登錄

選單

登錄

海擇短評 Haize Comment:

同程國際化很艱難,但,不影響盈利!

同程近期公告2024年報,如同其他OTA,仍展現穩定且良好的盈利能力。作為一家全國型而非國際型的OTA,同程在國際化發展上的進展仍然緩慢,AI和度假事業的成效目前對整體營運也尚未構成決定性影響。然而,這些因素並未阻礙它成為一家可持續增長盈利的OTA,它已經成功跨越了基本門檻,具備穩定經營的核心條件。

增長趨勢回歸季節性節奏

2024年同程的增長趨勢回歸季節性節奏,缺乏重大結構性變動,因此在財務面,我們不特別聚焦Q4財報,而是直接討論全年數據。

2024年同程全年收入達173億人民幣,年增46%;年內溢利為19.9億元,年增 27%。同程亦宣布每股派發0.18港元的現金股息,較去年成長20%,顯示其仍穩健執行境內外主流OTA的股東回報模式,具備長期收益潛力。

那些無關勝敗的戰場:國際化、AI與度假事業

本季同程的國際化發展呈現分流現象。根據公告,出境票務佔交通票務收入超5%.整體國際化相較於Q3,我們不認為有重大突破。從個別產品線來看,國際機票票務量在Q4年增超過130%,全年國際住宿業務間夜數則年增超過110%;相較Q3,當時機票增速為110%、住宿為130%,顯示出國際住宿成長相對放緩,機票成為主導國際化的核心推手,增長來源則集中在日本、韓國、馬來西亞與新加坡等目的地。

在AI布局方面,同程推出自研生成式AI”程心”。該工具不僅具備飯店比較功能,實測顯示其方向更類似於攜程的TripGene,提供全方位的內容推薦,而非 Booking的AI Agent,以酒店導購為唯一方向,但境外內容精準度仍有待提升。我們認為,同程談到的如數位導遊、語音互動、個人化推薦等功能,未來預計並不難實現,但全球而言,AI要成為主要流量入口仍需時間。

至於旅遊事業,同程已成功跨過盈虧平衡點,全年收入為31.4億人民幣,佔集團總收入約18%,惟利潤率僅2.3%,對整體獲利貢獻仍有限。

整體而言,從盈利貢獻與運營數據增長來看,國際化、AI、與度假業務目前尚”無關勝敗”。

同程的金庫密碼

若上述事業皆非關鍵,那麼同程盈利持續擴張的根本原因為何?海擇資本認為,從兩項關鍵數據中可見端倪:

首先是佣金快速成長-2023年度假事業尚未納入同程財報統計,若將其影響剔除,並假設度假業務佣金率為10%,則2024年核心在線旅遊平台的總交易額約為2,243億人民幣,反而低於2023年的2,388億元。然而,即便GMV較低,2024年核心在線旅遊平台收入卻年增22%至人民幣142億元,其中交通票務與住宿預訂皆增長20%,其他收入(包含酒店管理)則年增35%,顯示從交易額到收入的轉化強勁成長。結合對比相關要素,我們認為同程收入與盈利的成長,更多來自於對底層供應商(如酒店)的議價與變現能力,而非單純的訂單或用戶數成長。

其次是自有流量與費用控制-同程自有APP的全年日活(DAU)增長逾一倍,雖未公布小程序DAU數據,但APP的DAU增長,明顯有助於降低拉新費用的依賴,使行銷成本更加可控。這從Q4收入年增35%,行銷費用僅年增14%,研發費用甚至微幅下滑可見一斑;我們認為,若進一步排除度假業務影響,費用率將更具彈性與優勢。

穩健生長的根源

從2023年至2024年,同程的年付費用戶僅從2.35億增至約2.38億,年增僅 1.5%;但核心在線旅遊平台收入卻年增22%,經營溢利年增29%。這可以理解為,一群穩定的付費用戶,在略為提高消費頻次(2024年每個年付費用戶平均消費8.1次,2023年則為7.5次)的現況下,為公司帶來大額收入與盈利。

我們認為,這種現象的背後,是中國旅遊市場供過於求的結構性現實。底層供應商過剩使平台議價能力大增,產生平台紅利。這不僅是同程的利多,也同樣出現在攜程與美團等平台身上。雖然單純從中國OTA平台的佣金率來看,不如歐美巨頭,一旦加上廣告排序與付費曝光等變現方式,利潤率便顯著放大,這在住宿領域尤為明顯。

而在交通業務方面,雖然前返偏低甚至為零,但透過APP進入平台的用戶,其購買打包服務(BAF, Bundled Ancillary Fees)時產生的利潤差異顯著,尤其是在退改等環節,成為同程及眾中系OTA極為重要的盈利來源之一。

總結來說,即便同程在國際化推進仍慢、AI尚未成為主力流量入口、度假事業貢獻有限,但只要機票與酒店生態不變,供需結構維持,同程的盈利能力就屬可持續,甚至仍有進一步放大的空間。

---

Haize Capital Insights of the Day

Tongcheng’s Internationalization Is Challenging — But It Doesn’t Affect Profitability!

Tongcheng recently released its 2024 annual report. Like other OTAs, it continues to demonstrate stable and solid profitability. As a nationwide rather than international OTA, Tongcheng’s progress in globalization remains slow, and current developments in AI and the vacation business have yet to make a decisive impact on overall operations. However, these factors have not hindered its ability to become a sustainably profitable OTA. Tongcheng has already crossed the fundamental threshold and possesses the core conditions for stable operations.

Growth Trend Returns to Seasonal Rhythm

In 2024, Tongcheng’s growth trend returned to a seasonal rhythm, with no major structural changes. Therefore, from a financial perspective, we focus less on the Q4 results and instead discuss the full-year data directly.

Tongcheng reported annual revenue of RMB 17.3 billion in 2024, representing a 46% year-on-year increase. Net profit for the year reached RMB 1.99 billion, up 27% year-on-year. The company also declared a cash dividend of HKD 0.18 per share, a 20% increase from the previous year, reflecting its continued adherence to mainstream shareholder return practices among domestic and international OTAs, and highlighting its long-term profit potential.

Battlegrounds That Don’t Determine Victory: Internationalization, AI, and Vacation Business

This quarter, Tongcheng’s internationalization showed a split pattern. According to the announcement, outbound ticketing accounted for over 5% of transportation ticket revenue. Compared to Q3, we believe there was no significant breakthrough in overall globalization.

Looking at individual product lines, international air ticket volume in Q4 increased by over 130% year-on-year, while the total room nights of international accommodation grew over 110% for the full year. In Q3, air ticket growth was 110% and accommodation 130%, indicating a relative slowdown in accommodation, with air tickets becoming the core driver of internationalization. Growth was mainly concentrated in destinations such as Japan, South Korea, Malaysia, and Singapore.

In terms of AI development, Tongcheng launched its self-developed generative AI, "Chengxin." This tool offers hotel comparison functions, and testing shows that its positioning is more aligned with Ctrip’s TripGen, providing comprehensive content recommendations, rather than Booking’s AI Agent, which focuses solely on hotel guidance. However, the accuracy of overseas content still requires improvement. We believe that features mentioned by Tongcheng—such as digital tour guides, voice interaction, and personalized recommendations—should be technically achievable in the near future. Nevertheless, globally speaking, AI still needs time to become a major traffic entry point.

As for the vacation business, Tongcheng has successfully crossed the breakeven point, achieving full-year revenue of RMB 3.14 billion, accounting for about 18% of the group’s total revenue. However, its profit margin was only 2.3%, indicating a limited contribution to overall profit.

Overall, from both a profitability and operational growth standpoint, internationalization, AI, and vacation services are currently not decisive factors.

The Code to Tongcheng’s Profitability

If the above segments are not the key, then what is driving Tongcheng’s expanding profitability? Haize Capital believes two core data points offer insight:

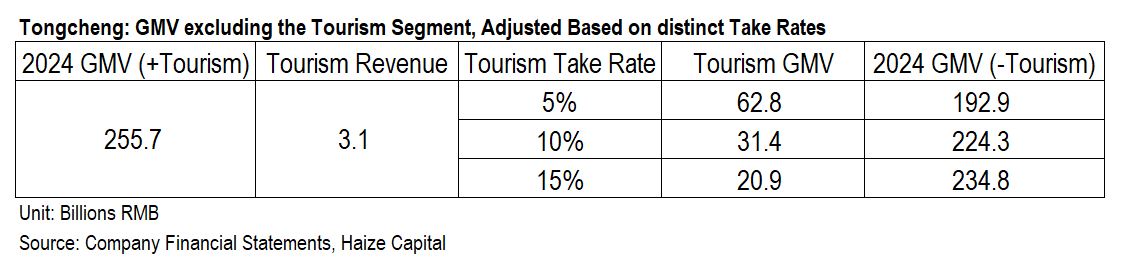

1. Rapid Growth in Commission Revenue –

In 2023, the vacation segment was not yet included in Tongcheng’s financial statements. If we exclude its impact and assume a 10% commission rate for the vacation business, then the 2024 GMV of the core online travel platform would be approximately RMB 224.3 billion—lower than RMB 238.8 billion in 2023.

However, even with a lower GMV, the core platform revenue still increased by 22% year-on-year to RMB 14.2 billion in 2024. Both transportation ticketing and hotel bookings grew by 20%, while other revenues (including hotel management services) rose by 35%, showing a strong conversion from GMV to revenue.

Based on comparative indicators, we believe the growth in revenue and profit was primarily driven by enhanced bargaining and monetization capabilities with downstream suppliers (e.g., hotels), rather than simply from user or order volume growth.

2. Self-Owned Traffic and Cost Control –

Tongcheng’s proprietary app saw a year-on-year doubling of its daily active users (DAU). Although mini program DAU figures were not disclosed, the surge in app DAU clearly reduced dependency on paid customer acquisition, making marketing costs more manageable.

This is evident in Q4, where revenue grew 35% year-on-year while marketing expenses rose only 14%, and R&D expenses even slightly declined. We believe that if the vacation business were excluded, the cost ratio would show even greater flexibility and advantage.

The Root of Sustainable Growth

From 2023 to 2024, Tongcheng’s annual paying users increased only slightly from 235 million to approximately 238 million—a mere 1.5% increase. However, core platform revenue rose by 22%, and operating profit increased by 29%.

This suggests that a stable user base, with slightly higher consumption frequency (8.1 times per user in 2024 vs. 7.5 in 2023), can still generate substantial revenue and profits.

We believe this phenomenon reflects a structural reality in the Chinese travel market: an oversupply on the supplier side, giving platforms significant bargaining power and resulting in platform dividends.

This trend benefits not only Tongcheng, but also peers like Ctrip and Meituan. Although Chinese OTAs have lower commission rates compared to Western giants, their profitability is significantly amplified through monetization mechanisms such as paid ranking and ad exposure—especially in the accommodation sector.

In the transportation segment, although front-end commissions are low or even zero, users who enter through the app and purchase bundled ancillary services (BAF) generate significant profit, particularly in cancellation and rescheduling services. These have become one of the most critical profit drivers for Tongcheng and other OTAs in the Zhongzhong ecosystem.

Conclusion

Even though Tongcheng’s international expansion remains slow, AI has yet to become a major traffic driver, and its vacation business contributes little to profit, its profitability remains sustainable—as long as the current air ticket and hotel ecosystem holds, and the supply-demand structure remains unchanged. There is even potential for further margin expansion.