登錄

選單

登錄

海擇短評 Haize Comment:

Uber與美團會在何處夢幻對決?

美團(HK: 3690)與Uber(NYSE: UBER)與是當今全球科技與服務領域中規模相當、影響深遠的兩家互聯網公司。雖然它們分別來自美國和中國,但其產品型態、收入規模到市值量級,都足以媲美彼此。如果兩者產生市場競爭,從商戰角度,將其視為中美新型代理人戰爭的一部分,或許也不算誇張。這場夢幻對決會出現嗎?如果出現,又將以什麼型態,在哪個地域出現?

業務對撞最可能發生在本地生活服務

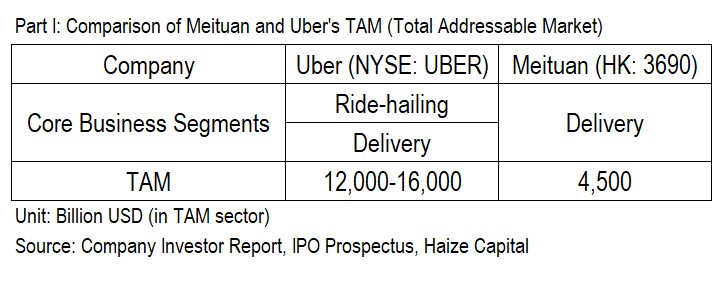

根據Uber的投資者報告,其潛在市場產值(Total Addressable Market, TAM)約為12兆至16兆美元,該產值反映了以網約車(Ride-hailing)為主(全球潛在市場約5兆至10兆美元)三項事業(另有配送與貨運)的全球市場。而根據美團在IPO時所估算,中國生活服務行業在2023年的潛在市場產值超過4.5兆美元(33兆人民幣),其中線上產值超過1.1兆美金(8兆人民幣);當時預估線上總產值50%來自於食品消費,30%來自酒旅服務。

Uber與美團都構築了超級APP生態系統。雙方的核心差異是,Uber雖擁有網約車與外賣雙主線事業,但網約車事業更為核心,將基於演算法的共用用車模型,按照使用的頻次、價格、場景三條線延伸成生態系統;至於外賣服務,在將配送延伸到生活雜貨後,近期才開始初步嘗試與到店服務結合。

美團自”千團大戰”崛起,但成為千億美金量級公司,主要還是從外賣主線事業延伸到”核心本地商業”,涵蓋從餐飲外賣、到店餐飲、食品零售、酒旅預訂等數十種從高頻到長尾的產品/服務。特別餐飲的部分,既往供應鏈上游延伸,也不斷裂變出對外賣和到店服務的補充(比如”秒提”),並以小象超市與美團優選增加品類廣度。不過,美團在網約車領域不如Uber成功,網約車的自營品牌”滴滴出行”,與用車整合平台”高德”,在中國市場影響力都高於美團。

因此,如果雙方發生激烈業務對撞,不會在出行領域,最可能在以外賣為主線的本地生活服務,特別是在國際市場。

頂流按需服務公司的規模

那麼,做為當前全球頂流的按需服務(on-demand)類公司,核心運營指標能到達什麼量級?比較2024Q3季報可以發現,雙方都已證明所涉入的商業需求足夠高頻、盈利空間足夠大,在境外也仍有足夠的複製圈地機會。

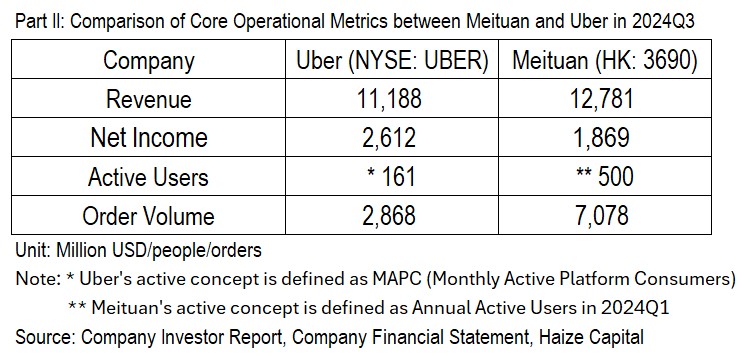

Uber在Q3的收入達112億美元,增速仍有20%,單季淨利超過26億美元;美團同期收入約128億美元(936億人民幣),增速仍有22%,單季期內溢利超18億美元(129億人民幣)。

從使用頻次更能證明其影響力。Uber在Q3的訂單數為28.7億單,除以月支付活躍用戶數1.6億,每活躍用戶單月約使用5.9次;美團同期訂單數70.8億單,雖然未公告月支付活躍資料,但依Q1公告年活躍用戶5億推斷,同口徑資料應優於Uber。

先國際化還是先城市下沉?

擁有如此高的消費頻次與收入增速,投資人求著它們國際化也不意外,畢竟時間就是金錢,各國得到資本挹注的copycat所在多有。不過,雙方不同的策略引導出迥異的國際化時程:美團選擇先深化中國的城市下沉市場,因此國際化佈局更晚;Uber則選擇先行國際化,在2024Q3才開始關注城市行政核心區以外的郊區與二、三線城市,認為在飽和前還能額外再增長150%-240%的產值。

具體來說,Uber在2009年由Travis Kalanick和Garrett Camp在美國加州三藩市創立後,於2011年首次進行國際化,進入美國以外的市場,第一個國際市場選擇巴黎(法國),迄今美國以外收入約占總收入的60%。與美國旅遊公司的國際化相比,Uber的國際化步伐更快,比如與Airbnb相比,Airbnb有75%的收入來自美加澳法英5大核心客源市場,說來有趣,除法國外,恰恰是地緣政治上的五眼聯盟地域;而Uber除了這五大市場,在拉美也很有影響力,在巴西的人口滲透率接近20%,在墨西哥則超過10%。

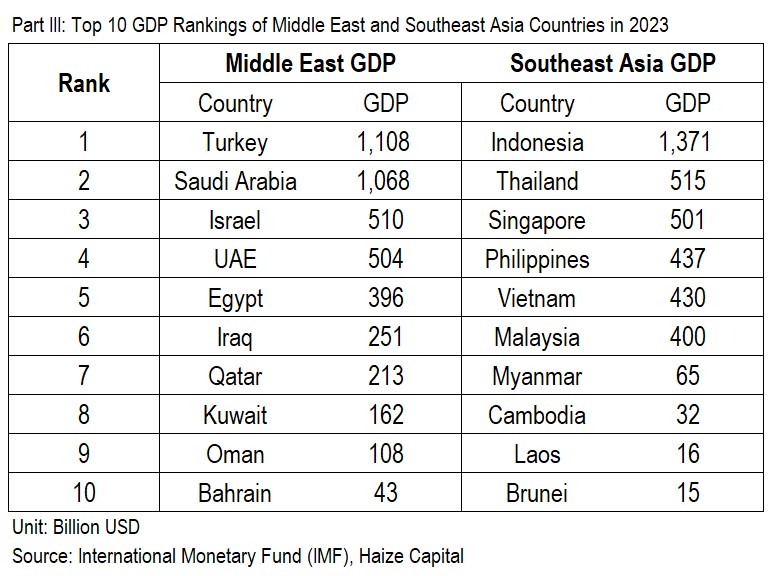

美團由王興在2010年創立,如果不計入對印尼Go-Jek和對印度Swiggy的轉投資,國際化應視2024Q3以Keeta品牌投入利雅德(沙特)為首次出海。考慮到中國市場足堪挖掘,美團國際化的時間較晚可以理解,因為,即便我們用廣義的地域定義(涵蓋北非),來計算中東在網約車和外賣領域的潛在市場,總產值僅百億美元量級,也不到中國的1%。相較來看,中國旅遊公司的國際化,一般先東亞再泛亞,亦即先從鄰近中國的日韓泰開始做起,攜程與同程都不例外。美團的國際化相對較為特殊,在香港之後直接跳級中東。東南亞與中東的差異在於,中東的人數較少,但客單價較高,更有可能快速盈利;但缺點也很明顯,如果將東南亞與中東各國按GDP排序,2023年東南亞榜首印尼接近1.4兆美元,排名第六的馬來西亞已達4,000億美元;但中東落差明顯,土耳其與沙特雖都破有兆美元的GDP,但排名第五(埃及)之後已不足4,000億美元,而且與什葉派及遜尼派國家交好,恐怕也不容易做(排名第三)以色列的生意,真正能經營的國家數/人口數大概率都不如東南亞。

旅遊佈局增添碰撞可能性

雖然兩者的本業都不是旅遊,但顯然雙方都很容易觸及旅遊場景,因為ROI遲早會算起來合理,值得加力投入。

Uber曾在多個地域試點與旅遊相關服務,比如火車票、船運、接送機和禮賓服務,目前大致可從”代駕”與”自駕”理解其佈局。代駕部分自網約車本業添加適合旅遊場景的功能,讓乘客瞭解目的地城市的平均叫車等待時間和乘車費用,並能基於航班資訊獲取機場接送建議時間;自駕部分則與共享用車公司Turo合作,細節我們在海擇觀點談過。

至於美團,就我們所理解,此前並沒有系統性的本地生活角度運營酒旅產品,導致看來更像是低配版(或說是價格敏感版)的攜程。2024年起,美團外賣與美團酒旅開始有較深入的交叉行銷,低星酒店與生活服務有更多融合。有趣的是,Airbnb也在2024Q3說明會更多的將本地生活產品融入旅遊場景,可以說所見略同。

值得注意的是,雙方在旅遊的佈局都沒有想像中快,影響力也沒有想像中大,我們認為部分是因為本地生活的頻次紅利太豐厚,本業的ROI既然仍高,何必多做投入?另一方面,確實也沒找到更好的本機服務/異地旅遊間的融合方式。近期本機服務”旅遊化”開始被重視,具體作法值得觀察。

最初一戰在中東

如果雙方在國際市場發生”本地生活服務”領域的業務碰撞,最可能發生在國際的哪個地域?

我們從國際化先行的Uber切入。Uber在投資人報告提及六個高成長的潛在市場,分別是西班牙、德國、義大利、阿根廷、日本、韓國,除去美團當前還不太可能直接覆蓋的歐洲與南美,剩下日本和韓國。不過,日韓Uber的市場份額較小,面臨當地強大競爭對手Kakao與JapanTaxi的挑戰,其中Kakao在韓國網約車市場的佔有率甚至超過90%,並不具備兩強對撞的土壤,我們還是分得清Uber投資者報告中的幻想與真實。

Uber與美團在各自的擴展路徑上面臨著不同的挑戰,這使得夢幻對決更加難以實現。不過,若把被收購的子公司也涵蓋在內,中東將是雙方最早掀起戰火之處。

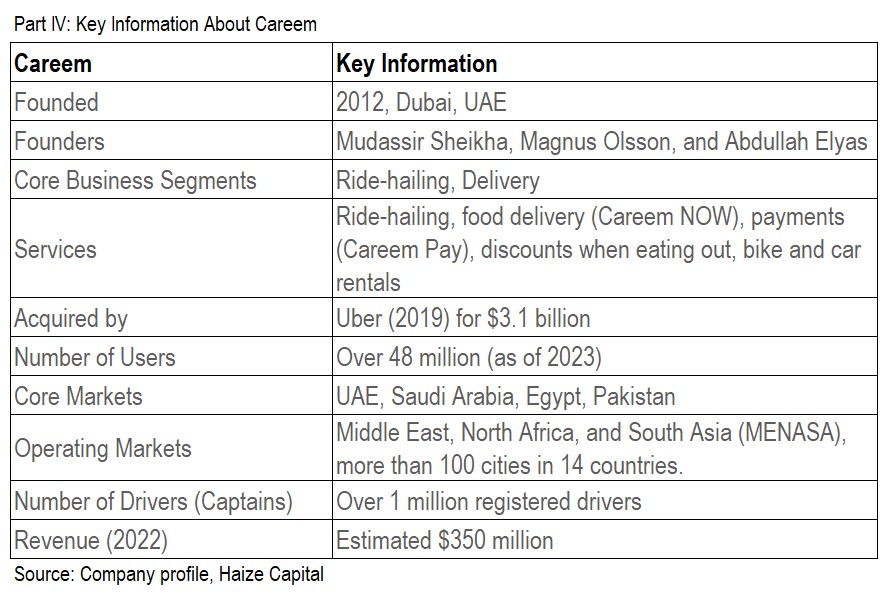

Uber本身雖然在中東影響力不大,但Uber在2019年以31億美金收購的Careem,則是當地的強大玩家。Careem與Uber很像,都從網約車應用,成為集用車、送餐(Careem NOW)、支付(Careem Pay)、配送於一身的超級APP。迄2023年,共覆蓋中東、北非和南亞3個地區、14個國家共100多個城市。2022年收入超過3.5億美元;截至2023年,用戶總數(非為活躍概念)超過4,800萬。

確實如同王興所說,中東不是空白市場與綠地市場(We understand that it's not an empty market, it's not a greenfield market)。美團已在沙特挑戰了Careem,未來還可能在中東其他城市正式壓迫Uber。

好吧,這不是代理人戰爭,而是代理人跟代理人的代理人戰爭,聽起來有點繞口,但也會讓投資人也有點興奮,不是嗎?

------

Haize Capital Insights of the Day

Where Will Uber and Meituan Face Off in a Dream Rivalry?

Meituan (HK: 3690) and Uber (NYSE: UBER) are two prominent internet giants in the global technology and service sectors. Despite their origins in China and the U.S., respectively, their product lines, revenue scales, and market capitalizations make them formidable competitors. If these two companies were to compete, it might be seen as a proxy war between China and the U.S. Where could such a clash occur? In what form and in which regions?

The Most Likely Collision: Local Services

According to Uber’s investor reports, its total addressable market (TAM) is estimated at $12–16 trillion globally, with ride-hailing ($5–10 trillion) as its primary business segment, alongside delivery and freight. On the other hand, Meituan’s IPO estimates suggest that China’s local services sector had a TAM of over $4.5 trillion (33 trillion RMB) in 2023, with the online segment accounting for $1.1 trillion (8 trillion RMB). Around 50% of this online market came from food consumption, while 30% came from hospitality and travel services.

Both Uber and Meituan have developed super-app ecosystems. However, their core differences lie in focus: Uber prioritizes ride-hailing, extending its ecosystem along three lines—frequency, pricing, and usage scenarios. Meanwhile, its delivery service is expanding into groceries and, more recently, on-site services.

Meituan, which emerged victorious from the “Thousand Group War,” became a $100 billion company by evolving from food delivery to a comprehensive local business ecosystem. This ecosystem spans food delivery, in-store dining, grocery retail, and hotel booking. Meituan’s strength in food extends upstream into supply chains and downstream into supplementary services (e.g., “Meituan Seconds”). Despite these successes, Meituan struggles in ride-hailing, where competitors like Didi and Amap dominate the Chinese market.

If Uber and Meituan clash, it will likely be in food delivery and local services rather than ride-hailing, particularly in international markets.

On-Demand Giants: Core Operational Metrics

As leading global on-demand service companies, both Uber and Meituan demonstrate high-frequency consumer demand and significant profit potential. Comparing their Q3 2024 earnings highlights their strengths:

Uber: Revenue reached $11.2 billion (+20% YoY), with net profit exceeding $2.6 billion.

Meituan: Revenue reached $12.8 billion (936 billion RMB, +22% YoY), with net profit of $1.8 billion (129 billion RMB).

In terms of user engagement:

Uber: 2.87 billion orders in Q3 divided among 160 million monthly active users result in an average of 5.9 uses per user per month.

Meituan: With 7.08 billion orders in Q3 and an estimated 500 million annual active users, its user engagement likely surpasses Uber’s.

Internationalization vs. Urban Penetration

The demand for rapid globalization aligns with investor expectations. Uber and Meituan, however, have chosen divergent strategies:

Uber: Focused on internationalization since 2011, starting in Paris, France, and generating 60% of its revenue outside the U.S. It has achieved strong penetration in Latin America, with Brazil reaching a 20% population penetration rate and Mexico exceeding 10%.

Meituan: Prioritized deepening its domestic presence before exploring international opportunities. Its international debut came in 2024Q3 with the Keeta brand in Riyadh, Saudi Arabia.

Tourism: A Possible Expansion Arena

Tourism is not a primary business for either Uber or Meituan, yet both can naturally integrate it into their ecosystems. For Uber, travel-related services like train tickets, ferry rides, airport transfers, and concierge services are logical extensions. Meituan, however, has historically operated tourism products from a local lifestyle perspective, resembling a budget-conscious version of Ctrip. Starting in 2024, Meituan began integrating food delivery with travel marketing.

First Battle: The Middle East

If Uber and Meituan collide in international markets, the Middle East is the likeliest battleground. Uber’s subsidiary Careem, acquired for $3.1 billion in 2019, is a dominant player in the region, offering ride-hailing, food delivery (Careem NOW), and payment services (Careem Pay). By 2023, Careem had operations in 14 countries across the Middle East, North Africa, and South Asia, with revenue exceeding $350 million in 2022.

Meituan’s entry into Saudi Arabia signals its intention to challenge Careem and, indirectly, Uber. While the Middle East is not a greenfield market, its smaller population but higher transaction value per order makes it an intriguing opportunity.

This isn’t just a proxy war—it’s a proxy vs. proxy’s proxy battle. Investors might find this complex competition exciting.