登錄

選單

登錄

海擇短評 Haize Comment:

美團(HK: 3690)近期公告2024Q2財報,經營溢利再創新高的同時,也出現飛躍式的增長,且增長同時基於核心本地商業的降本增效與新業務的成功減虧,可說是幾無缺點的成績單。美團的成功,創造了"零售+科技"在當前經濟低迷時期的新時代意義,而做為一家單季能盈利15億美金的企業,它將無可避免的在提供股東投資報酬外,還必須做為典範,成為企業社會責任與互聯網監管的觀察指標。海擇資本簡述觀點如下:

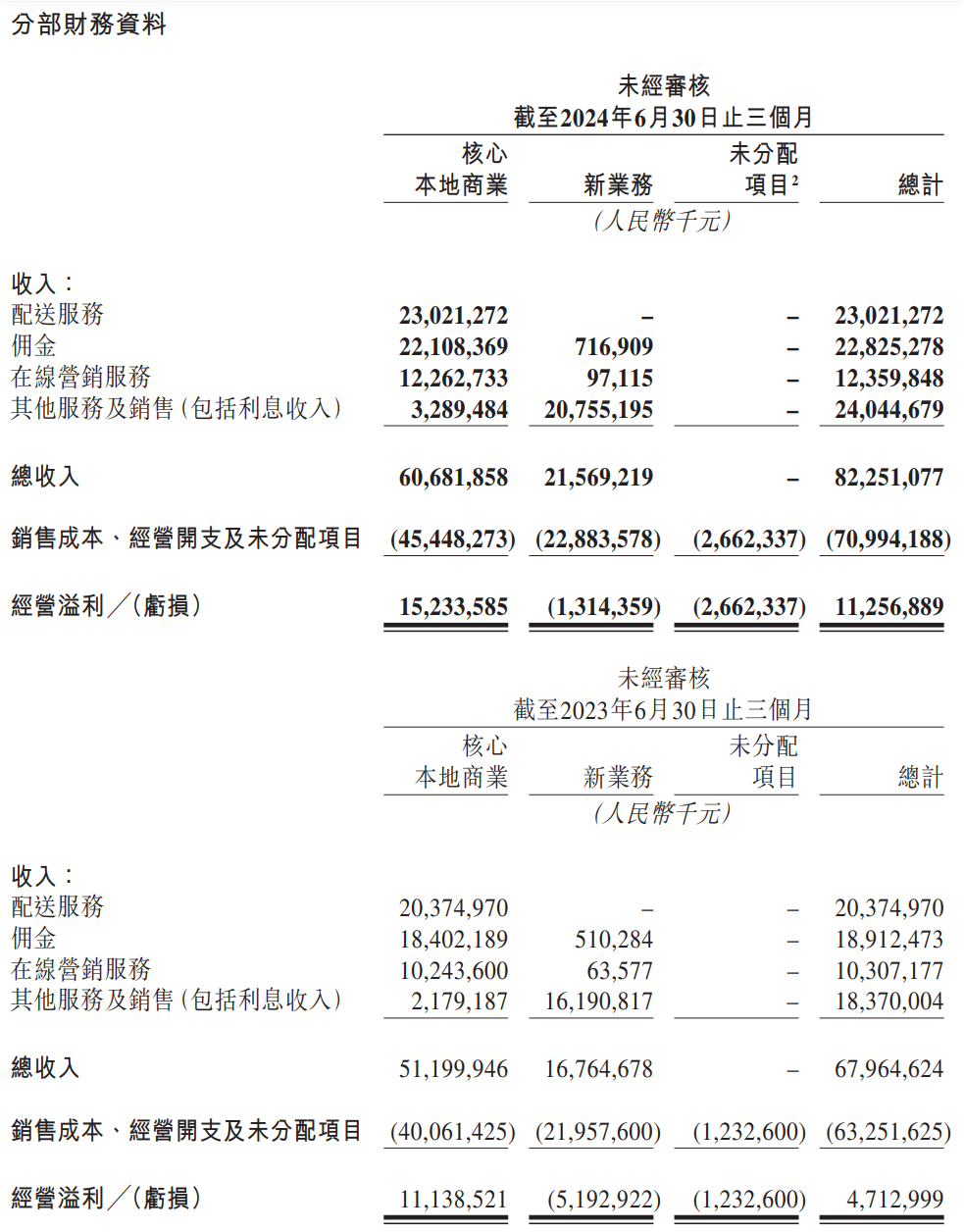

1. 無可批評的創新高成績單:本季美團的財務數據出現飛躍式的增長,總收入YoY增長21%、QoQ增長12%至823億人民幣;經營溢利YoY增長139%、QoQ增長116%,達113億人民幣,雙雙創下歷史新高。分解來看,核心本地商業板塊收入YoY增加18.5%,而經營溢利增加37%,表示成本/費用控管嚴格;新業務在收入增長41%之際,虧損大幅降低,本季經營虧損為13億人民幣,整整比2023年同期減少39億人民幣(75%)。這意味著外部經濟降溫之際,公司在各種消費場景精細化運營,成功提供用戶能接受的低價(也可說是高性價比)產品,帶動用戶增加購買頻次。

2. 對低單價的住宿有控制力:此前我們談過美團的組織架構變動,其中之一的變化體現在多項業務的交叉整合。除了"神會員"計畫,在旅遊與住宿的場景,整合了外賣配送、到店業務。在消費者能感知的層面,就是"酒+X"的打包比OTA更多元,OTA的"酒+X"打包的是用車/門票/機票,美團延伸到外賣/配送;在消費者感知不到的層面,美團則嘗試打入商戶的採購供應鏈。對住宿業主來說,美團從流量獲取到客房裝修都能提供一定的資源,對ADR越低(1間夜低於100人民幣甚至低於50人民幣)的業主影響越大,甚至可以壓制攜程(NASDAQ: TCOM);而對ADR高的中高星酒店來說,一方面外賣的補貼相對競品更便宜的間夜單價不具吸引力,一方面有自己的供應鏈,影響較低。但回歸當前經濟情勢,對低單價的住宿有控制力已能形成巨大的槓桿。

3. "零售+科技"策略的新時代意義:美團所說的"以零售+科技戰略,幫助人們吃得更好、生活更好的使命",在當前的經濟情勢下,海擇資本認為有了新的產品戰線與效果。無論是"神會員"、"團好飯"、"特價團"、"神搶手",這些活動除了拉新/拉活外,目的都是(將原有產品)以更低的價格服務用戶。如果說Uber(NYSE: UBER)藉美國經濟不景氣情勢更好的控制了供給端(司機);美團則在需求端以餐飲產品為始,延伸到生活的方方面面,以價生量,刺激了龐大的消費降級需求。本季各消費品類和場景,平均訂單量年增近40%,對應比核心本地商業板塊收入年增19%,可以想見刺激初多大的需求;容或訂單單價可能降低,但是ARPU呈現爆發式增長。若將Uber與美團對比,Uber與美團在 MAPC(Monthly Active Platform Consumers)的數量級是類似的,但Uber本季運營利潤為7.97億美金,美團則為15.86億美金,美團幾乎翻倍。

4. 美團難以只做提供股東報酬的美團:中概股的低PE現象並非只發生在美團,這是地緣政治影響下的Collateral Damage;儘管如此,美團正在努力用自己的方式帶給股東回報,年初至今回購了已發行股份總數的3.6%,董事會並批准了另一項10億美元的回購計劃。不過,在全球地緣政治混沌不安、各國政治力監管頻仍的背景下,美團做為生活服務類公司,其創立/存在/被罰款/增長的歷史,本身就是一個企業社會責任與互聯網監管的觀察指標,也是巨大且絕無僅有的社會學實驗典範,這可能還是長達數十年的現在進行式。未來它被要求的不會只有ESG,也不可能只做到所謂"快遞友善社區通行解決方案",就能得到認可。它會是一個且值得研究的動態標的,且並非只對買方與賣方分析師有價值。

-------

Meituan (HK: 3690) recently announced its Q2 2024 financial report, showcasing record-breaking operating profits and remarkable growth. This growth stems from cost optimization in core local commerce and successful loss reduction in new businesses, making it a near-flawless performance. Meituan's success has defined a new era for "retail + technology" during economic downturns. As a company earning $1.5 billion in quarterly profits, Meituan is not only providing shareholder returns but also becoming a benchmark for corporate social responsibility and internet regulation. Haize Capital offers the following insights:

1. **Impressive, Record-High Performance**: Meituan’s financials showed explosive growth, with total revenue increasing 21% YoY and 12% QoQ to 82.3 billion RMB. Operating profit grew 139% YoY and 116% QoQ to 11.3 billion RMB, both reaching record highs. Core local commerce revenue increased 18.5% YoY, with operating profit up 37%, indicating strict cost control. New business revenue grew 41%, while losses decreased significantly. Operating losses dropped to 1.3 billion RMB, 3.9 billion RMB less than in Q2 2023 (a 75% reduction). This shows that despite external economic slowdowns, Meituan has refined its operations across various consumption scenarios, offering high-value products that drive increased purchase frequency among users.

2. **Control Over Low-Priced Accommodation**: Previously, we discussed Meituan's organizational changes, including cross-integration of multiple businesses. One significant change is seen in the tourism and accommodation sectors, where Meituan integrates food delivery and in-store services. For consumers, Meituan offers more diverse "Hotel + X" packages compared to OTAs, which typically bundle hotel stays with transport, tickets, or flights. Meituan extends these packages to include food delivery. Behind the scenes, Meituan is also penetrating the procurement supply chain of merchants. For hotel owners, especially those with low average daily rates (ADR) below 100 RMB or even 50 RMB, Meituan offers resources ranging from traffic acquisition to room renovations, giving it leverage over competitors like Trip.com (NASDAQ: TCOM). For mid-to-high-end hotels with higher ADRs, Meituan's cheaper delivery subsidies have less appeal, as these hotels often have their own supply chains. However, given the current economic environment, Meituan’s control over low-priced accommodation creates significant leverage.

3. **New Era Significance of the "Retail + Tech" Strategy**: Meituan’s mission of "improving people's lives through retail and technology" has taken on new meaning in the current economic climate, according to Haize Capital. Initiatives like "Shen huiyuan," "Tuan haofan," "Tejia tuan," and "Shenqiangshou" aim not only to attract and retain users but also to offer lower-priced services for existing products. While Uber (NYSE: UBER) has leveraged the U.S. economic downturn to better control supply (drivers), Meituan has focused on the demand side, starting with food and expanding into all aspects of life, meeting massive demand for consumption downgrades through lower prices. This quarter, the average order volume across categories increased by nearly 40% YoY, compared to a 19% revenue growth in core local commerce, indicating significant demand stimulation. While order values may have decreased, ARPU has seen explosive growth. Comparing Uber and Meituan, both have similar Monthly Active Platform Consumers (MAPC), but Uber’s operating profit for the quarter was $797 million, while Meituan’s was $1.586 billion—nearly double.

4. **Meituan Can't Just Focus on Shareholder Returns**: The low PE ratio for Chinese stocks, including Meituan, is largely a collateral damage of geopolitical tensions. Despite this, Meituan is actively working to provide shareholder value, repurchasing 3.6% of its total issued shares this year and approving an additional $1 billion buyback plan. However, in a world of geopolitical instability and frequent regulatory oversight, Meituan, as a lifestyle services company, represents a unique case study in corporate social responsibility and internet regulation. Its history of creation, existence, fines, and growth is a rare sociological experiment that is still unfolding and may continue for decades. In the future, Meituan's expectations will go beyond ESG compliance or implementing "delivery-friendly community solutions." It will remain a dynamic case worth studying, not only for analysts on the buy and sell sides but for a wider audience.

標籤 Label: HK: 3690 Retail Regulation Hotel NASDAQ: TCOM NYSE: UBER