登錄

選單

登錄

海擇短評 Haize Comment:

國際化是同程市值突破80億美元的唯一機遇

今年Q3對全球旅遊業都是豐碩的季度,同程旅行(HK: 0780)也創下收入與淨利歷史新高,收入YoY增長51.3%,達人民幣49.9億元,經營溢利YoY增長63.1%,達人民幣9.8億元。財務指標乍看無可挑剔,然而,若從運營指標的角度看,或與同業攜程相比,不足之處就很明顯。不過,即便同程的出境產值落後攜程甚多,但國際化仍是唯一能讓市值從峰值再突破30%的機遇與冒險。

增長瓶頸從用戶活躍開始

從運營指標看,同程的增長瓶頸就趨於明顯。首先,用戶活躍的增速不高,Q3平均月付費用戶僅年增5%,Q2甚至出現季減,雖然以4,640萬人次的龐大基數看,個位數增長並不算不好。但若同時考慮同程旅行自2024年初,已將”度假” 事業併表,理論上從季報公告的用戶活躍、交易額、購買頻次、交叉銷售率到平均用戶收入(ARPU),都應該要有戲劇化的提升。

從”度假”併表的角度來理解下列數據,就能清楚為什麼海擇資本認為這些不錯的增速會是瓶頸:交易額年增速2.4%、用戶購買頻率從2019年的每年5.5次,到2024年的每年8次;交叉銷售率從2023Q3的10%,到2024Q3的12%;ARPU較2023年9月底增長54%。看起來盈利增長更多來自降本增效。

國際化是攜程的內卷底氣

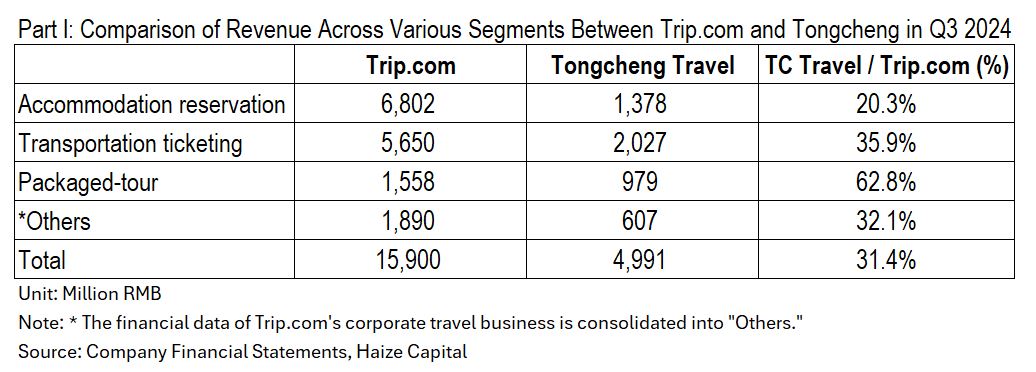

如果與攜程相比,不足之處就更為明顯。攜程集團Q3收入159.0億人民幣,運營利潤50.1億人民幣;同程旅行同期收入49.9億元,已達攜程的1/3,但經營溢利為9.8億元,僅為攜程的1/10。分項來看,Q3同程的住宿服務收入13.8億人民幣,為攜程的20%;交通票務收入20.3億人民幣,達攜程的36%;度假收入9.8億人民幣,甚至是攜程同事業部的63%,表現並不差。

為什麼同程的盈利能力與攜程的差距,遠高於交易規模間的差距?中間的因素很多,但我們認為,最核心的要素,就是攜程的國際化盈利能力夠強,無論基於中國客源的各同業在中國目的地怎麼卷,攜程都能靠中國人出境盈利(但不是靠外國人使用Trip.com Brand盈利)。

因此,同程的挑戰就很明確,提升每用戶平均收入(ARPU)的目的,必須依賴國際化達成。同程的國際化做得好,攜程在境外如果不卷,同程跟著印鈔票;攜程如果選擇在境外一起卷,自傷利潤率,那攜程就必須降低境內卷的程度,那同程一樣可以印鈔票,可能還更多。

當前同程國際化對攜程尚無威脅

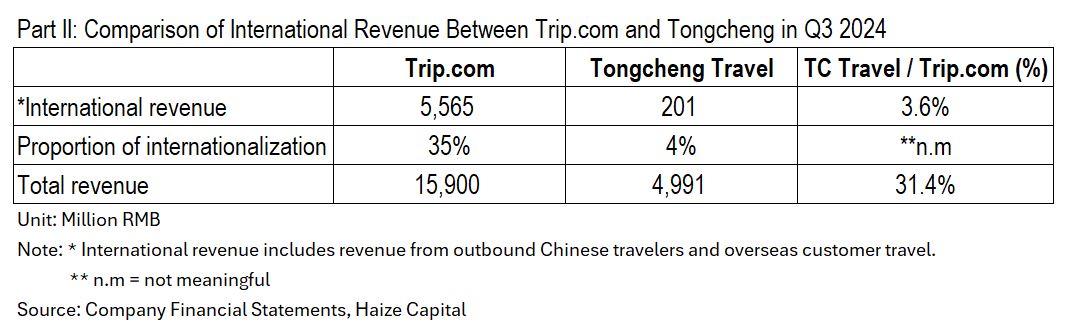

想像是美好的。那麼,現在同程的國際化對攜程是威脅嗎?遠遠不是。從中國客源出境的層面看,雖然攜程未公告Q3中國客源出境的國際收入,若依2019年季報公告看,一樣推估國際收入佔總收入的35%,產值約55.7億人民幣。相比之下,同程Q3的國際收入約佔其核心在線旅遊平台的5%,即總收入的4%,約2.0億人民幣,僅占攜程同口徑的3.6%,意外得小,對中國客源出境的掌握仍相對初級。

如果僅看境外客源,Q3攜程的國際客源(非中國市場客源)收入中,Trip.com Brand約貢獻集團總收入的9%,即約14.3億人民幣;同程的國際客源收入我們則認為可以忽略不計。這所反映的現況是,”同程旅行”品牌對境外客源意義不大;看來管理層也尚未比照攜程,從內部事業體建立單獨的財務中心(如Trip.com Brand),吸引境外客源。不過,即便不使用”同程”品牌,同程確實也有直接取得境外客源的能力與投入,如下述。

地緣政治是攜程毒藥,但卻是同程妙藥

從對初創公司的股權投資看,就會比較有意思。攜程堪稱中國旅遊業在全球化佈局的王者,這點殆無疑義。其所收購的Skyscanner(2016年11月)、Travelfusion(2015年1月)、MakeMyTrip(2016年1月),甚至控股俄羅斯的機票平台,無一不具有重大影響力。但也因其400億美金的市值地位,能與Booking及Airbnb共論劍,投資收購備受各國監管機構用放大鏡檢視。或者我們用另一個角度說,攜程過往收購的平台,若處於當前的地緣政治現況發起收購,極有可能沒有任何一家能通過審核。事實上,自中美貿易戰後,攜程也沒有過大規模的項目收購。

相對來說,雖然同程背後的騰訊不小,但同程市值僅60億美元,只約攜程的1/8,就不會像攜程動見觀瞻,處處觸發各國監管對中國企業莫名的反壟斷神經。這樣的競爭力,雖不是同程主動取得的優勢,但卻是意外之喜。在此背景下,同程投資在地域上單壓日本,產品上側重酒店管理品牌,期望在最鄰近中國、客單價最高、目的地產品最多元的地域取得一席之地,梭哈有限資源單點突破,似乎是唯一也是最好的方法,很類似台灣玩樂業者KKday面對Klook所選擇的策略。日本以外,我們認為同程最重要的海外小老虎,是在新加坡推出的返利平台Azgo與香港的HopeGoo,特色同是側重效果行銷而非品牌行銷。

同程的奇妙機遇與冒險

同程有一定程度的路徑依賴,這導致它同時有著在中國境內極強,但在國際化又極弱的超級奇妙地位。從市盈率的角度看,它與攜程相仿,這讓二級市場投資人不得不想像,這家在(中國)國慶前能創造300多萬日活躍用戶的旅行公司,一旦能從日本目的地開始吸納中國出境客源,或是藉由小到不被地緣政治壓迫的靈活地位,用股權投資直接在境外發起挑戰,它本身的投資價值,似乎還有很大的潛力。同樣是從峰值增長30%市值,是攜程靠Trip.com Brand容易,還是同程靠國際化容易,將會是2025的有趣議題。

----

Haize Capital Insights of the Day

Internationalization: The Only Opportunity for Tongcheng to Surpass an $8 Billion Market Cap

Q3 2024 has been a prosperous quarter for the global travel industry, with Tongcheng Travel (HK: 0780) achieving record highs in both revenue and net profit. Revenue grew by 51.3% year-over-year to RMB 4.99 billion, while operating profit increased by 63.1% year-over-year to RMB 980 million. At first glance, the financial metrics appear flawless. However, from the perspective of operational indicators or in comparison to its competitor Trip.com (NASDAQ: TCOM), shortcomings become evident. Even though Tongcheng’s outbound travel segment lags far behind Trip.com, internationalization remains the only opportunity for Tongcheng to break past its peak value and achieve a 30% increase in market cap—a journey filled with challenges and potential.

Growth Bottleneck Starts with User Engagement

Analyzing Tongcheng’s operational indicators, its growth bottleneck is increasingly apparent. First, user engagement growth is modest. In Q3, the average monthly paying users (MPUs) increased by only 5% year-over-year, while Q2 even saw a quarter-on-quarter decline. Although its massive base of 46.4 million MPUs makes single-digit growth reasonable, considering that Tongcheng integrated its "Vacation" business into its financials at the start of 2024, dramatic improvements in user engagement, transaction volume, purchase frequency, cross-selling rates, and average revenue per user (ARPU) were theoretically expected.

Understanding the following data from the perspective of "Vacation" consolidation explains why Haize Capital views these growth rates as a bottleneck:

˙Transaction volume grew by 2.4% year-over-year.

˙User purchase frequency increased from 5.5 times annually in 2019 to 8 times in 2024.

˙Cross-selling rates rose from 10% in Q3 2023 to 12% in Q3 2024.

˙ARPU grew by 54% compared to the end of September 2023.

It appears that profit growth has relied more on cost reduction and efficiency improvements.

Internationalization: The Driving Force Behind Trip.com’s Success

In comparison to Trip.com, Tongcheng’s weaknesses are even more evident. In Q3, Trip.com reported revenue of RMB 15.9 billion and an operating profit of RMB 5.01 billion, while Tongcheng’s revenue of RMB 4.99 billion is roughly one-third of Trip.com’s, yet its operating profit of RMB 980 million is only one-tenth.

Breaking it down by segments:

˙Tongcheng’s accommodation services revenue was RMB 1.38 billion, 20% of Trip.com’s.

˙Transportation ticketing revenue reached RMB 2.03 billion, 36% of Trip.com’s.

˙Vacation revenue was RMB 980 million, even 63% of Trip.com’s corresponding segment.

Why does the profitability gap between Tongcheng and Trip.com far exceed their transaction volume gap? The key factor is Trip.com’s robust international profitability. Regardless of the intense domestic competition among Chinese travel platforms, Trip.com secures steady income from Chinese outbound travelers (not primarily from foreign users on the Trip.com brand).

Thus, Tongcheng’s challenge is clear: to enhance ARPU, it must rely on internationalization. If Tongcheng’s international expansion succeeds, it could share the profitability of Trip.com’s outbound market or force Trip.com to reduce its focus on domestic competition, thereby allowing Tongcheng to improve its domestic margins.

Tongcheng’s Current Internationalization Poses No Threat to Trip.com

The potential for internationalization is enticing. However, does Tongcheng’s current international strategy pose a threat to Trip.com? Not yet.

From the perspective of Chinese outbound travelers, while Trip.com hasn’t disclosed its Q3 outbound travel revenue, past reports, such as its 2019 earnings, suggest international revenue comprises about 35% of total revenue, amounting to RMB 5.57 billion. In comparison, Tongcheng’s Q3 international revenue is about 5% of its core online travel platform revenue, or 4% of total revenue, approximately RMB 200 million—only 3.6% of Trip.com’s estimated figure. Tongcheng remains at an early stage in capturing the Chinese outbound travel market.

As for overseas customer revenue, Trip.com’s international customers (non-Chinese market) contributed 9% of total revenue, approximately RMB 1.43 billion in Q3. Tongcheng’s contribution in this area is negligible, reflecting that the "Tongcheng Travel" brand holds little value for overseas customers. Management has not established a dedicated financial center, like Trip.com’s internal brand strategy, to attract international users. Nonetheless, Tongcheng has made investments to acquire overseas customers indirectly, as discussed below.

Geopolitics: A Poison for Trip.com, Yet a Boon for Tongcheng

The differences in equity investments offer intriguing insights. Trip.com is undoubtedly the leader in global expansion within China’s travel industry, with acquisitions of Skyscanner (November 2016), Travelfusion (January 2015), and MakeMyTrip (January 2016), as well as control over a Russian ticketing platform. However, its $40 billion market cap subjects it to intense scrutiny by global regulators, akin to Booking.com and Airbnb.

From another angle, if Trip.com were to pursue these acquisitions in today’s geopolitical climate, none would likely pass regulatory approval. Indeed, since the U.S.-China trade war began, Trip.com has made no significant acquisitions.

In contrast, while Tongcheng benefits from Tencent’s backing, its $6 billion market cap—only one-eighth of Trip.com’s—allows it to avoid triggering geopolitical concerns over Chinese corporate monopolies. This "small and agile" position may not be an intentional advantage, but it is certainly a welcome one.

Tongcheng’s international investment strategy focuses on Japan, particularly in hotel management brands, targeting the region with the highest per-customer spending and the most diverse product offerings. Tongcheng’s strategy of concentrating resources for single-point breakthroughs mirrors KKday’s approach to competing with Klook. Beyond Japan, Tongcheng’s key overseas initiative lies in Singapore, where it launched the cashback platform Azgo, which emphasizes performance marketing over brand marketing.

Tongcheng’s Unique Position and Potential

Tongcheng’s unique path dependency positions it as exceptionally strong domestically yet notably weak internationally. Valuation-wise, it is comparable to Trip.com, compelling investors to imagine the potential of a travel company that, during China’s National Day holiday, attracted over 3 million daily active users.

If Tongcheng can begin leveraging outbound travel from Japanese destinations or capitalize on its agility to execute overseas equity investments, it could challenge international markets without the geopolitical pressures faced by Trip.com. The investment potential of Tongcheng’s internationalization strategy remains significant.

Whether a 30% market cap growth is easier for Trip.com via its Trip.com brand or for Tongcheng via internationalization will undoubtedly be one of the most intriguing topics for 2025.