登錄

選單

登錄

海擇短評 Haize Comment:

東亞組團社將迎接怎麼樣的2025?

隨著2025年到來,即使Q4財報尚未放榜,從各地上市公司所披露先期資料,已能大體推斷未來趨勢。從台日韓三地的核心組團旅行社雄獅旅遊、H.I.S及HanaTour來看,雖然復甦程度有異,但仍能觀察出共通趨勢,海擇資本期待所歸納的趨勢,能更有利於旅遊從業者及投資人對2025年的投入方向做出判斷。

Q3是旅遊業重要旺季,也是下一年的試金石,我們歸納台日韓三大組團社的財報做為參考:

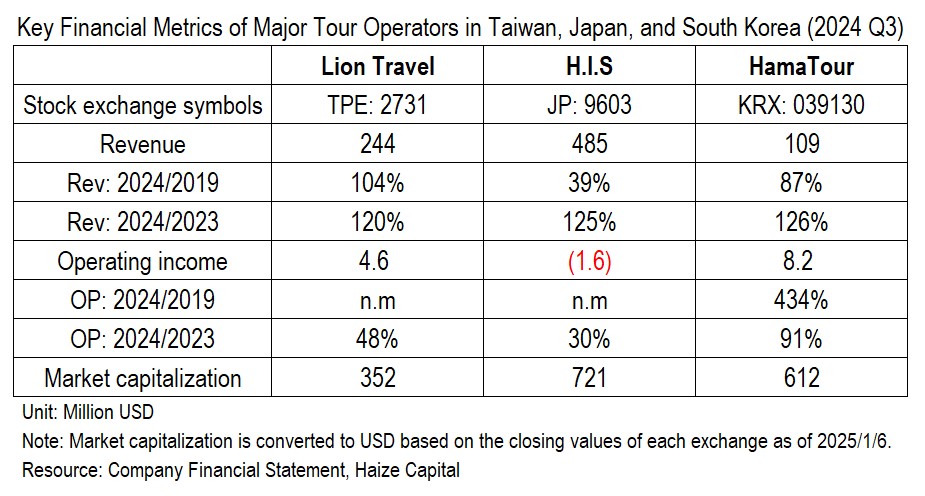

雄獅旅遊(TPE: 2731)收入超2019年同期:雄獅旅遊於2024Q3合併財報收入80.1億台幣(約2.44億美金),較2019年增長4%,較2023年成長20%;營業利益1.50億台幣(約455萬美金),相比2019年虧轉盈,較2023年衰退52%。依今年1月6日當地證交所收盤價,市值116億台幣,約3.52億美金。

HanaTour(KRX: 039130)盈利能力最優:HanaTour於2024Q3合併財報收入1,594億韓元(約1.09億美金),為2019年同期的87%,較2023年成長26%;營業利潤120.26億韓元(約824萬美金),較2019年增長3.3X,較2023年衰退9%。依今年1月6日當地證交所收盤價,HanaTour市值8,934億韓元,約6.12億美金。

H.I.S(JP: 9603)市值最高:H.I.S於2024Q3合併財報收入764億日圓(約4.85億美金),為2019年同期的39%,較2023年成長25%;營業虧損2.56億日圓(約163萬美金),相比2019年盈利113億日圓轉為虧損,但虧損較2023年降低70%。依今年1月6日當地證交所收盤價,市值1135億日圓,約7.21億美金。

這裡我們比對的是各公司在Q3的合併財報,合併財報會納入組團產品以外的收入。比如,雄獅旅遊有5%非團費收入,即FIT收入與其他收入;HanaTour的非團費收入更高,有37%的收入來自於包機航班及酒店訂房的散賣;H.I.S在疫情後售出了豪斯登堡,財報整整少了一整個事業部(ハウステンボスグループ),不過仍有82%的收入來自旅遊事業。大體上來說,我們認為公司整體的收入/損益現況以及與2019年的對比,仍相當精准反映了組團社的運營現況,並未改變做為組團社的定位。

三大組團社的復甦現狀容有不同,比如雄獅的收入超過2019年同期,但H.I.S的收入不到2019年同期的40%,但結合財報的細部內容與歷史變化,我們認為,有五個趨勢正在發生:

1. 報復性旅遊潮回歸常態:從2024年暑假開始,台日韓三地組團社的報復性旅遊潮正在快速回歸常態。三大組團社Q2到Q3的QoQ收入增速都低於2023年同期,H.I.S的收入甚至出現季減,無論是合併報表或單看旅行事業都是如此。更值得注意的是,除了H.I.S,盈利能力都較2023年同期衰退,雄獅旅遊甚至降低超過一半;而H.I.S雖然沒有衰退,但2023Q3也呈現虧損,2024年只是減虧而已。

2. 日本以外的新目的地正在出現:以韓國HanaTour為例,雖然Q3的總出團人數還有3%的增速,但後疫情深受歡迎的日本目的地,2024年以來出行人次已持續減少。HanaTour團隊遊輸送到日本的人數在Q1、Q2、Q3,分別為16.4萬人、14.3萬人、12.9萬人。韓國另一家上市組團社ModeTour的減幅更為劇烈。相比之下,輸送到中國的人數則持續增加,從Q1的4.0萬人到Q3的超過8萬人,增長翻倍。我們認為並非每個團客都對深耕日本的低線城市感興趣,他們會開始挖掘更新鮮的目的地;但日本仍是自由行旅客的重要目的地。

3. 降本增效會是長久趨勢:日本H.I.S在Q3旅行事業的員工數為8,748人,較2019年同期的13,209人,大幅減少34%。HanaTour與雄獅旅遊雖然沒有公告員工數,但是前者歸屬於費用的員工支出,在Q3較2019年同期減少26%,後者在員工福利的提撥費用也有類似的趨勢,我們認為這都反映了員工數減少。而且未來可能不會再增回原來的規模,因為AI確實減少了不少人力。

4. 組團社難以打造OTA基因:疫情間各組團社可能基於客戶需求增加在互聯網的投入,在APP或移動設備的月活躍大有增長,比如HanaTour的月活為123萬,甚至超過Triple及Myrealtrip,但遺憾的是,FIT及元件產品的銷售始終拉不上來,HanaTour機酒產品在Q3收入占比37%與四年前基本一致;雄獅比較好,四年占比接近翻了一倍,但FIT收入加上其它收入也只是從3%到5%,團費收入仍為主要的路徑依賴。

5. 2019的送客規模難再:即便後疫情期增長迅速,但各社距離恢復到疫情前的送客規模仍有很大差距。HanaTour今年1月至10月的跟團旅遊累計送客數量為175.4萬人次,僅達當年的69%,雄獅的出團數也僅約2019年的七成,兩者驚人相似,我們認為這個趨勢與OTA在疫情間快速蠶食組團社客源的現象有關,這點在日本的組團社也同步發生,而且影響更為劇烈。

------

Haize Capital Insights of the Day

What Awaits East Asia’s Tour Operators in 2025?

As 2025 begins, despite Q4 financial reports not yet being released, preliminary disclosures by publicly listed companies in Taiwan, Japan, and South Korea provide valuable insights into future trends. Examining core tour operators such as Lion Travel (Taiwan), H.I.S. (Japan), and HanaTour (South Korea), we observe distinct recovery levels but also common patterns. Haize Capital has summarized these trends to help tourism professionals and investors better align their strategies for 2025.

Q3: A Key Indicator for Tourism Recovery

2024Q3 is a crucial peak season for the tourism industry and serves as a litmus test for the following year. We analyzed the Q3 consolidated financial reports of major tour operators in Taiwan, Japan, and South Korea as a reference:

Lion Travel (TPE: 2731) exceeded its 2019 revenue levels:

Lion Travel’s consolidated Q3 2024 revenue reached TWD 8.01 billion (approximately USD 244 million), marking a 4% increase from 2019 and a 20% growth compared to 2023. Operating profit was TWD 150 million (approximately USD 4.55 million), representing a turnaround from losses in 2019 but a 52% decline from 2023. As of January 6, 2025, the company’s market capitalization stood at TWD 11.6 billion (approximately USD 352 million).

HanaTour (KRX: 039130) showcased the highest profitability:

HanaTour reported Q3 2024 revenue of KRW 159.4 billion (approximately USD 109 million), 87% of its 2019 level, and a 26% increase from 2023. Operating profit reached KRW 12.026 billion (approximately USD 8.24 million), representing a 3.3x increase from 2019 but a 9% decline from 2023. As of January 6, 2025, HanaTour’s market capitalization was KRW 893.4 billion (approximately USD 612 million).

H.I.S. (JP: 9603) had the highest market capitalization:

H.I.S. reported Q3 2024 revenue of JPY 76.4 billion (approximately USD 485 million), 39% of its 2019 level and a 25% increase from 2023. The company posted an operating loss of JPY 256 million (approximately USD 1.63 million), compared to an operating profit of JPY 11.3 billion in 2019. However, this loss was 70% less than in 2023. As of January 6, 2025, its market capitalization was JPY 113.5 billion (approximately USD 721 million).

Consolidated Financial Reports Reflect Broader Operations

These consolidated reports include non-tour product revenues, such as Lion Travel’s 5% revenue from FIT (Free Independent Traveler) and other sources, HanaTour’s 37% revenue from chartered flights and standalone hotel bookings, and H.I.S., which has divested from its Huis Ten Bosch Group. Despite these nuances, the overall financial performance and comparisons to 2019 accurately reflect the operational status of these tour operators without altering their positioning.

Five Key Trends for 2025

Revenge Travel Fades to Normalcy:

Since the summer of 2024, the post-pandemic surge in “revenge travel” across Taiwan, Japan, and South Korea has been rapidly normalizing. QoQ revenue growth from Q2 to Q3 for all three operators was lower than in 2023, with H.I.S. even reporting a sequential revenue decline. Moreover, profitability declined across the board compared to 2023, with Lion Travel’s operating profit halving. While H.I.S. reduced losses, it remained unprofitable in Q3 2024.

Emergence of New Destinations Outside Japan:

HanaTour’s Q3 total group tour volume grew by 3%, but trips to Japan, a popular post-pandemic destination, declined throughout 2024 (164,000 in Q1 to 129,000 in Q3). Conversely, group tours to China doubled from 40,000 in Q1 to over 80,000 in Q3. This shift suggests that not all group travelers are interested in exploring Japan’s less mainstream destinations, opting instead for newer locations. However, Japan remains a key destination for independent travelers.

Cost Reduction and Efficiency Gains Are Here to Stay:

H.I.S. reduced its travel business workforce by 34%, from 13,209 employees in 2019 to 8,748 in Q3 2024. HanaTour and Lion Travel also cut employee-related expenses by 26% and similar margins, respectively, reflecting workforce reductions. These changes, driven partly by AI adoption, are unlikely to be reversed.

Difficulty Adopting OTA Characteristics:

Despite increased investments in digital platforms during the pandemic, tour operators struggle to grow FIT and dynamic packaging sales. HanaTour’s Q3 revenue from flights and hotels remained at 37%, unchanged from four years ago. Lion Travel improved its FIT revenue share from 3% to 5% but remains heavily reliant on group tour revenue.

2019 Passenger Volumes May Be Unattainable:

Despite post-pandemic growth, none of the operators have returned to pre-pandemic passenger levels. HanaTour’s cumulative group tour passengers from January to October 2024 reached 1.754 million, only 69% of 2019 levels. Lion Travel reported similar figures at around 70% of 2019 group departures. This trend reflects OTAs’ rapid encroachment on traditional tour operators’ customer base during the pandemic, a phenomenon particularly pronounced in Japan.