登錄

選單

登錄

海擇短評 Haize Comment:

Uber不會選擇收購Expedia的三個理由

近日英國金融時報報導了Uber(NYSE: UBER)考慮收購Expedia(NASDAQ: EXPE)一事。考慮到Uber少數細分產品線確實涉入旅遊行業,且做為現任CEO的Dara Khosrowshahi,不僅曾任職Expedia的CEO長達12年,在離任Expedia前,更與Expedia現任董事會主席Barry Diller共事超過26年,顯得收購一事格外可信。即便如此,海擇資本從潛在市場的布局綜效等三個角度來看,仍認為Uber最終不會選擇收購Expedia,謹說明於下。

Uber三大事業的投入產出比仍高

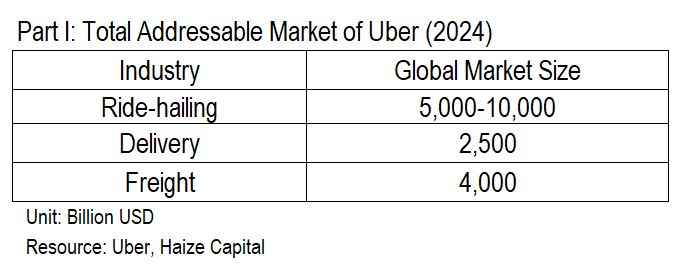

從過往歷史看,我們認為Uber不是四處尋找盈利公司併表的控股公司,而是強調優化各種轉化率的互聯網公司,這類公司一般會認真計算收購前後在潛在市場的ROI。根據Uber曾披露的投資者報告,其所著力的總潛在市場(Total Addressable Market, TAM)約為12兆至16兆美元,該產值反映了三項事業的全球市場:

1. 網約車(Ride-hailing)-全球潛在市場約5兆至10兆美元,包括使用到計程車與小客車的所有城市交通需求。

2. 配送(Delivery)-全球潛在市場約2.5兆美元,包括餐飲外賣和雜貨配送等各類配送服務。

3. 貨運(Freight)-全球潛在市場約4兆美元,包括跨國物流、公路運輸、海運、鐵路和航空運輸。

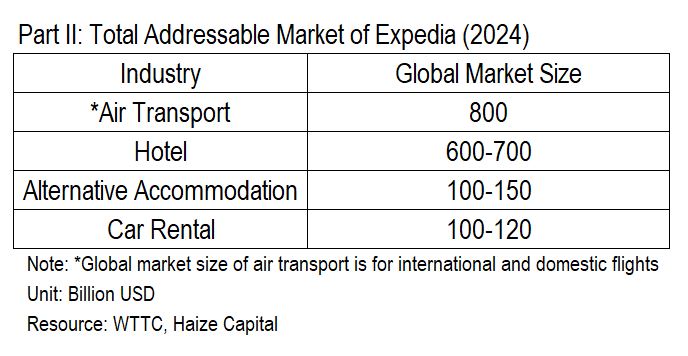

那麼,Expedia所覆蓋的潛在市場有多大?雖然廣義來看,我們會認定全球旅遊市場的總規模會相當於全球GDP的10%左右,亦即在疫情前(2019年)約達9兆美元;但除去與本地生活相關的旅遊產值後會小得多,狹義來看僅約2兆美元上下;而Expedia所覆蓋的全球潛在市場僅涵蓋航空運輸市場(約8000億美元)、住宿市場(約7000-8500億美元)與租車市場(約1000-1200億美元),總值約1.6兆美元至1.8兆美元之間,只能算狹義中的狹義,特別在Uber決意通過P2P共享模式進入(不帶駕駛的)租車市場後,Expedia的價值沒有看起來高,這裡還不談Expedia有80%的收入來自於訂房,收入極端單一。

我們認為,Uber當然可以再創設第四項事業,但從投資報酬率來說,目前Uber滲透率較高的主要市場,以區域看為北美、歐洲,在拉美的覆蓋較弱,在亞洲則只在部分城市佔優。整體來說,在新興市場的滲透率仍然較低;從ROI看,我們認為投入於現有事業的產出效益會遠超過投入於旅遊業。Uber並不需要這麼快就進入(Expedia覆蓋的)旅遊市場。

Expedia更需要Uber,而非反之

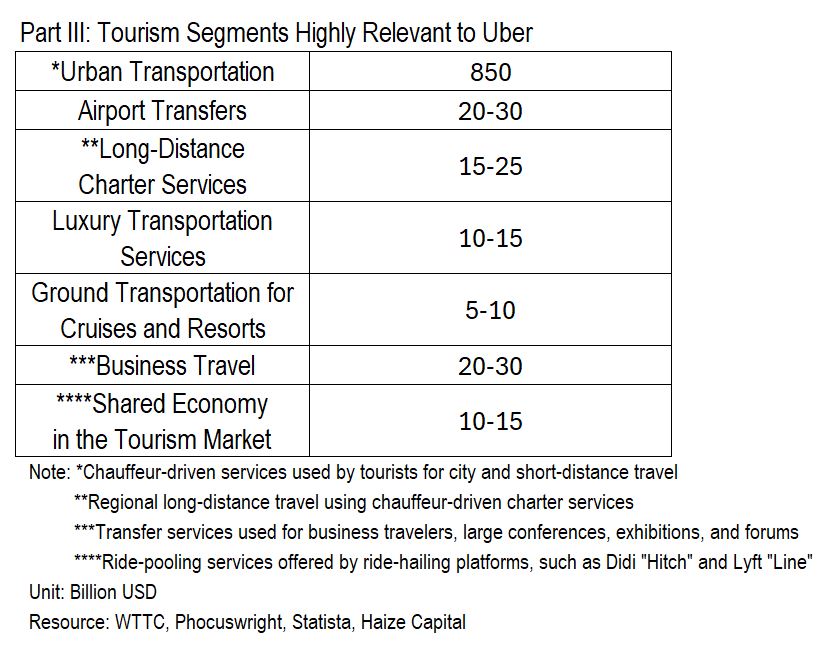

Expedia與Uber間,到底誰更需要對方?從細分領域的覆蓋來說,即便沒有Expedia的助力,Uber也正在侵蝕全球旅遊市場的版圖,如城市交通的旅遊部分(8,500億美元)、機場接送服務(約200-300億美元)、包車服務(約150-250億美元)、禮賓用車服務(約100-150億美元)、郵輪和度假村的地面交通(約50-100億美元)、商務旅遊交通服務(約200-300億美元)、網約車的順風車服務(約100-150億美元),而且Uber還覆蓋了不少Expedia目前沒觸及到的產品領域。

當然投資Expedia可以快速增加"車+X"的交易,但這通過與各OTA的分銷合作也辦得到,只差沒有將Expedia的收入併表而已。

此外,在效率上,Expedia用了一年半才整合好Hotel.com、Vrbo、Expedia的積分系統(即所謂"onekey"),這對同為集團的Booking或攜程來說,效率之低幾乎是不可想像的,很難推估Uber如果要在系統面整合Expedia必須浪擲多少成本/費用。我們認為其實還是Expedia更需要Uber,如果雙方當前的估值交換,由1,600億美元的Expedia來整合200億美元的Uber,看來反而是不錯的交易。

媒體放話無益促成收購

根據金融時報報導,其徵詢的未具名人士,說明"(Uber)尚未與Expedia進行正式接觸,目前也沒有進行任何討論(No formal approach has been made to Expedia and there are no current discussions)"。而可能知道"收購"一事的層面雖然廣,但能確認是否進行”正式”接觸者,只有雙方關鍵部門人員與受委託的投行,而投行受NDA約束,除非這也在委託範圍,不然提前公示是自毀信譽。從歷史經驗來看,會有這篇報導大概率是特定方嘗試通過股價波動提高收購籌碼的行為。不過,收購不只是Dara Khosrowshahi與Barry Diller兩人之間的事,而是雙方董事會甚至大股東之間的事,這樣操作只會讓收購更困難,早前Tripadvisor被收購破局一事就是殷鑑。

總結而言,Uber是間正在起飛的增長型公司,Expedia則是間在旅遊版圖覆蓋並不全面的價值型盈利公司,Uber現有資金有更好的投入標的,我們認為收購Expedia不算特別聰明的決策。

----

Haize Capital Insights of the Day

Three Reasons Why Uber Won’t Acquire Expedia

Recently, the Financial Times reported on Uber (NYSE: UBER) potentially considering an acquisition of Expedia (NASDAQ: EXPE). Given Uber’s involvement in some niche travel-related product lines, and the background of its current CEO, Dara Khosrowshahi—who served as Expedia’s CEO for 12 years and worked closely with Expedia’s current chairman, Barry Diller, for over 26 years—the acquisition speculation seemed credible. However, Haize Capital views Uber as unlikely to proceed with the Expedia acquisition, based on three key considerations, which are outlined below.

1. Uber’s ROI in Its Three Core Businesses Remains High

Historically, Uber is not a holding company looking to consolidate profitable companies but rather an internet company focused on optimizing conversion rates. Such companies typically carefully calculate ROI in potential markets before and after any acquisition. According to investor reports previously disclosed by Uber, its total addressable market (TAM) is estimated at around $12-16 trillion, covering the following three sectors:

a. Ride-hailing: Global TAM of about $5-10 trillion, covering all urban transportation needs involving taxis and passenger cars.

b. Delivery: Global TAM of approximately $2.5 trillion, spanning all delivery services, including food and grocery delivery.

c. Freight: Global TAM of around $4 trillion, covering international logistics, road, sea, rail, and air transportation.

So, how large is the potential market for Expedia? Broadly, the global travel market is estimated to account for roughly 10% of the world’s GDP, reaching about $9 trillion in 2019 before the pandemic. However, after excluding the segment related to local lifestyle spending, the narrow travel market comes to about $2 trillion. The TAM for Expedia’s core markets—air transport (approximately $800 billion), lodging (around $700-850 billion), and car rentals (about $1-1.2 trillion)—amounts to roughly $1.6-1.8 trillion. This is a small subset, especially since Uber has already entered the car rental market (without driver services) via a peer-to-peer model. While Uber could potentially create a fourth business line, its major markets remain concentrated in North America, Europe, and, to a lesser extent, Latin America and parts of Asia. Given these factors, investing in its current business lines is likely to yield much higher ROI than venturing into the travel market Expedia serves.

2. Expedia Needs Uber More than Uber Needs Expedia

Which company benefits more from a potential partnership? Even without Expedia’s support, Uber has been increasingly encroaching on the global travel market, especially segments like urban transportation (estimated at $850 billion), airport transfers (estimated at $20-30 billion), long-distance charter services (estimated at $15-25 billion), luxury transportation services (estimated at $10-15 billion), ground transportation for cruises and resorts (estimated at $5-10 billion), business travel (estimated at $20-30 billion) and shared economy in the tourism market (estimated at $10-15 billion).

Moreover, integrating Expedia could come with significant challenges and costs. For example, it took Expedia a year and a half to integrate loyalty programs for Hotels.com, Vrbo, and Expedia into its “OneKey” system. This would be unimaginable for competitors like Booking or Ctrip. Estimating the cost of system integration for Uber, should it pursue such a path with Expedia, could be overwhelming. In reality, Expedia arguably needs Uber more. If the roles were reversed and Expedia, valued at $160 billion, were to acquire Uber at $20 billion, it might seem a more fitting transaction.

3. Media Hype Does Not Facilitate an Acquisition

According to the Financial Times report, unnamed sources indicated that "No formal approach has been made to Expedia, and there are no current discussions." While knowledge of the “acquisition” might be widespread, only key department personnel within both companies and their appointed investment banks would have the authority to confirm any “formal” contact. These banks are bound by confidentiality agreements, and disclosing information prematurely, unless within their mandate, would harm their credibility. Historically, reports like this are often attempts by specific parties to leverage stock price fluctuations to increase acquisition bargaining power. However, an acquisition is not just between Dara Khosrowshahi and Barry Diller; it involves both boards of directors and potentially major shareholders. Such tactics would only complicate the acquisition process, as seen in the failed acquisition of Tripadvisor as a cautionary example.

In conclusion, Uber is a growth-oriented company on the rise, while Expedia is a profitable value company with incomplete coverage in the travel landscape. Uber’s current capital would be better allocated elsewhere, making an Expedia acquisition a less-than-ideal decision.

標籤 Label: EXPE Expedia UBER Uber Trip.com Booking.com Delivery Ride-hailing Freight TAM FT FinancialTimes M&A Lodging