登錄

選單

登錄

海擇短評 Haize Comment:

美團公告了2021Q2財報,我們從酒店行業切入簡要談談下我們的部分觀點:

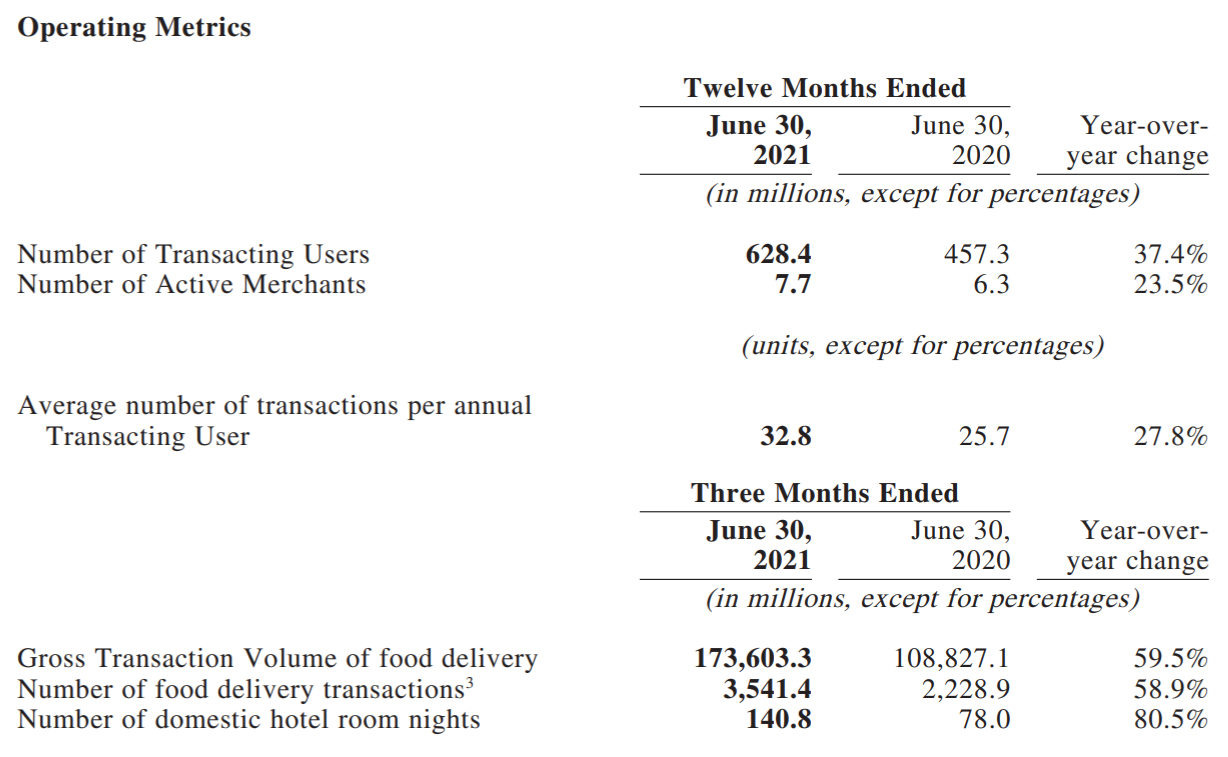

1. Q2到店、酒店與旅遊的收入是86.0億人民幣(以下同),較2019年同期52.5億增長64%。雖然到店、酒店與旅遊的收入打包在一起公告,我們無從得知酒店的現況,但可以推估酒店收入增速沒有理由不好。

2. Q2國內酒店間夜量達1.41億間夜,相對2019年同期增長50%,增速應該是全球OTA巨頭中最高。從絕對值來看,Q2全球間夜量最高是Booking的1.57億間夜,美團約為Booking的90%,再次證明了疫情間中國單一市場的魅力。

3. 美團Q2間夜增速對2019年同期增長很高,投資人會更關心接下來攜程財報是否能反應相同趨勢。

4. 王興在電話會議談了共同富裕,我們理解這是對政府監管趨勢的回應。現況下公司應該會從"兼顧盈利"回歸"重市場份額"的模式,特別在創新業務層面,這對其在各領域的競爭者來說不算是好事。

----------

메이투안(美团)은 2021년 2분기의 재무보고서를 발표했는데, 우리는 호텔업계부터 우리의 일부 관점을 간단히 이야기하고자 한다.

1. 2분기의 고객 유치, 호텔 숙박, 여행 예약의 수입은 86.0억 위안으로 2019년 같은 기간 52.5억 위안에 비해 64% 증가했다. 비록 고객 유치, 호텔 숙박, 여행 예약의 수입과 함께 종합적으로 발표하였기 때문에 우리는 현재 상황을 정확하게 알 수 없다. 하지만 호텔 수입 증가가 나쁜지 않다고 추정할 수 있다.

2. 2분기 국내 호텔의 룸나잇은 1.41억 개로 2019년 동기 대비 50% 성장했으며, 성장 속도는 전 세계 OTA 거두 중 최고일 것이다. 절대치로 볼 때, 2분기의 전 세계의 룸나잇의 수량은 Booking이 1억 5700만 개로 가장 많았다. 메이투안은 Booking의 약 90%를 차지해, 중국 단일 시장의 매력을 다시 한번 입증했다.

3. 메이투안 2분기의 룸나잇의 성장속도가 2019년 동기 대비 매우 높아 투자자들은 씨트립(Ctrip.com)의 재무보고서도 같은 추세를 반영할 수 있을지 더욱 관심을 가질 것이다.

4. 왕싱(王興)은 전화회의에서 ‘공동부유’를 이야기했는데 우리는 이는 정부의 감독관리 추세에 대한 반응이라고 이해한다. 현재 상황하에서 회사는 '수익성을 겸해'에서 '시장 점유율에 중점을 둔' 모델로 회귀할 것으로 보인다, 특히 혁신 업무 측면에서, 이것은 각 분야의 경쟁자들에게 좋은 일이 아니다.

----------

美団(Meituan)は、2021年第2四半期の決算を発表した。宿泊業界を切り口にして、私たちのいくつかの観点を簡単に説明する。

1、第2四半期の店舗集客・宿泊・旅行予約の収入は86.0億人民元で、2019年同期の52.5億人民元に比べて64%増加した。店舗集客とホテル、旅行予約の収入をまとめて発表したので、宿泊事業の現状はわからなかった。しかし、宿泊業務の収入増が悪いわけではないと推測できる。

2、第2四半期の国内ホテルの泊数は1億4100万泊で、2019年同期比50%増と、世界のOTA大手の中で最も高い伸び率となった。絶対値で見ると、第2四半期に全世界の宿泊数が最も多かったのは、bookingの1億5700万泊だった。美団の宿泊数はbookingの約90%に相当した。新型コロナ期間の中国単一市場の魅力が再確認された。

3、美団の第2四半期の宿泊数の伸び率は2019年同期より高くなった。投資家たちは、次のCTRIPの決算が同じトレンドを反映するかどうかにより多くの関心を持っている。

4、王興CEOは電話会議で「共同富裕」について話した。これは、政府の規制トレンドに対する美団の反応だと考えている。現在の状況では、美団は「利益との兼ね合い」から「市場シェア重視」のモデルに回帰するはずで、特にイノベーション業務のレベルでは、各分野の競合他社にとっては良いことではない。

----------

Meituan announced its 2021Q2 earnings report. We'd like to start with the hotel industry and briefly share some of our views:

1. The revenue of in-store, hotel&travel in Q2 reached RMB 8.60 billion yuan(the same below), an increase of 64% from 5.25 billion in the same period in 2019. Although the revenue of in-sore and hotel&travel were packaged to announce and we don't know its current status of hotel, we have no reason to doubt Meituan achieved good growth rate of hotel revenue.

2. The number of domestic hotel room nights in Q2 amounted to 141 million, an increase of 50% compared to the same period in 2019, this growth rate should be the highest among global OTA giants. In terms of absolute number of room nights, the world top1 in Q2 is Booking with 157 million, the number of room nights of Meituan is about 90% of Booking’s, which once again proves the charm of China as a single market during the pandemic.

3. Compared to the same period in 2019, Meituan reached a high growth rate of room nights in Q2. Now investors would be more concerned about whether the following earning report of Trip.com could reflect the same trend.

4. Wang Xing mentioned common prosperity in its conference call. We believe this is a response to the trend of government regulation. Under the current situation, the company should return to the model of "focusing on market share" from "considering profit", especially at the level of innovative business, which is not a favor for its competitors in various fields.

資料來源 Resource:Meituan

標籤 Label:Meituan 3690 Booking BKNG OTA Chinese market COVID-19 food delivery