登錄

選單

登錄

海擇短評 Haize Comment:

滴滴的盈虧之謎:中國的網約車平台之王為何無法盈利?

滴滴近日發佈了2024年第四季度財報,呈現出一幅耐人尋味的財務畫面:單季交易量高達42.66億筆,合併報表收入達到529億元人民幣,但淨虧損仍達13億元。作為中國網約車領域的領軍企業,滴滴的財報提出了一個關鍵問題——這家公司是真的不具備盈利能力,抑或只是尚未找到盈利的節奏?

同時間,滴滴的全球對手Uber(NYSE: UBER)卻實現了顯著盈利,進一步突顯了雙方之間的差距。本文將透過解構財報數據,並延伸觀察聚合打車模式的發展機會,嘗試為這場網約車新博弈找出未來的轉捩點。

如果Uber是典範,滴滴還差了什麼?

是賽道的問題還是車手的問題?一季超過40億次的交易量(用車訂單數),還不能盈利?但從滴滴的全球同業Uber(NYSE: UBER)來看,就是另一番風景。

從交易量來看,滴滴在規模上明顯占優:Q4總訂單數42.6億筆,遠高於Uber的30.7億筆,即使僅計中國境內(32.5億筆)也已超越Uber全球資料。然而,在收入與盈利表現上,兩者卻出現了明顯反差。

Uber第四季總交易額(GTV, Gross Transaction Value)為442億美元,約合3,210億元人民幣,是滴滴的1,032億元人民幣的三倍有餘。佣金率方面,Uber達到27.0%,而滴滴僅為18.5%。在這兩項差異驅動下,Uber取得119.6億美元(約869億元人民幣)的收入,是滴滴平台收入的3.5倍。

即便將滴滴合併報表中包含“核心平台(Core Platform)”以外業務納入比較,其Q4總收入529億元人民幣,仍僅達Uber對應收入的64%。換言之,Uber以較少的訂單數量,創造出更多的營收,背後所反映的,不只是單價與佣金結構的不同,更揭示了兩家公司在業務模型上的本質差異。

盈利關鍵:客單價、佣金率與司機激勵的再平衡

造成滴滴與Uber獲利能力差異的主因,歸根結底在於三個層面:

1. 客單價:中國用戶平均付費較低,客單價遠不及歐美市場;

2. 佣金率:滴滴為平衡司機收入與政策壓力,Take Rate明顯偏低;

3. 司機補貼:平台對司機仍需一定激勵,進一步壓縮平台利潤空間。

而這三者的改善空間,將決定滴滴能否從一家高交易量公司,轉化為高價值平台。

短期有盈虧之憂,長期藏轉型之機

海擇資本認為,儘管仍處虧損狀態,滴滴的營運效率已逐步展現。根據財報,滴滴在運營支持(Operations and Support)、行銷(Sales and marketing)與研發(Research and development)方面的費用率,分別僅為收入的4.0%、6.1%與4.0%,顯著低於Uber與Grab(NASDAQ: GRAB)等國際同業。

這顯示出一個新趨勢:當前網約車技術已趨於成熟、資本市場氛圍已不鼓勵激進補貼,既不像過去必須有大額技術投入,也跳脫了行銷補貼的價格戰怪圈。

在此背景下,我們認為滴滴的機會可從三個時間維度切入:

· 當下:費用率控制得宜,具備良好運營效率;

· 短期:海外市場佣金率仍低於市場平均,有調升空間-相較於東南亞Grab在隨選服務的佣金率達15.0%,滴滴海外的佣金率僅9.6%,確實偏低,更別說與Uber(27.0%)相比;

· 長期:中國本土客單價與佣金率若能微幅提升,盈利能力將迅速改善-現在的疑慮是中國的訂單均價能提升到什麼規模(客單價議題),以及在政策面與行業競爭面是否能允許本地生活服務商漲價(佣金率議題)。

聚合打車:新的衍生賽道與機會

在關注滴滴能否模仿Uber之外,我們可以關注另一個正在全球興起的趨勢:整合”多平台”與”多運力”的聚合打車平台。

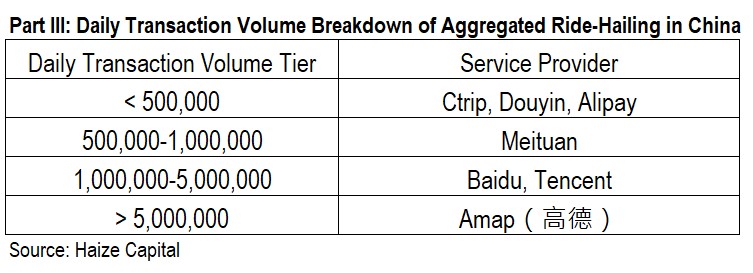

中國的聚合打車已經很成熟,日交易量最大有在500至1,000萬單區間的服務商(見附圖),主要流量入口如高德(地圖)、騰訊(社交)、百度、美團(生活服務)、支付寶(電商)、哈囉(出行)、攜程(旅遊)、抖音(短視頻)…,都建立了聚合打車平台,強調低佣金、多運力、多平台。這些平台本身不自營車隊,而是整合多家運力與服務商,建立覆蓋更廣的叫車生態。

這股趨勢也逐漸向海外擴散,亞洲各區也開始了”類聚合”的演化:

· 中國供應商(比如悅行”Heycars”)將聚合平台帶到東南亞、東北亞。

· 印度的Namma Yatri采開源協議、0佣金政策,結合政府與社群力量,聚合當地計程車司機與三輪車;

· Grab自印尼與越南開始推出Aggregator模式,讓協力廠商計程車及私家車平台/車隊接入;

· 日本的MOV(DeNA)與S.RIDE(Sony)聚合多家計程車公司運力,但不自營車隊,也不干預車價與派單。。

整體來看,未來如同中國走向更完整聚合用車服務也不奇怪。

滴滴作為中國交易量最大的出行平台,其收入結構與盈利能力尚有優化空間;但從費用控制、未來增長動能看,其在境內外與新型聚合平台的競爭與合流,是值得持續觀察的市場格局。

-----

Haize Capital Insights of the Day

The Profitability Puzzle of Didi: Why China’s Ride-Hailing King Still Struggles to Turn a Profit

Didi recently released its financial results for Q4 2024, revealing a set of figures that invite closer scrutiny. Despite recording a massive 4.27 billion trips in the quarter and a consolidated revenue of RMB 52.9 billion, the company still posted a net loss of RMB 1.3 billion. As the leading ride-hailing platform in China, Didi’s report raises a key question for investors: Is the company fundamentally unprofitable, or has it simply not yet found its path to profitability?

Meanwhile, Didi’s global peer Uber (NYSE: UBER) reported solid profits during the same period, underscoring the gap between the two giants. This article will unpack the financial data and explore the emerging opportunities in the “aggregated ride-hailing” model, in an effort to identify where the next inflection point in the industry may lie.

If Uber Is the Benchmark, What’s Didi Still Missing?

Is the problem the track—or the driver? With over 4 billion orders in a single quarter, how is it still unprofitable? Didi’s numbers stand in sharp contrast to Uber’s.

In Q4, Uber completed 3.07 billion trips globally—significantly fewer than Didi’s 4.27 billion. Even Didi’s domestic trips in China (3.25 billion) exceeded Uber’s global total. However, when it comes to revenue and profitability, the tables are turned.

Uber reported a Gross Transaction Value (GTV) of USD 44.2 billion (~RMB 321 billion) in Q4, more than triple Didi’s RMB 103.2 billion. Its average take rate reached 27.0%, compared to Didi’s 18.5%. This allowed Uber to generate USD 11.96 billion (RMB ~86.9 billion) in revenue—3.5x higher than Didi’s platform revenue of RMB 19.1 billion.

Even when considering Didi’s total consolidated revenue of RMB 52.9 billion (including businesses beyond the Core Platform), the figure is only about 64% of Uber’s. In essence, Uber is generating significantly more revenue with fewer trips. The difference lies not only in pricing and commission structures, but also in the fundamental design of each company’s business model.

The Path to Profit: Balancing Fare per Trip, Take Rates, and Driver Incentives

Didi’s profitability gap relative to Uber can be attributed to three key factors:

· Fare per Trip: Chinese users pay significantly less on average than users in Western markets.

· Commission Rate (Take Rate): Didi maintains a relatively low take rate to balance driver earnings and regulatory pressure.

· Driver Incentives: The platform still offers substantial subsidies to drivers, further squeezing margins.

Improving performance in these three areas will be crucial for Didi to evolve from a high-volume platform into a high-revenue, high-profit one.

Near-Term Losses, Long-Term Opportunities

Despite the current losses, Didi’s operating efficiency is beginning to shine through. According to its financial report, the company’s cost ratios for operations and support, sales and marketing, and R&D stood at just 4.0%, 6.1%, and 4.0% of revenue, respectively—significantly lower than international peers like Uber and Grab (NASDAQ: GRAB).

This reflects a broader industry trend: ride-hailing technology has matured, and capital markets are no longer rewarding aggressive subsidy strategies. Massive R&D spending and marketing-driven price wars are no longer required to survive or grow.

Against this backdrop, we believe Didi has strategic opportunities across three timeframes:

Immediate term: Strong cost control and operational efficiency;

· Short term: Overseas commission rates are below industry averages and could be raised. For reference, Grab's on-demand services achieve a take rate of ~15.0%, while Didi’s overseas rate stands at just 9.6%—significantly lower than Uber’s 27.0%;

· Long term: Even marginal increases in average fare and commission rates in China could significantly boost profits. Key concerns include whether average fares can sustainably rise, and whether regulatory and competitive conditions will permit meaningful price adjustments.

Aggregated Ride-Hailing: An Emerging Vertical with Global Momentum

Beyond Didi’s profitability challenge, another industry trend deserves attention: the rise of aggregated ride-hailing platforms, which integrate multiple operators and fleets under a single interface.

China’s aggregator ecosystem is already highly developed. Several platforms report daily transaction volumes ranging from 5 to 10 million orders, with major consumer gateways such as Amap (Gaode Map), Tencent (WeChat), Baidu, Meituan, Alipay, Hello, Ctrip, and Douyin all offering ride-hailing access. These platforms typically don’t operate fleets themselves. Instead, they aggregate third-party service providers, creating broader and more flexible ride-hailing networks with low commissions, multiple supply sources, and cross-platform coverage.

This trend is now spreading beyond China, with regional adaptations emerging across Asia:

· Chinese suppliers (e.g., Heycars) are exporting the aggregator model to Southeast and Northeast Asia;

· Namma Yatri in India is an open-source, 0% commission platform backed by local governments and communities, aggregating local taxi and auto-rickshaw drivers;

· Grab has launched its “Aggregator” service in Indonesia and Vietnam, allowing third-party taxi and fleet operators to integrate;

· In Japan, MOV (DeNA) and S.RIDE (Sony) aggregate multiple taxi companies without controlling pricing or dispatching.

Looking ahead, the emergence of full-featured ride-hailing aggregators—mirroring China’s model—is not only possible, but increasingly probable in many global markets.

Final Thoughts

As the dominant ride-hailing platform in China by transaction volume, Didi still has work to do in optimizing its revenue structure and improving profitability. However, its tight cost control and lean operations provide a solid foundation.

Its future performance—whether as a rival to Uber or as a collaborator or participant in the broader aggregator ecosystem—will depend on how effectively it adapts to evolving customer expectations, regulatory environments, and platform governance models.

The story of Didi is no longer just about scale. It’s about adaptability, business model innovation, and the search for sustainable value in a post-subsidy era of ride-hailing.