登錄

選單

登錄

海擇短評 Haize Comment:

盛放於微縮花園:從HanaTour看韓國組團市場的集中進化

在後疫情全球旅遊浪潮復甦之際,從韓國看,組團旅遊佔比雖然變低了,但是主要組團社不僅沒有消失,反而成為在越來越小的花園中,越來越大的花朵。

重啟的節奏

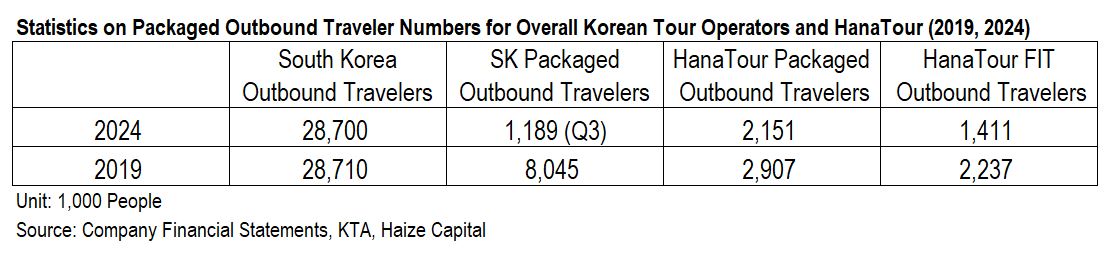

疫情後,亞洲旅遊市場的重啟步調顯得分裂且多元。韓國作為一個高度仰賴出境需求的旅遊大國,在2024年迎來幾乎與2019年持平的出境總人次,達到2,870萬人,對照疫情前的2,871萬,幾乎可視為全面復甦。

花園變小之後

但若從出境團隊旅遊的角度觀察,那就是另一番風景。根據韓國官方觀光統計(한국관광통계),2019年出境團隊旅遊人次達804.5萬,佔整體出境人次的28.0%;而到了2024年第三季,出境團隊旅遊僅118.9萬人次,佔同期總出境人次717.4萬的比重,下降至16.6%。短短五年內,團隊旅遊的市場佔比下滑了近12個百分點,儘管全年數據尚未公布,但趨勢已極為明確。

在更小的花園中更大的花

然而,在這樣”花園變小”的環境中,韓國組團社巨頭卻沒有跟著縮水,反而展現出逆勢成長的集中效應。2019年,HanaTour(KRX: 039130)共服務了290.7萬出境團隊旅客,佔全韓整體團隊旅客人次的36%;而到了2024年第三季,其服務人次雖回落至49.5萬,但在更為萎縮的市場中,市佔率反而上升至41.6%。換言之,它在一個萎縮的花園中,成為一朵更大的花。

更強大的訂價權

這樣的集中也反映在交易額上。雖然HanaTour全年出境團體旅遊人次在2024年降至215萬,較2019年下滑約26%,但交易額卻從2.17兆韓元(14.8億美元)上升至2.23兆韓元(約15.2億美元),實現逆勢增長。這背後除了反映全球通膨帶動目的地資源漲價,也與市場集中帶來的訂價能力提升息息相關。換句話說,HanaTour不只是活了下來,還更能定價、也更能賺錢,同業環境降價取單的氛圍較疫情前大幅收斂。

不是每一座花園都一樣小

當然,這樣的現象能否放諸四海皆準,仍需謹慎觀察。海擇資本認為,即便僅限泛東亞地區的日本、韓國及台灣,不同市場間的差異仍十分明顯。組團旅遊在總市場中的佔比縮小、大者恆大的結構趨勢確實存在,但集中度的幅度並不一致。

這其中的關鍵可能在於旅行社對FIT(Free Independent Traveler)產品的銷售與運營能力。以2024年第三季為例,韓國旅行社共服務250.2萬出境人次,其中123.3萬人(約49.3%)屬於FIT旅客,HanaTour在同期服務88.4萬出境人次,其中有38.9萬(約44.0%)屬於FIT旅客;反觀台灣,組團社對自由行市場的參與度普遍偏低,佔比普遍在5%以下,這種差距亦可從各組團社自營APP的月活躍(MAU)數中清晰看出。

成為小眾卻無可取代的花

組團旅行是否會因自由行的普及而走向消亡?我們的判斷是否定的。在高端、低價與家庭團體三個維度上,組團旅遊仍然具有不可取代的結構性價值。未來真正具備規模經濟、能夠跨越團與非團邊界的旅行品牌,反而更有機會像HanaTour一樣,在這片越來越小的花園中,綻放出越來越大的花。

----

Blooming in a Shrinking Garden: HanaTour and the Consolidation of Korea’s Group Travel Market

As global travel recovers in the post-pandemic era, a closer look at Korea reveals an interesting contradiction: while the share of group travel has declined, leading tour operators have not only survived but flourished—becoming ever-larger flowers in an ever-shrinking garden.

The Rhythm of Reopening

Following COVID-19, the pace of recovery in Asia’s travel market has been fragmented and varied. Korea, a country heavily reliant on outbound tourism, reached 28.7 million outbound trips in 2024—virtually identical to its pre-pandemic 2019 figure of 28.71 million. In terms of overall demand, full recovery has essentially been achieved.

When the Garden Shrinks

However, the story looks quite different when we focus specifically on group travel. According to official Korean tourism statistics (한국관광통계), 8.045 million outbound group travelers were recorded in 2019, accounting for 28.0% of total outbound travelers. By Q3 2024, that number had shrunk to just 1.189 million, representing only 16.6% of the 7.174 million outbound travelers during the same period. In just five years, group travel’s share has dropped by nearly 12 percentage points. Though full-year data is not yet available, the trend is already clear.

A Bigger Flower in a Smaller Garden

Despite this contraction, Korea’s leading group travel operator has not diminished. On the contrary, it has become even more dominant. In 2019, HanaTour (KRX: 039130) served 2.907 million outbound group travelers, representing 36% of Korea’s group travel market. By Q3 2024, its group travel volume had dropped to 495,000, but its market share rose to 41.6% due to the overall decline in the category. In other words, HanaTour has become a larger flower in a much smaller garden.

Stronger Pricing Power

This consolidation is even more evident in transaction volume. While HanaTour’s total annual outbound group travelers fell to 2.15 million in 2024—down roughly 26% from 2019—its total transaction volume grew from KRW 2.17 trillion (USD 1.48 billion) in 2019 to KRW 2.23 trillion (USD 1.52 billion) in 2024. This counter-cyclical growth reflects both global inflation (raising the cost of destination resources) and HanaTour’s strengthened pricing power due to increased market concentration. In short, HanaTour not only survived but is now in a stronger position to set prices and drive profitability. The industry’s pre-pandemic practice of discount-driven competition has also significantly diminished.

Not Every Garden Shrinks the Same Way

Still, this phenomenon should not be assumed to apply universally. Haize Capital believes there are important differences even within the East Asian region. While the overall trend of declining group travel share and increased consolidation holds true, the degree of concentration varies by market. A key variable may lie in each market’s ability to sell and manage FIT (Free Independent Traveler) products. For example, in Q3 2024, Korean travel agencies served a total of 2.502 million outbound travelers, with 1.233 million (approximately 49.3%) classified as FIT. HanaTour alone served 884,000 outbound travelers during the same period, of whom 389,000 (approximately 44.0%) were FIT. In contrast, Taiwanese tour operators have significantly lower FIT penetration, often below 5%, as reflected in their self-operated apps' monthly active users (MAUs).

A Niche Flower That Won’t Wither

Will group tours disappear in the age of FIT dominance? We don’t think so. In three key segments—high-end travel, ultra-budget travel, and family groups—group travel remains structurally indispensable. The future belongs to travel brands with economies of scale and the ability to straddle the line between group and independent travel. Like HanaTour, they may continue to bloom, becoming ever-larger flowers in an increasingly compact but fertile garden.