登錄

選單

登錄

海擇短評 Haize Comment:

東亞台日韓地區2024出境遊復甦現況一覽

2024年即將告終,正是各旅遊企業擬定新一年預算的時間。海擇資本於此整理今年東亞台日韓地區的出境遊恢復程度與組團社復甦現況,期待能對行業供應鏈相關環節的業者帶來些幫助。

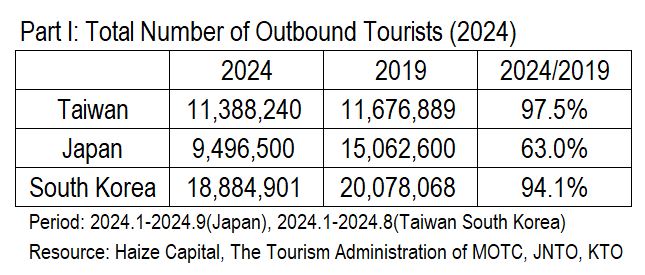

1. 從出境遊的整體恢復現況來看,台灣與南韓兩地累計2024年前8月的總出境人次,都已恢復到2019年的95%上下,分別為97.5%與94.1%。不過,日本的恢復較差,累計前9月僅略超60%,為63%;即便單看9月,仍未達7成,為2019年同期的69.2%。

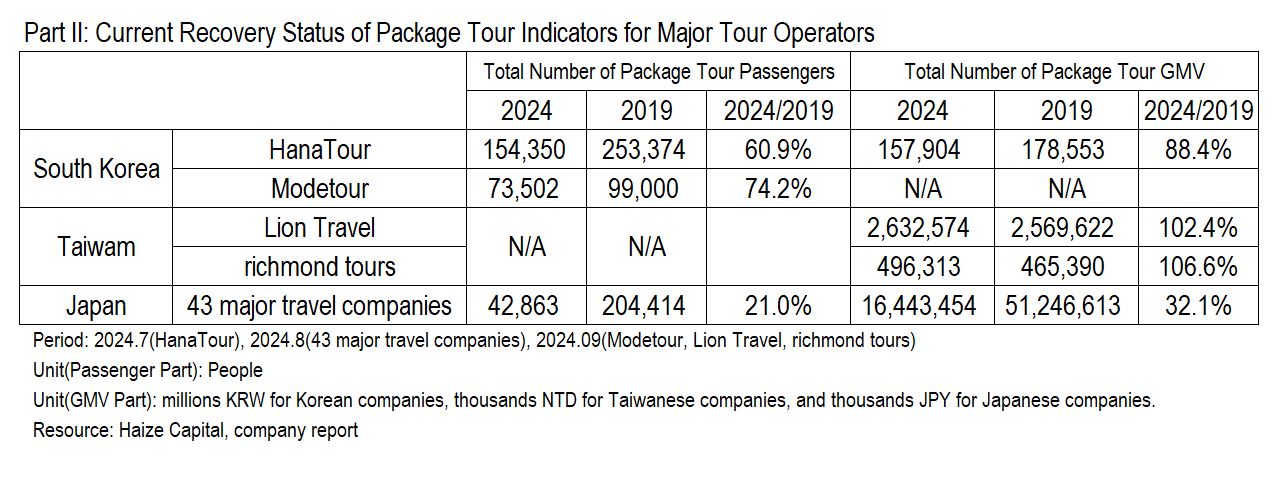

2. 若關注南韓出境組團社的復甦程度,會發現,雖然出境遊總人次已接近完全復甦,但組團社所輸送的團隊旅遊人次則大幅落後,HanaTour與Modetour僅恢復至2019年的60.9%與74.2%。但值得注意的是,交易額的恢復優於輸送人次,HanaTour的出團人次雖然僅為6成,但交易額已達2019年的88.4%,由於出行目的地的佔比在疫情前後差異不大,我們認為這主要反映了通貨膨脹現況。

3. 再看台灣出境遊組團社的復甦程度,若以最新公告的9月單月營收來看,雄獅旅遊與山富旅遊的收入都超過了2019年同期,分別較2019年同期超出2.4%與6.6%;雖然兩家業者都未公告輸送人數,但即便只從交易額的角度看,也能明白台灣的主要組團社復甦程度為日韓台三地最優。

4. 日本的出境遊組團社的復甦程度,我們則以43家主要旅遊社的8月團隊旅遊數據為樣本。43社8月的出境總輸送人次為2019年同期的21.0%,交易額則為2019年同期的32.1%,遠遠不如台韓的復甦現況。考慮到疫情這類重大挑戰會讓行業倖存者大者恆大,我們認為JTB與H.I.S這類大社的運營數據會比43社的平均數據好些,但無法顛覆日本出境遊的孱弱格局。

海擇資本認為,依東亞台日韓出境遊的恢復數據,台韓出行人次今年迄今均已接近2019年的規模,日本則停留在7成左右。若看近期主要組團社的恢復現況,台灣組團社的抗打擊能力較強.可能也與台灣沒有規模特別大的一站式OTA有關;韓國的兩家上市公司在疫情後走向不同的路,HanaTour更像OTA、售出的機票等元件式產品佔比更高了,而Modetour則更專注團隊遊;日本的組團社復甦最弱,韓國組團社輸送人數能達疫情前的6-7成,但日本只剩2成。

------

Haize Capital Insights of the Day

Overview of the 2024 Outbound Travel Recovery in East Asia (Taiwan, Japan, South Korea)

As 2024 draws to a close, it's the time when travel companies are drafting their budgets for the coming year. Haize Capital has compiled the recovery status of outbound travel in East Asia, specifically in Taiwan, Japan, and South Korea, along with the status of group tour operators, with the hope that this will provide some guidance to stakeholders in the travel industry supply chain.

1. Overall Recovery of Outbound Travel

Looking at the overall recovery status of outbound travel, both Taiwan and South Korea have seen cumulative outbound trips in the first eight months of 2024 recover to around 95% of 2019 levels, with Taiwan at 97.5% and South Korea at 94.1%. However, Japan’s recovery is lagging behind, with cumulative outbound trips for the first nine months of 2024 reaching only slightly above 60%, at 63%. Even when looking at September alone, Japan has not yet reached 70%, standing at 69.2% of the same period in 2019.

2. Recovery of South Korean Group Tour Operators

While the total number of outbound trips in South Korea is nearing full recovery, the number of group tour passengers transported by major operators is significantly lower. HanaTour and Modetour have only recovered to 60.9% and 74.2% of 2019 levels, respectively. However, it’s worth noting that transaction volumes have recovered better than passenger numbers, with HanaTour's revenue reaching 88.4% of 2019 levels. Since the destination mix hasn't changed much compared to pre-pandemic, we believe this mainly reflects inflation.

3. Recovery of Taiwanese Group Tour Operators

Turning to Taiwan’s group tour operators, based on the latest revenue figures for September, Lion Travel and Sanfo Travel have both exceeded their revenues from the same period in 2019, with increases of 2.4% and 6.6%, respectively. Although neither company has disclosed the number of passengers transported, even from a revenue perspective alone, it’s clear that Taiwanese group tour operators are showing the strongest recovery among the three regions (Taiwan, Japan, South Korea).

4. Recovery of Japanese Group Tour Operators

For Japan, we used the August group tour data from 43 major travel companies as a sample. The total number of outbound passengers transported by these 43 companies in August 2024 was only 21.0% of the same period in 2019, with transaction volumes reaching 32.1% of 2019 levels. This lags far behind the recovery seen in Taiwan and South Korea. Given the significant challenges posed by the pandemic, which tend to favor larger companies, we believe that large companies like JTB and H.I.S. might show better operational data than the average of these 43 companies, but it will not change the overall weak outlook for Japan’s outbound travel sector.

Conclusion by Haize Capital:

Based on the recovery data for outbound travel in East Asia, both Taiwan and South Korea have seen travel volumes approach 2019 levels, while Japan remains at around 70%. Looking at the recent recovery status of major group tour operators, Taiwan’s operators have shown the strongest resilience, which may also be related to the fact that Taiwan does not have a particularly large one-stop OTA. Meanwhile, the two listed companies in South Korea have taken different paths post-pandemic: HanaTour has shifted more towards selling component-based products like flight tickets, resembling an OTA, while Modetour remains more focused on group tours. In contrast, Japanese group tour operators have shown the weakest recovery, with South Korean operators transporting around 60-70% of pre-pandemic passenger numbers, while Japanese operators have only recovered 20%.

標籤 Label: SouthKorea Taiwan Japan KTO JNTO OutboundTravel MOTC