜性也不無改變的可能,這部分較難具體預估成長數據。

3. 型塑專精於團隊遊的新常態:從途牛財報與電話會議,大體可以勾勒出後疫情期途牛的新形象。亦即,相對於攜程Q1團隊遊收入恢復到2019年同期的84%,而途牛的恢復率不到25%,它的規模可能很難回到2019年。但目前看來,它已圍繞團隊遊產品建立了新常態;從產品結構與收入上看,它不會走向類似攜程的一站式,最多是沿著團隊遊產品的組成,出售有庫存/價格優勢的資源(住宿/包機機票等)或附加產品(保險等);即便中國出境遊恢復速度不會很快,但途牛仍然可以一定程度捕捉國內旅遊的團隊客人(依Q1收入組成,國內遊佔GMV約70%,出境遊佔30%);它會更專注於自營產品,這可能導致最後售出的自營產品會偏高端,因為需要更高的利潤率;最後,它也必須續續用系統和自動化技術嚴格做費用控制。即便它會有很長一段時間不會恢復到2019年的規模,但在財務體質上會比過去更為健康(如果直播通路沒有問題的話)。

-------

Chinese online travel company Tuniu (NASDAQ: TOUR) recently announced its Q1 2024 financial results, marking its first profitability under GAAP standards. Despite slower sales recovery compared to peers, the post-pandemic "new normal" for Tuniu has changed from pre-pandemic times. Key observations from Haize Capital include:

1. Tuniu's first GAAP profitability: In Q1, Tuniu achieved profitability under GAAP for the first time, with operating and net profits of 12.3 million RMB and 21.9 million RMB, respectively. With revenue of 108 million RMB, only 24% of the same period in 2019, profitability was primarily due to effective cost control, with R&D, marketing, and administrative expenses at only 14%, 17%, and 15% of their 2019 levels, respectively. The company reported over 200% growth in outbound travel transactions during the Labor Day holiday compared to last year. Given the base in 2022 was much lower than in 2019, the focus remains on how the company can enhance the profitability of group travel products.

2. Focus on live streaming channels: While Tuniu still operates about 200 offline stores and develops various channels, such as being a travel supplier for Alipay's transportation service, it is most active in live streaming, positioning itself as the first OTA to focus on live streaming as a core sales channel. Tuniu's MCN agency manages 60 internal live streaming accounts on Douyin and collaborates with over 1,000 influencers. The company has increased the flexibility of group travel and destination products through live streaming, implementing unbundled ticketing policies that allow customers to choose preferred transportation and accommodations. From January to May this year, Tuniu's live streaming channel saw a payment total increase of over 200% and a 400% rise in order fulfillment. However, the true costs of live streaming are not insignificant, and potential changes in Douyin's algorithms make it difficult to precisely predict growth figures.

3. Shaping a new normal for group travel: Tuniu's financial reports and conference calls outline its post-pandemic transformation. While Trip.com's Q1 group travel revenue recovered to 84% of its 2019 levels, Tuniu's recovery was less than 25%, suggesting it may not return to its 2019 scale. However, Tuniu has established a new norm around group travel products; unlike Trip.com's one-stop-shop approach, Tuniu focuses on selling resources with inventory/price advantages (such as accommodations or chartered flights) or add-ons (like insurance). Even if the recovery of outbound travel from China is slow, Tuniu can still capture domestic group travel (as of Q1, domestic travel accounted for about 70% of GMV, with outbound at 30%). It is focusing more on proprietary products, likely skewing towards the higher-end due to the need for higher profit margins. Finally, it must continue to rigorously control costs through systems and automation. While it may not return to its 2019 scale for some time, Tuniu's financial health could improve, assuming its live streaming channel faces no issues.

標籤 Label: NASDAQ: TOUR Live Streaming Group Tour OTA