登錄

選單

登錄

海擇短評 Haize Comment:

亞太OTA市場爭奪現況

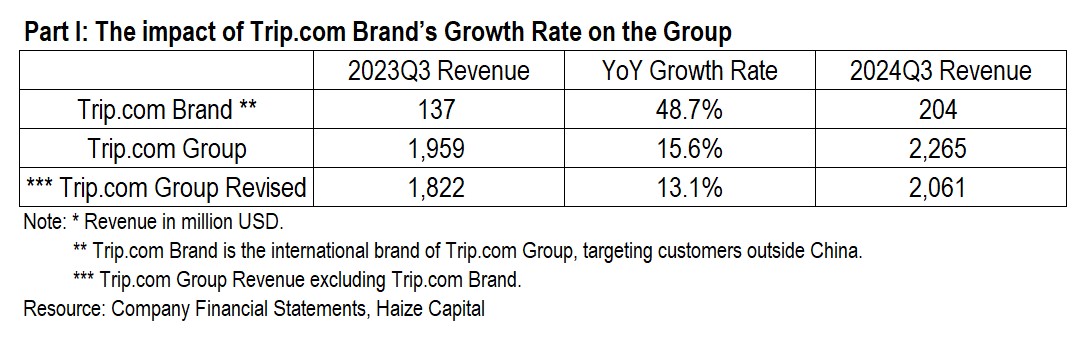

攜程集團(NASDAQ: TCOM)近期公告2024Q3財報,單季運營利潤再創歷史新高,達50億人民幣,GAAP淨利甚至超過百度(NASDAQ: BIDU),堪稱疫後的新消費主流。不過,攜程在中國境內的增速已相對飽和,如果市值要在當前的標準再增長30%以上,目前看來,必須仰賴國際平台Trip.com Brand的增長(Q3年增速達48.7%),但目前其在亞太市場的產值落後歐美玩家相距不少。從這個角度看,攜程Q3季報在境內細分領域的成績單,既可能是切入亞太市場的契機,也可能是眾OTA未來的激戰區,這些領域將衍生不少的投資機會。

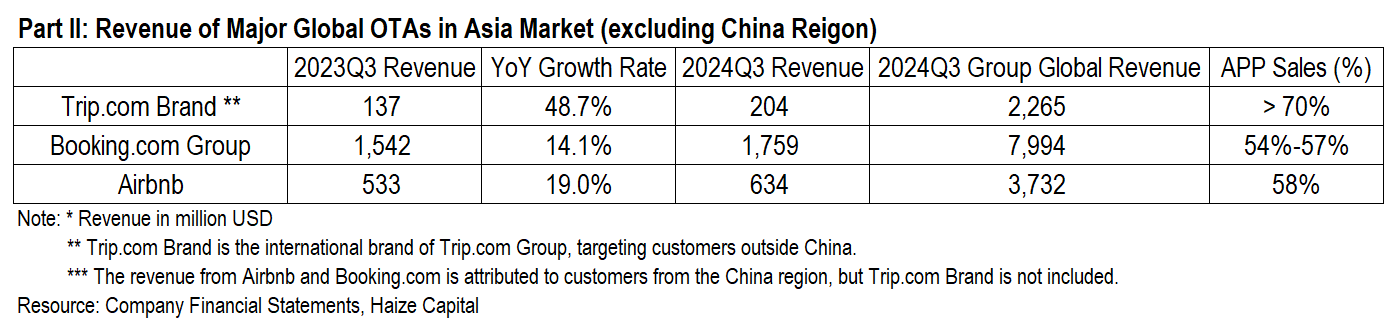

根據各OTA的財報與電話會議,我們整理出Booking(NASDAQ: BKNG)、Airbnb(NASDAQ: ABNB)與攜程國際平台Trip.com Brand在亞太市場的收入與APP消費占比,如下:

1. Trip.com Brand間夜量通過APP銷售的占比最高,推定超過70%;但歐美主流OTA也能接近60%,其中Booking公告值為54%-57%,Airbnb為58%。

2. 從各OTA的Q3亞太市場收入來看,Trip.com Brand的Q3收入約占集團總收入的9%,亦即2.0億美金。Airbnb有75%的收入來自美加澳法英5大核心市場,9個次要擴張市場合占收入的15%,其中的韓日印(度)中位於亞太,我們推估亞太市場不超過整體的17%,即約6.3億美金。Booking有24%的間夜由亞太客源預訂,由於亞太ADR會低些,我們推估22%的收入來自亞太市場,即約17.6億美元。

3. 就產品組合看,Trip.com Brand住宿相關收入占總收入的40%以上,而Booking的住宿占比約90%,Airbnb的住宿占比更在95%以上。

從上述資料我們可以做出幾個判斷:設若不看攜程式控有的中國客源市場,僅關注攜程的Trip.com Brand與歐美同業在亞太地區的競技,在APP直銷占比所代表的產品閉環與用戶獲取/留存上,攜程占優但沒有絕對優勢;從收入的絕對值看,攜程弱于歐美同業,有大幅甚至接近量級式的差距。而攜程的收入增速雖然超過競品很多,但競品近年也著力於一站式服務,用Booking的說法是”互聯旅遊(Connected Trip)”,Airbnb則在Q3官宣要從體驗產品的“本地化”開始做起,每年推出產值達10億美元的新產品線(we will launch one to two new businesses that will generate $1 billion or more of revenue incrementally a year)。

-----

The Current State of the Battle for the Asian OTA Market

Ctrip Group (NASDAQ: TCOM) recently announced its Q3 2024 financial report, achieving a record-breaking quarterly operating profit of 5 billion RMB. Its GAAP net profit even surpassed that of Baidu (NASDAQ: BIDU), establishing itself as a post-pandemic leader in new consumer trends. However, Ctrip's growth within the domestic Chinese market has become relatively saturated. For its market value to increase by more than 30% from the current level, the growth of its international platform, Trip.com Brand (Q3 YoY growth of 48.7%), appears essential. That said, its output in the Asia-Pacific market lags significantly behind Western competitors. From this perspective, while Ctrip's Q3 performance in domestic segments may represent an entry point into the Asia-Pacific market, these segments could also become key battlegrounds for OTAs, generating numerous investment opportunities.

Based on financial reports and earnings calls from various OTAs, we have summarized the revenue and app-based consumer proportions of Booking (NASDAQ: BKNG), Airbnb (NASDAQ: ABNB), and Ctrip’s international platform, Trip.com Brand, in the Asia-Pacific market as follows:

1. App-based sales: Trip.com Brand has the highest proportion of room-night sales via its app, estimated at over 70%. Western OTAs are close, with Booking reporting 54%-57% and Airbnb at 58%.

2. Revenue in the Asia-Pacific market: In Q3, Trip.com Brand's revenue from the Asia-Pacific region accounted for 9% of its total revenue, or approximately $200 million. For Airbnb, 75% of its revenue comes from its five core markets (US, Canada, Australia, France, and the UK), while nine secondary markets collectively account for 15%. Among these, South Korea, Japan, India, and China are in Asia-Pacific, which we estimate contributes no more than 17% of Airbnb’s total revenue, or around $630 million. Booking derives 24% of its room-nights from Asia-Pacific customers. Given the slightly lower ADR in the region, we estimate 22% of Booking’s revenue comes from Asia-Pacific, totaling approximately $1.76 billion.

3. Product mix: Trip.com Brand derives over 40% of its revenue from accommodation-related services, whereas Booking derives about 90%, and Airbnb exceeds 95%.

From these observations, we can draw several conclusions:

• Excluding the Chinese domestic market dominated by Ctrip, and focusing solely on Trip.com Brand’s performance against Western peers in the Asia-Pacific region, Trip.com Brand holds an advantage in app-based direct sales (representing a closed product loop and customer acquisition/retention) but lacks an absolute edge.

• In terms of absolute revenue, Trip.com Brand significantly underperforms its Western peers, with a substantial gap in scale.

• While Trip.com Brand's revenue growth outpaces its competitors, Western players have also been strengthening their offerings in recent years. For instance, Booking emphasizes the "Connected Trip," and Airbnb announced during its Q3 earnings call plans to launch one to two new localized product lines annually, each generating $1 billion or more in incremental revenue.

標籤 Label: TCOM BKNG ABNB Booking.com Trip.com Airbnb Japan ThingsToDo PackageTour ESG Invest Accommodation