登錄

選單

登錄

海擇短評 Haize Comment:

中國赴韓團隊免簽:新政下的區域競爭與產業機會

韓國代理總統兼經濟副總理崔相穆(최상목)近期在施政報告會議中宣布,韓國將於4月公告針對中國旅客的團隊遊免簽政策,並預計於第三季正式生效。這項政策的核心,在於透過有條件的免簽制度,促進中國旅客入境,進而推動整體觀光與經濟發展。其力度與彈性備受關注,政策不容易重塑東北亞旅遊格局,但能為韓國旅遊行業打下更扎實的基業。

從郵輪開放到陸路團體免簽

早在2023年,韓國已恢復疫前針對郵輪旅客的免簽政策,當時針對符合條件的所有國際遊客,提供最長90天的入境免簽期。到了2024年底,韓國針對中國郵輪旅客推出特殊免簽待遇,允許停留最多三日,這意味著韓國已提高中國旅遊客源市場的優先級。如今,即將上路的團隊免簽政策則進一步擴及陸路與空路入境,範圍與彈性遠高於先前措施。

新政觀察三重點:定向、定義與停留彈性

海擇資本認為,此次新免簽政策的觀察重點有三:

首先,這是針對特定市場的定向政策,目標明指中國市場。該政策體現韓國政府認為,中國旅客即便在2024年已是最大占比的客源國(280萬人次、32%),但在絕對值上仍有大幅增長潛力。

其次,4月將正式公告的政策,其”團隊”的定義與執行方式尤為關鍵。儘管可以預期需由旅行社辦理相關手續與名單報備,但若只要求由旅行社安排入出境,而行程安排允許旅客高自由度參與,而非對時間地點高度管控,這對中國業界而言將是一項極大利多。旅行社在風險可控的前提下,或可透過半自由行或套裝自由行等產品組合迅速拓展客源。

第三,免簽停留期限若能達到一至兩週的彈性空間,將有利於深度旅遊產品的發展。雖不及日本等傳統免簽國90天寬鬆,但對大多數短中線路已綽綽有餘。

積極政策背後的戰略意圖

我們之所以對該政策抱持樂觀預期,來自兩項系統性觀察。

首先,在本次韓國”國民經濟審議會議(민생경제점검회의)”中,旅遊被明確納入推動內需的支柱產業。儘管會議未明說,但整體語境已將日本視為入境競爭假想敵,而中國為兩地共同的重要潛在客源地。韓國若要在東北亞甚至泛東亞入境旅遊中勝出,勢必得在制度與資源更積極投入。

其次,韓國政府在會議中,同時表明將透過市場、產品與路線的多樣化策略,推進以”K-everything”為核心的體驗型旅遊產品與非首都圈觀光資源開發。這意味著韓國正試圖擺脫傳統跟團模式的旅遊依賴,轉向體驗導向與市場細分。

與日本的競爭關係:潛力與壓力並存

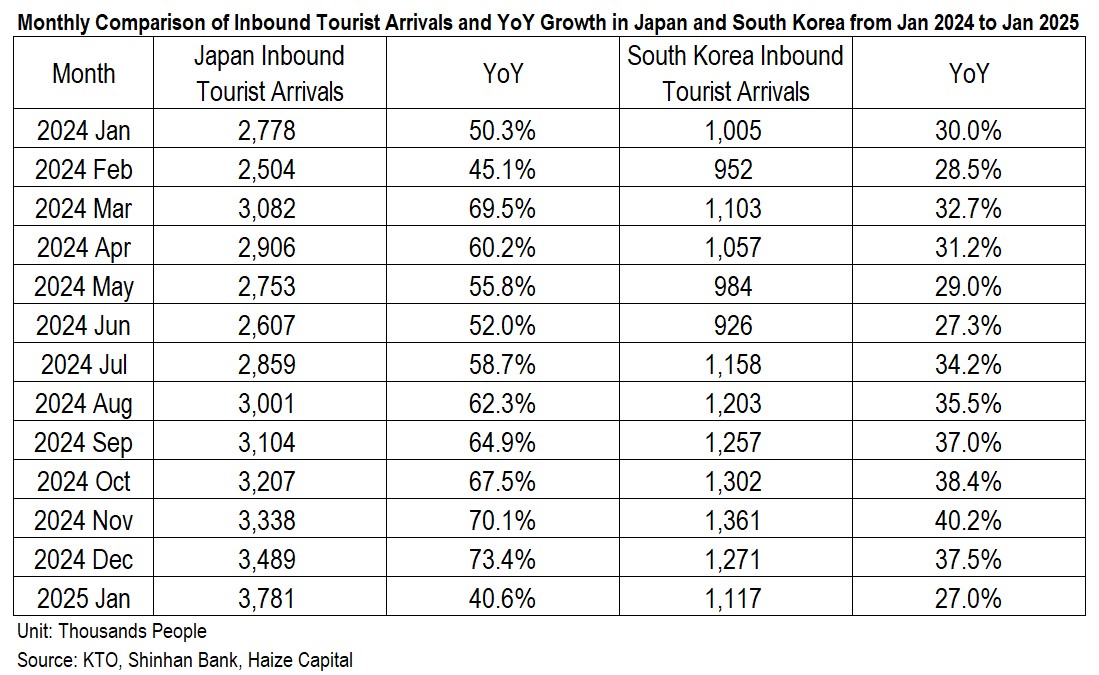

2025年1月,韓國入境旅客人次年比增長27%,較2019年同期更增長39%,展現疫後強勢復甦動能。但同月日本則在高基期下仍實現41%增幅,顯示其接待能力與國際吸引力仍更勝一籌。即便以模型還原國土面積與人口結構再與日本相比,韓國的入境潛力仍有很大的成長空間。

政策投放之後,韓國還面臨是否能持續增加一線城市產品的深度廣度,同時引導低線城市觀光基礎建設,才能達到其所預期的擴張。

誰將真正受惠?

若從產業結構來看,最直接受惠的將是韓國地接旅行社與底層產品供應商。尤其是體驗類活動提供者,將因旅客停留時間增加與政策鼓勵率先受益。

這同時也代表更高的服務品質與接待能力門檻,企業若能在政策紅利期建立獨有定位,將有機會在疫後重塑產業格局中,更好的藉由投資人挹注更進一步成長。

---

Haize Capital Insights of the Day

China Visa-Free Group Travel to Korea: Regional Competition and Industry Opportunities under a New Policy

Acting President and Deputy Prime Minister for Economic Affairs of South Korea, Choi Sang-mok (최상목), recently announced at a policy briefing that the government will implement a conditional visa-free policy for Chinese group travelers. The details of the policy will be officially released in April, with implementation expected in the third quarter. The core of the policy lies in encouraging inbound tourism from China through regulated visa exemptions, with the aim of revitalizing South Korea’s tourism sector and boosting its economy. While the policy alone may not reshape the travel landscape of Northeast Asia, it could lay a more solid foundation for Korea's tourism industry.

From Cruise Arrivals to Land and Air Group Entry

Back in 2023, Korea reinstated its pre-pandemic visa-free entry policy for cruise passengers, allowing eligible international visitors to stay for up to 90 days. At the end of 2024, a special exemption was granted to Chinese cruise travelers, allowing them to stay in Korea for up to three days—an indication that China’s outbound tourism market had become a strategic priority. The upcoming policy will extend visa-free entry beyond cruise arrivals to include land and air travel, with significantly broader scope and flexibility.

Three Key Aspects to Watch: Targeting, Definition, and Duration

Haize Capital identifies three key dimensions worth monitoring in this new visa policy:

First, this is a highly targeted policy, aimed squarely at the Chinese market. Even though Chinese tourists already accounted for the largest share of Korea’s inbound visitors in 2024 (2.8 million, or 32%), the government sees substantial room for further growth in absolute numbers.

Second, the definition and enforcement of the term “group” will be crucial. If the policy merely requires entry and exit to be handled through a registered travel agency—while allowing participants high freedom in their on-ground itineraries—it would be a major boon for the Chinese travel industry. Under manageable risk, travel agencies could rapidly scale operations through semi-independent or flexible tour packages.

Third, if the visa-free stay period offers one to two weeks of flexibility, it would support the development of more in-depth travel products. Although it would still fall short of the 90-day visa-free access granted by traditional markets like Japan, the proposed duration would more than suffice for most short- to medium-length trips.

Strategic Implications Behind the Policy

We are optimistic about this policy’s rollout, based on two structural observations:

First, in the latest Korean “National Economic Policy Review Meeting (민생경제점검회의),” tourism was officially designated a pillar industry for boosting domestic demand. Although Japan was not mentioned by name, the tone of the discussion implicitly positioned Japan as Korea’s primary competitor in the inbound tourism space. Meanwhile, China remains the most important potential source market for both countries.

Second, the Korean government expressed its intention to pursue market, product, and route diversification, promoting experience-based travel under the “K-everything” banner and developing tourism resources beyond Seoul. This reflects a strategic shift away from traditional group tours toward a more segmented and experiential approach.

Japan as Benchmark: Room for Growth Amid Pressure

In January 2025, Korea’s inbound tourism rose 27% year-on-year and 39% compared to the same period in 2019, showing strong post-pandemic recovery momentum. However, Japan, operating from a much larger base, still achieved 41% year-on-year growth in the same month—demonstrating its superior capacity and international appeal.

Even when adjusting for national size and population, Korea’s inbound tourism still has considerable growth potential. Moving forward, the challenge will be to expand the depth and breadth of tourism products in major cities while developing tourism infrastructure in lower-tier cities to achieve balanced expansion.

Who Stands to Benefit?

From an industry structure perspective, the most direct beneficiaries of the new policy will be Korean inbound tour operators and base-level service providers. In particular, providers of local experiences and activities are expected to gain early traction due to extended stays and more flexible itineraries.

However, this also implies higher expectations in service quality and operational capacity. Companies that can establish a clear position during this policy window will be better placed to attract post-pandemic investment and achieve sustained growth as the industry reshapes itself.