登錄

選單

登錄

海擇短評 Haize Comment:

中國遊客帶動韓國入境遊經濟之後

韓國傳統上被視為龐大的出境旅遊市場,這個擁有5,000萬人口的國家,出境人次每每能超過1.2億人口的日本。然而,隨著全球旅遊市場的逐步復甦,在中國遊客帶動之下,2024年韓國的入境旅遊開始展現出可觀的經濟效益。這種轉變不僅改變了韓國旅遊業的發展方向,也為市場帶來了新的機遇。海擇資本將透過信用卡交易數據說明並驗證這一趨勢。

韓國旅遊行業處於零售消費的火車頭

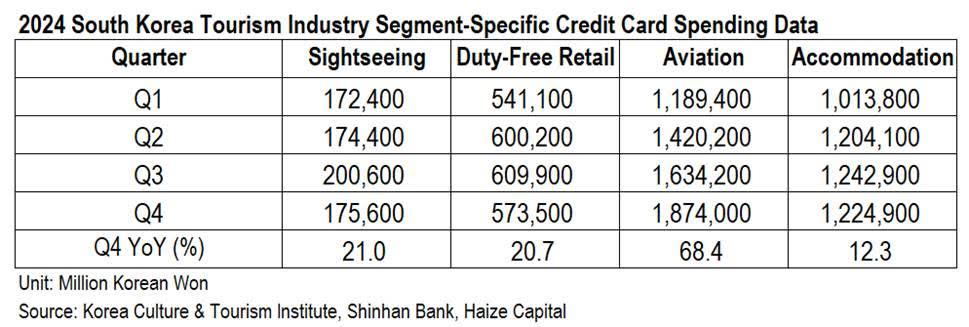

韓國文化觀光研究院提供以新韓銀行作為收單銀行的信用卡交易數據報告,數據顯示Q4國內外信用卡消費總額達148.8兆韓元(約1,019億美元),YoY增長2.1%;其中休閒活動(文化/運動/旅遊)領域佔整體的11.6%,達17.4兆韓元(約119億美元),YoY增長8.1%,增速優於整體增速;而旅遊四大細分領域的增速又都高於包括整體旅遊在內的休閒活動領域,足證明韓國旅遊行業處於零售消費的火車頭。

其中旅遊四大細分領域(觀光業/免稅店業/航空業/住宿業)的數據還揭示了一個有趣的消費模式:韓國人在選擇不同國家旅遊時,雖然機票費用會有所差異,但在住宿與購物方面的支出卻基本保持一致。換言之,韓國旅客在機票之外的總體消費水平是固定的,而非根據當地物價進行調整。

這一現象帶來了一些有趣的影響。例如,前往東南亞等低物價國家的韓國遊客往往會選擇較高端的住宿與購物體驗,而在歐美等高消費國家,則可能為了維持預算而選擇較為節儉的住宿方式。這對旅遊業者而言具有重要啟示:短途市場(如東南亞)的地接產品可以朝高端化發展;而長途市場(如歐美)或可考慮提供更具成本效益的旅遊選擇。

外國遊客的消費正在重塑韓國旅遊市場

根據2024Q4的信用卡消費數據,韓國國內居民在休閒活動(文化/運動/旅遊…)領域的信用卡消費總額達12.2兆韓元(約83.5億美元),而同期外國旅客的信用卡消費總額已達5.2兆韓元(約35.6億美元),占整體市場的29.4%,幾乎接近三分之一。這一比例顯示,韓國旅遊業已經朝向更依賴國際旅客的方向發展,成為一個”旅遊外匯導向”的國家。

雖然目前韓國觀光公社(KTO)尚未公佈韓國2024Q4國內旅遊市場的旅遊人次數據,但若以2019年3.8億的國內旅遊人次作為基準推斷,假設2024年已恢復至疫情前水平,則全年國內旅遊人次仍接近3.8億,每季至少有數千萬韓國人進行國內旅遊。將此數據與2024Q4總入境外國遊客436萬人次對比,足以顯示外國旅客的消費影響力正快速擴大。

主要客源國的消費特徵與比較

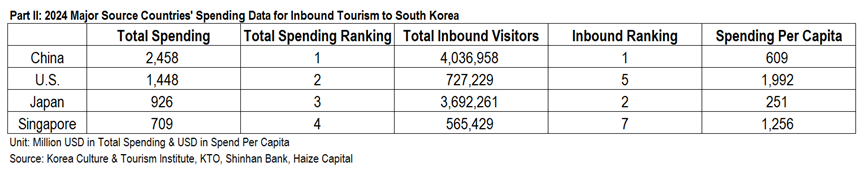

從2024全年數據來看,外國人在韓國的信用卡總消費額達18兆韓元,其中,中國(3.6兆韓元)、美國(2.1兆韓元)、日本(1.4兆韓元)與新加坡(1.0兆韓元)為前四大消費客源國。然而,值得注意的是,雖然日本是韓國最大的入境客源國,但其人均消費水平遠低於中國、美國和新加坡。

如果將這四大國的信用卡消費總額除以全年入境人次,則可得出人均信用卡消費額如下:

‧ 中國:88.9萬韓元(約609美元)

‧ 美國:290.9萬韓元(約1,992美元)

‧ 日本:36.7萬韓元(約251美元)

‧ 新加坡:183.4萬韓元(約1,256美元)

從數據分析來看,中日兩客源國年入境韓國約400萬人次,中國旅客的總體消費為日本遊客的1.5倍,這或許與日本遊客偏好短期旅行、消費因匯率而趨於節儉有關。另一方面,美國和新加坡遊客

的年入境人數均超過50萬人次,但其人均消費額遠高於中國遊客,甚至達到中國遊客的1至2倍。這些數據顯示,韓國政府應會加大對這些高消費群體的吸引力度。

信用卡數據的補充說明

新韓銀行(Shinhan Bank)作為韓國主要的商業銀行之一,在韓國銀行業中占有重要地位。根據2024Q1的市場份額數據,新韓銀行在存款市場的地位僅次於KB國民銀行與NH農協銀行。韓國境內外遊客在韓國使用其本國信用卡消費時,這些交易會經由新韓銀行的支付系統或POS機處理,從而計入新韓銀行的交易數據;考慮到單季信用卡消費額已達千億美元量級,我們仍認為該數據具有極高的參考價值。

雖然新韓銀行作為收單銀行的信用卡交易數據,為市場分析提供了重要參考,但仍存在一定的局限性。首先,信用卡交易無法完全反映旅客的所有消費行為,特別是在電子支付領域。韓國的高佔比電子支付系統中,僅Samsung Pay需綁定信用卡才能使用,而KakaoPay、Naver Pay及預付卡類的T-Money和 WOWPASS等並不需要綁定信用卡,因此這些交易並未被計入信用卡支付樣本。此外,中國遊客常用的支付寶與微信支付也不需綁定信用卡,這進一步降低了信用卡數據的代表性。

韓國旅遊業的未來機遇

韓國旅遊市場正逐步轉向更加依賴外國遊客的模式,外國遊客的消費已占韓國旅遊收入的近30%,其中,中國、美國和新加坡遊客的消費力尤其強勁,這一趨勢可能改變過去東北亞旅遊市場的格局。傳統上,韓國是主要的出境旅遊市場,而日本則是主要的入境旅遊市場。然而,隨著韓國入境市場的快速增長,未來韓國有可能成為一個同時具備龐大出境與入境旅遊規模的國家,並在入境旅遊市場上與日本形成競爭。

當然,在玩樂產品的豐富程度、地接社語言服務資源等方面,韓國與日本仍存在顯著差距。然而,透過針對不同市場的需求,韓國政府與旅遊業者有極高動機提升旅遊競爭力,而對供應鏈的相關業者來說,這也許是一個值得關注的新機遇。

----

Haize Capital Insights of the Day

China’s Tourists Drive South Korea’s Inbound Tourism Economy

South Korea has traditionally been recognized as a major outbound tourism market. Despite its population of just 50 million, the country's outbound travel volume often surpasses that of Japan, which has a population of 120 million. However, as the global travel market gradually recovers, 2024 has brought a new economic outlook for South Korea’s inbound tourism, largely driven by Chinese tourists. This shift is not only altering the trajectory of South Korea’s tourism industry but also creating new opportunities for the market. Haize Capital aims to analyze and validate this trend through credit card transaction data.

South Korea’s Tourism Industry: The Engine of Retail Consumption

A report by the Korea Culture & Tourism Institute, based on credit card transaction data processed by Shinhan Bank as the acquiring bank, provides valuable insights. In Q4 2024, domestic and international credit card spending in South Korea reached KRW 148.8 trillion (approximately USD 101.9 billion), reflecting a 2.1% year-on-year (YoY) growth. Within this, the leisure sector (covering culture, sports, and tourism) accounted for 11.6% of total spending, amounting to KRW 17.4 trillion (USD 11.9 billion), with an 8.1% YoY growth, outperforming overall consumer spending growth. Notably, the four key tourism subsectors saw even higher growth than the broader leisure sector, reinforcing the crucial role of tourism as a key driver of retail consumption in South Korea.

The four major tourism subsectors—sightseeing, duty-free retail, aviation, and accommodation—also reveal an interesting consumer pattern. While airfare costs vary depending on the destination, South Korean travelers tend to maintain a consistent level of spending on accommodation and shopping, regardless of the price levels in their travel destinations.

This phenomenon leads to important strategic implications. For example, South Korean travelers heading to lower-cost destinations such as Southeast Asia are more likely to indulge in premium accommodations and shopping experiences. Conversely, when traveling to high-cost regions like Europe and North America, they may opt for more budget-conscious accommodations to maintain overall expenditure levels. For travel operators, this suggests that short-haul markets like Southeast Asia should focus on offering premium products, while long-haul destinations in Europe and North America should consider providing more cost-efficient travel options.

Foreign Tourists Are Reshaping South Korea’s Tourism Market

According to Q4 2024 credit card transaction data, South Korean residents spent KRW 12.2 trillion (USD 8.35 billion) on leisure activities (including culture, sports, and tourism). Meanwhile, international visitors spent KRW 5.2 trillion (USD 3.56 billion) during the same period, accounting for 29.4% of total spending, nearly one-third. This proportion highlights South Korea's increasing dependence on international tourists, solidifying its transformation into a “tourism foreign exchange-driven” economy.

While the Korea Tourism Organization (KTO) has not yet released official Q4 2024 data on domestic tourism volume, estimates based on 2019’s 380 million domestic trips suggest that if the market has recovered to pre-pandemic levels, total domestic tourism trips in 2024 would likely remain close to this figure, with at least several tens of millions of South Koreans traveling domestically each quarter. Comparing this with the 4.36 million inbound foreign visitors in Q4 2024, it is clear that foreign tourists are playing an increasingly significant role in South Korea’s tourism economy.

Consumption Characteristics and Comparisons Among Key Source Markets

For the full year 2024, foreign visitors spent a total of KRW 18 trillion in South Korea, with the top four source markets being:

‧ China: KRW 3.6 trillion

‧ United States: KRW 2.1 trillion

‧ Japan: KRW 1.4 trillion

‧ Singapore: KRW 1.0 trillion

A crucial observation is that while Japan remains South Korea’s largest inbound source market, its per capita spending is significantly lower than that of Chinese, American, and Singaporean tourists.

By dividing the total credit card spending by the number of annual inbound visitors from each country, the following per capita credit card spending figures emerge:

‧ China: KRW 889,000 (approx. USD 609)

‧ United States: KRW 2.91 million (approx. USD 1,992)

‧ Japan: KRW 367,000 (approx. USD 251)

‧ Singapore: KRW 1.83 million (approx. USD 1,256)

Among the two largest visitor groups—China and Japan, each with approximately 4 million visitors per year—Chinese tourists spent 1.5 times more than Japanese tourists. This discrepancy may be attributed to Japanese tourists' tendency for shorter trips and more frugal spending habits, influenced by exchange rate fluctuations. Meanwhile, American and Singaporean visitors, though their annual inbound numbers exceed 500,000, demonstrate significantly higher per capita spending, reaching 1–2 times that of Chinese tourists. These insights suggest that the South Korean government may place greater emphasis on attracting these high-spending tourist groups.

Understanding the Credit Card Data Limitations

As one of South Korea’s leading commercial banks, Shinhan Bank plays a crucial role in the country’s financial sector. As of Q1 2024, it ranks just behind KB Kookmin Bank and NH Nonghyup Bank in terms of deposit market share. When domestic and foreign tourists use their credit cards in South Korea, these transactions are processed through Shinhan Bank’s payment network or POS systems, contributing to the bank’s transaction data. Given that quarterly credit card spending already surpasses USD 100 billion, this dataset remains an invaluable reference for market analysis.

However, Shinhan Bank’s credit card transaction data has inherent limitations. Firstly, it does not capture all tourist expenditures, particularly in the field of digital payments. South Korea has a high penetration of digital payment systems, and while Samsung Pay requires a credit card linkage, services such as KakaoPay, Naver Pay, and prepaid cards like T-Money and WOWPASS do not require credit card binding, meaning their transactions are not included in this dataset. Additionally, Chinese tourists frequently use Alipay and WeChat Pay, which also do not require credit card binding. As a result, credit card transaction data underrepresents the total spending of visitors who primarily use these alternative payment methods.

Future Opportunities in South Korea’s Tourism Industry

South Korea’s tourism sector is undergoing a profound shift toward greater reliance on international visitors, with foreign tourists’ spending now accounting for nearly 30% of total tourism revenue. Among them, China, the U.S., and Singapore stand out as the most significant source markets in terms of spending power. This trend may reshape the traditional tourism landscape in Northeast Asia. Historically, South Korea has been a dominant outbound tourism market, while Japan has been a major inbound tourism destination. However, with South Korea’s inbound tourism segment expanding rapidly, the country may soon become a major player in both inbound and outbound tourism, positioning itself as a competitor to Japan in attracting international visitors.

Despite these opportunities, South Korea still faces significant gaps compared to Japan in terms of entertainment offerings, language capabilities among tour operators, and the overall depth of tourism infrastructure. However, recognizing the shifting trends, the South Korean government and tourism industry stakeholders have strong incentives to enhance the country’s tourism competitiveness. By refining marketing strategies tailored to different markets—whether through premium product offerings, luxury shopping incentives, or VIP experiences tied to Korean pop culture—South Korea has a compelling opportunity to strengthen its position in the global tourism landscape. For supply chain stakeholders, this evolving market presents a new frontier of opportunities worth close attention.