登錄

選單

登錄

海擇短評 Haize Comment:

1億美元比400億美元便宜…嗎?解讀途牛的天花板

各國(存活的)主要旅遊公司,在疫情後大體都活得很好,途牛(NASDAQ: TOUR)也不例外,歸屬於途牛股東的淨利,在2024Q3創下4,445萬人民幣的歷史新高。然而,途牛依靠抖音等直播帶貨通路,推動團隊遊事業增長,頗有天花板的現象。途牛沒有同業可以借鑑,投資價值能否再突破,將與抖音如何定位旅遊版塊有更大的關聯。

途牛增速弱於同業

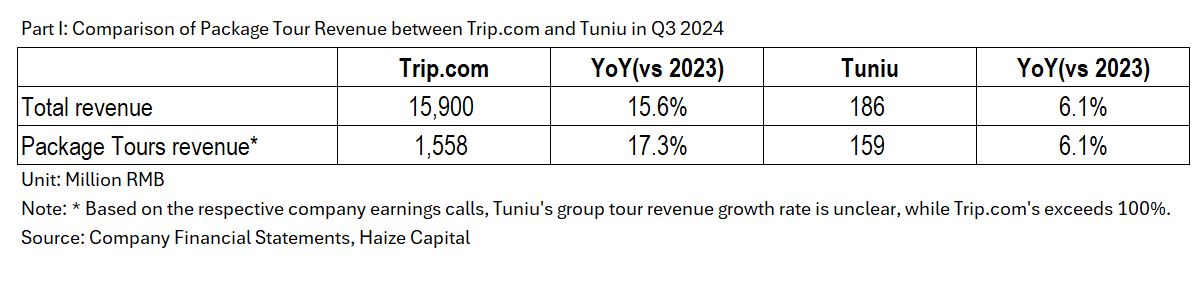

途牛的2024Q3財報顯示,占比總收入86%的度假事業(Packaged tours),收入YoY增速為6%,與攜程同事業部相比,略低但沒有重大差距。不過,值得注意的是,途牛的度假事業以跟團遊為核心,而攜程度假事業若單獨拉跟團遊出來看,依季報Q3的同比增速超過100%。攜程與途牛規模有差距,對比不盡然有意義,我們提出這點是想說明,途牛團隊遊在Q3的收入增速,很可能低於行業與同業。

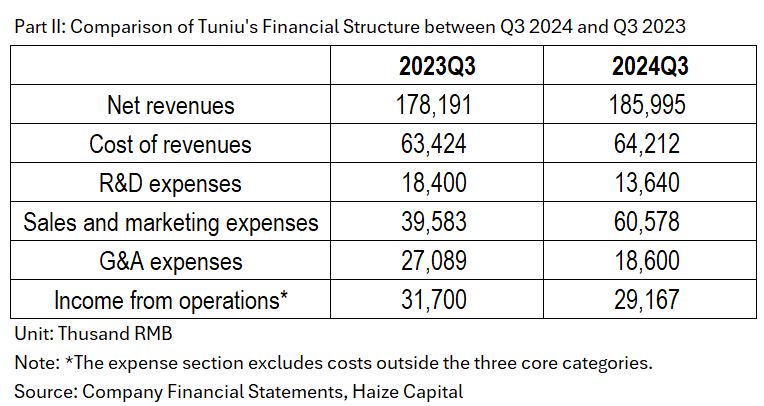

若將途牛Q3季報與去年同期季報比對,可以發現,兩季度假事業收入、毛利與運營利潤基本相仿,而研發和管理費用YoY各壓縮26%與31%;兩大費用壓縮,但運營利潤卻沒有上升,原因在於行銷費用大幅增加53%。季報顯示途牛在行銷投放的ROI大幅下降;我們的另一層理解是,途牛或許出現行銷投放在超過某個平衡點後,ROI就快速下降的結構性問題。

直播帶貨的難題在於履約

途牛的行銷模式高度依賴直播帶貨,特別是抖音短視頻平台。途牛在2023年年報記載了直播的重要性(live streaming shows to promote our own products… is popular for both product sales and content offering);而根據Q1季報,今年1月-5月,途牛直播交易額年增超過200%,核銷量增加400%(即核銷率提高)。除了擁有超過60個內部直播帳號,還與MCN機構及1,000名網紅合作。

抖音作為帶貨渠道,一直以來的特色,就是銷量大但核銷率低,從履約的角度看,客戶不約而退款的概率遠高於OTA銷售日曆房的退改率。而抖音本身對標準品與非標品的核銷率,也有高低之別,如住宿這類的標品較好,但核銷率一般也只有5%-10%,頂峰估計也只在20%-30%之間;標品如此,充滿複雜性的度假類甚至團隊遊產品,核銷率可想而知。

國際市場誰能借鏡誰?

投資市場中,跨境借鑑、異地複製並不丟臉,靠這個模型IPO的公司可多了。途牛的尷尬之處,也是很多中國互聯網公司的宿命,就是在境外沒有借鑑典範,從旅遊直播帶貨的角度看,境外比中國更早期。目前境外旅遊直播大多只是各國旅遊局用來推廣目的地的方式,東南亞帶貨形式比較完整,Shopee Live與Lazada Live會與旅行社合作銷售套裝旅行、景點活動、美食體驗…,但KPI在基因上就不是以盈利為主,更像是協助政府當局做旅遊推廣,以換取不被既得利益者抵制,有興趣可以參考TikTok在印尼與政府的交手,這不是個案。

韓國的直播帶貨又比東南亞更具深度,旅行社與電商平台(如Coupang、11번가)和社交媒體平台(如Naver、Kakao、YouTube)結合得很頻繁。組團社對直播帶貨也很積極,Hana Tour (KRX: 039130)推出"Hana LIVE"、ModeTour (KOSDAQ: 080160)推出"Live M"、Very Good Travel推出"Very Good LIVE",共有的特色是主動披露交易額、訂單數,且提高直播頻率,但不公告核銷率或核銷量。最合理的解釋是,直播確實有流量,也確實能成交,但從履約的角度看,ROI仍屬堪憂,但可以替代逐漸失效的渠道,比如電視購物。因此最後的選擇是,核心資源投入官網/自有APP直播,而非平台通路,至少用品牌行銷的指標檢核,不會像效果行銷那麼尷尬。

從這個角度看,途牛與借鑑境外,倒不如說被境外當成教科書(不論成敗)的可能性比較大。途牛針對不同目的地設立矩陣式直播帳號,以細分客群。然而,Q3財報也能理解為矩陣策略的成績單。如果進一步的矩陣(比如以用戶年齡或使用場景再細分),還無法帶來可觀的ROI提升,那麼就看不出收入大幅向上的空間--無論是否依賴抖音。

抖音平台能用什麼視角看途牛?

更值得重視的是抖音與途牛的關係,3,000億美金市值的公司需要跟1億美金市值的公司維持什麼關係?不就是割韭菜嗎?這樣說也對、也不對。作為平台,當然可以通過流量傾斜創造賣貨以外的商業模式,哪怕平台上商戶的盈利能力受損,方法太多了,這是商業原則,無涉道德。更容易理解的是,把攜程在住宿市場的地位視為典範來看,只要酒店物業供過於求,就可以通過商戶之間的內卷獲得更多收益,抖音當然也可以這麼做,為了盈利與IPO,不但要做,還要做到精細。

對於途牛而言,教科書的解決方案當然是行銷渠道多樣化,降低對抖音的依賴,但是談何容易?如果精算各渠道的行銷ROI曲線變化,就知道難題並不總是有解。途牛在年報也披露了客戶獲取難度與品牌認知的關聯(If we fail to enhance our brand recognition, we may face difficulty in retaining existing customers and attracting new customers…)。

不過,站在抖音的角度,需要考慮的是,途牛的公司規模,至少也是千人量級的員工與億人民幣量級的收入,中國超過途牛規模的商戶能有多少?如果連途牛在抖音平台上都難以增長,抖音其實很難說服其他商戶,在平台賣度假產品是個好賽道,更別說TikTok所覆蓋的境外市場。即便抖音認為是途牛運盈面的問題,那也要打造其他的典範。

攜程相對沒有這個問題,攜程的核心供應商華住,就是個很好的典範,過往10年,多數時候市盈率甚至比攜程高。先不談”攜程四君子”的關係,與華住APP能輾壓同業的有機流量佔比,至少華住的存在,證明了平台與商戶能共生的事實。抖音需要一個類似華住之於攜程的範例,只是,這個範例可以是、也可以不是途牛。

途牛的投資價值再思考

途牛目前的市值約為1億美元,與攜程和同程相比固然絕對值低很多,股東權益甚至低於淨值,從投資的角度看似很可口。然而,若加諸考慮收入與淨利增長的能見度,看起來又沒有那麼可口了。對於投資者而言,不能說途牛再增長的契機,但是從優先級看,與渠道的合作深度,將重於運營上的產品力與價格力。

----

Haize Capital Insights of the Day

$0.1 Billion Cheaper Than $40 Billion... Really? Interpreting Tuniu's Ceiling

In the post-pandemic era, major surviving travel companies worldwide are thriving, and Tuniu (NASDAQ: TOUR) is no exception. In Q3 2024, Tuniu achieved a record-high net profit attributable to shareholders of RMB 44.45 million. However, Tuniu's reliance on livestream sales channels like Douyin to drive growth in its group tour segment has seemingly hit a ceiling. Without clear industry benchmarks to follow, Tuniu’s investment potential hinges heavily on how Douyin positions its travel segment.

Tuniu’s Growth Trails Its Peers

According to Tuniu’s Q3 2024 financial report, its packaged tour segment, which accounts for 86% of total revenue, saw a YoY growth rate of 6%. While slightly lower than Ctrip’s comparable segment, the gap isn’t significant. However, Tuniu’s packaged tours are centered around group tours, whereas Ctrip’s group tours alone achieved over 100% YoY growth in Q3.

Although comparing Ctrip and Tuniu directly might not seem entirely fair due to their differing scales, this highlights a key point: Tuniu’s group tour revenue growth in Q3 likely lags behind industry and peer averages.

A closer comparison of Tuniu’s Q3 2024 and Q3 2023 financials shows that its packaged tour revenue, gross profit, and operating profit remain largely flat, despite R&D and administrative expenses declining by 26% and 31% YoY, respectively. The stagnation in operating profit is attributed to a 53% surge in marketing expenses. This suggests a significant decline in the ROI of Tuniu’s marketing investments, possibly reflecting a structural issue where marketing ROI drops sharply after surpassing a certain threshold.

Livestream Sales: The Fulfillment Challenge

Tuniu’s marketing strategy heavily relies on livestream sales, particularly through Douyin. Its 2023 annual report highlighted livestreaming’s importance (“live streaming shows to promote our own products…is popular for both product sales and content offering”). According to Tuniu’s Q1 2024 report, its livestream GMV from January to May grew over 200% YoY, with redemption volume surging 400%, indicating an improvement in redemption rates. Tuniu boasts over 60 internal livestream accounts and collaborations with MCN agencies and 1,000 influencers.

However, Douyin’s hallmark as a sales channel is its high volume but low redemption rate. From a fulfillment perspective, customer cancellations and refunds are far higher compared to OTA hotel bookings. Douyin’s redemption rates also vary between standard and non-standard products. For standard items like accommodations, rates generally range from 5%-10%, peaking at 20%-30%. For complex vacation or group tour products, redemption rates are likely even lower.

Who Learns From Whom in the Global Market?

Cross-regional learning and replication are common in the investment world, and many companies have IPOed based on this model. Tuniu’s awkward position, which mirrors the fate of many Chinese internet companies, is that there are no overseas benchmarks to follow. From the perspective of travel livestreaming, international markets are still in their infancy.

Currently, travel livestreaming overseas is mostly used by tourism boards to promote destinations. In Southeast Asia, platforms like Shopee Live and Lazada Live collaborate with travel agencies to sell packaged tours, activities, and food experiences. However, their KPIs are more aligned with tourism promotion rather than profitability, aiming to avoid resistance from vested interests. Examples like TikTok’s negotiations with the Indonesian government illustrate this approach.

South Korea’s livestreaming ecosystem is more mature. Travel agencies actively collaborate with e-commerce platforms (e.g., Coupang, 11st) and social media (e.g., Naver, Kakao, YouTube). Major agencies like Hana Tour (KRX: 039130) and ModeTour (KOSDAQ: 080160) have launched their own livestream platforms such as “Hana LIVE” and “Live M.” However, these platforms tend to disclose transaction volumes and order counts while withholding redemption data, likely indicating that while livestreaming drives traffic and transactions, ROI from fulfillment remains questionable.

From this perspective, Tuniu might serve more as a case study for overseas markets—successful or not—rather than finding inspiration abroad. Tuniu’s destination-specific livestream matrix strategy has segmented its customer base further, but Q3 results suggest that even this approach may have reached its limits. If further segmentation (e.g., by user age or usage scenario) fails to deliver meaningful ROI, significant revenue growth appears unlikely—whether reliant on Douyin or not.

Douyin’s View of Tuniu: Symbiosis or Exploitation?

The relationship between Douyin and Tuniu is worth examining. What kind of relationship does a $300 billion company need with a $100 million company? A parasitic one? Perhaps, but not entirely. As a platform, Douyin can tilt its algorithms to drive revenue beyond product sales, even at the expense of merchants’ profitability—this is business, not morality.

Drawing parallels with Ctrip’s dominance in accommodation, Douyin could exploit merchant competition to maximize its own earnings. For Tuniu, diversifying its marketing channels to reduce reliance on Douyin is the textbook solution, but easier said than done. Tuniu’s annual report acknowledges the challenge of customer acquisition and brand recognition (“If we fail to enhance our brand recognition, we may face difficulty in retaining existing customers and attracting new customers…”).

From Douyin’s perspective, Tuniu’s scale is significant, with a workforce in the thousands and revenues in the billions of RMB. If even Tuniu struggles to grow on the platform, Douyin may find it hard to convince other merchants that selling vacation products is a viable path, especially in overseas markets covered by TikTok. Even if Douyin views Tuniu’s challenges as operational, it must establish alternative success stories.

Ctrip doesn’t face this issue. Its core supplier, Huazhu, is a proven example of platform-merchant symbiosis. For over a decade, Huazhu’s market cap often rivaled Ctrip’s, driven by its superior organic traffic on its app. Douyin needs a similar flagship example for its platform—whether or not that example is Tuniu.

Rethinking Tuniu’s Investment Potential

With a market cap of $1 billion, Tuniu seems undervalued compared to Ctrip or Tongcheng. However, when factoring in its visibility for revenue and net profit growth, it appears less attractive. For investors, Tuniu’s path to further growth lies more in its depth of collaboration with channels than in operational product or pricing advantages.

標籤 Label: TOUR TCOM Tuniu DouYin TikTok PackagedTours HanaTour ModeTour ShopeeLive LazadaLive

#TOUR #Tuniu #DouYin #TCOM #TikTok #PackagedTours #HanaTour #ModeTour #ShopeeLive #LazadaLive