登錄

選單

登錄

海擇短評 Haize Comment:

Booking(NASDAQ: BKNG)近期公告2021Q4財報。Booking的Q4運營成果不錯,Q1預期也偏樂觀,不過在俄烏戰事對業績衝擊回答得偏無力。在對Airbnb的競爭上,Booking仍將持續通過投資與一站式服務服務尋求增長的路。我們摘錄海擇資本部分研究重點如下:

Booking與Airbnb在歐美的競爭,從財務看,本質是當Airbnb的間夜數成長一倍到了Booking的規模,以Airbnb的商業模式與模型,盈利是否可能更有效率,從這點看,我們的答案是Yes。不過現在雙方已經不盡然能完全對標,Airbnb選擇的是SKU總數相對少、庫存獨佔、高毛利的市場,而Booking反之,只要投放的ROI能賺錢的都做,估計也不介意Airbnb通過channel manager拿Booking的房賣,這樣的策略能最大化市場份額。2022Q1 Airbnb就算收入增長70%到14億美金,Booking的酒店本業收入可能仍然還有28億美金,加計廣告等其他收益還超過33億。當然Airbnb的強項是不斷擴充邊界,最後的結果是,雙方激烈衝突,然後位於後位的同業如果不轉型,都會被邊緣化。

----------

Booking(NASDAQ: BKNG)은 2021년 4분기 재무제표를 최근 발표했다. 2021년 4분기 경영 실적이 괜찮고, 2022년 1분기 실적 전망도 낙관적이다. 그러나 우크라이나 정세가 실적에 미치는 영향에 대해 Booking의 답변은 설득력이 약했다. Airbnb의 경쟁에 맞서 Booking은 투자와 원스톱 서비스를 통해 끊임없이 성장을 모색해 왔다. Haize Capital의 분석 결과를 요약하면 다음과 같다.

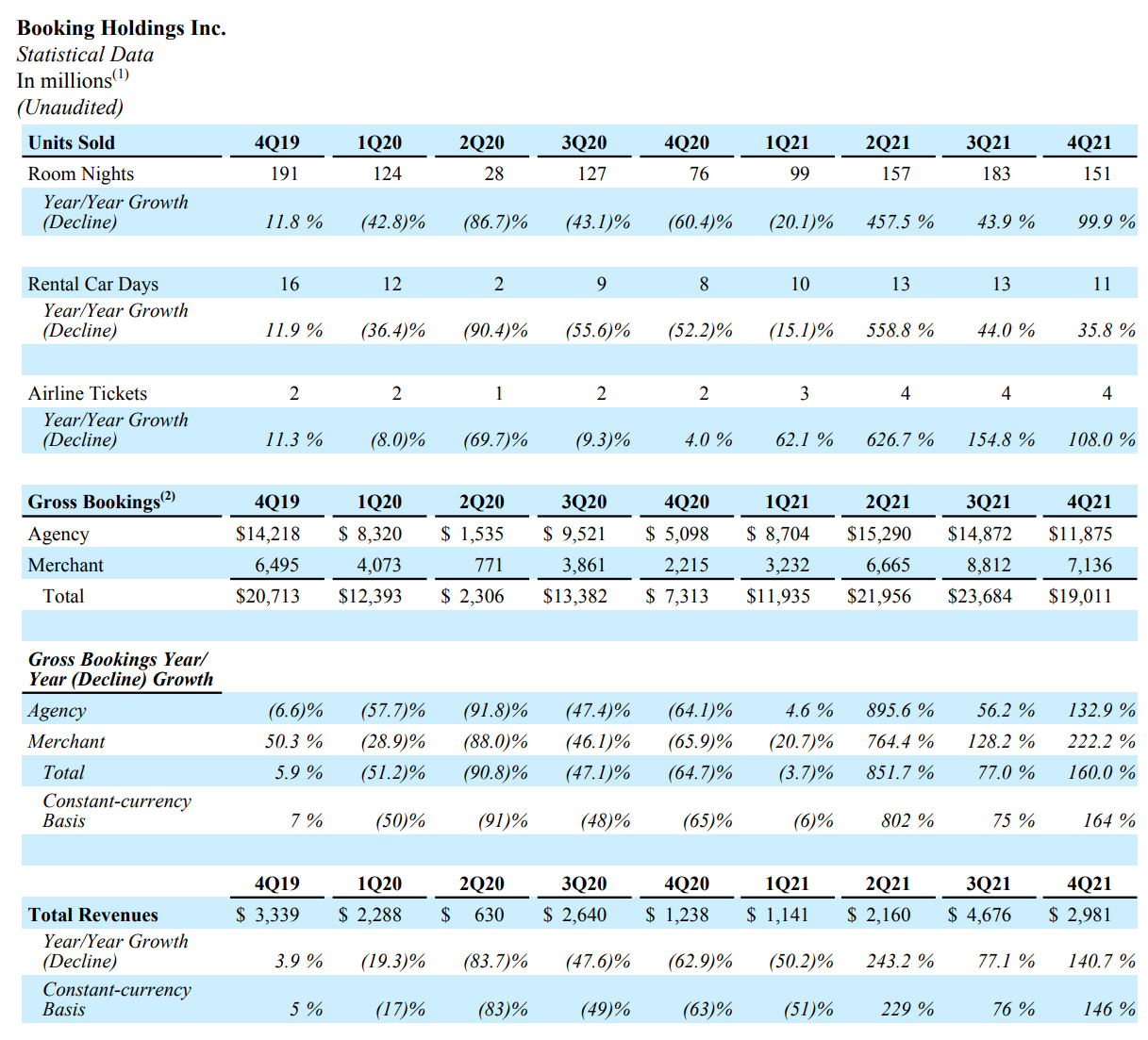

1. 2021년 4분기 실적은 다음과 같다. Booking의 4분기 숙박 매출 객실 수는 1억 5000만 개로 2019년 동기 대비 79% 수준이었다. EBITDA는 9억 4000만달러로 2019년 같은 기간의 73%였다.

2. 2022년 1분기에 대한 실적 전망은 다음과 같다. Booking은 2022년 1분기 전체 실적 전망은 공식적으로 발표하지 않았고, 콘퍼런스 콜에서 일부 수치만 설명했다. 2022년 1분기 숙박 매출 객실수는 2019년 동기보다 1015% 줄어들 전망이다. 또 서유럽 시장은 2022년 2분기 거래액이 2019년 동기 대비 2배 이상 성장할 것으로 예상된다. 2019년 서유럽이 Booking의 주요 판매시장임을 감안하면 매우 낙관적인 전망이라고 할 수 있다.

3. 동업자간의 경쟁에 대한 전망은 다음과 같다. Airbnb이 공개한 실적예기에 따르면 2022년 1분기 수입이 2019년 동기 대비 70% 정도 성장하게 된다. Booking의 2019년 실적 절대치가 큰 것을 감안하면 2022년 1분기에도 여러 지표에서 약 Airbnb의 2배가 될 것으로 예상된다. 이 때문에 두 회사의 격차는 눈에 띄게 줄어들지 않고 있다. 세계 1, 2위 OTA로 꼽히는 Booking과 Airbnb를 합한 숙박 매출 객실수 증가는 양사의 경쟁으로 다른 경쟁사의 시장 점유율이 더 줄어들 수 있음을 의미한다.

4. 원스톱 서비스의 진행 상황은 아래와 같다. Booking이 그동안 거론했던 'Connected Trip'사업 초점은 행사 체험과 렌터카에서 항공권 판매로 바꿨다. 항공권 판매 업무는 현재 34개 국가를 망라하고 있으며 업무량은 2019년 대비 104% 성장했다. 비록 새로운 업무에 대해 말하자면 이 성적은 불합격이긴 하지만, 코로나19가 숙박산업보다 항공산업에 미치는 영향이 크다는 점을 감안하면 2022년은 Booking의 항공권 판매 사업을 살펴보는 중요한 시기가 될 것이다.

5. 우크라이나 정세가 회사 실적에 미치는 영향은 다음과 같다. 전쟁은 관광산업의 천적이다. 최근 투자자들이 촉각을 곤두세우고 있는 우크라이나 정세에 대해 Booking은 '러시아와 우크라이나의 여행목적지 시장에서이 지역 교역액이 전체에서 차지하는 낮은 비중에 불과하다(If we look at Russia and Ukraine combined as destination markets, they represent a very low single-digit percentage of our total gross bookings). 게다가 2022년 한 해 동안 어떤 일이 일어날지 예측하기 매우 어렵다'고 말했다. 그런 대답은 만족스럽지 않지만 Glenn Fogel은 영매자나 예언자가 아니라 CEO뿐이다.

유럽과 미국 시장에서 Booking과 Airbnb의 경쟁은 본질적으로 Airbnb의 매출 객실 수가 두 배로 증가하여 Booking과 같은 규모가 되었을 때, Airbnb의 비즈니스 모델이 Booking보다 더 높은 이윤률을 창출할 수 있는가에 달려 있다. 우리는 Airbnb이 해낼 수 있을 거라고 믿는다. 하지만 아직 두 회사가 서로의 참고 기준이 될 만한 수준은 아니다. Airbnb은 SKU수량이 상대적으로 적고, 주택 재고를 독점하고, 총이익률이 높은 시장을 선택했다. Booking은 반대로 이익이 나면 사업을 할 것이다. Airbnb이 Booking 재고를 channel manager를 통해 판매해도 Booking은 개의치 않을 수 있다. 시장 점유율을 극대화할 수 있기 때문이다. Airbnb의 2022년 1분기 매출이 14억 달러로 70% 성장하더라도 Booking의 주력 사업인 숙박사업 매출은 28억 달러, 광고 등 기타 수익을 합치면 33억 달러를 넘을 것으로 예상된다. 물론 Airbnb의 강점은 사업 범위를 계속 확장하는 것이다. 결국은 두 회사 간의 경쟁은 더욱 치열해져 다른 회사들은 변신을 하지 않으면 도태될 것이다.

----------

Booking(NASDAQ: BKNG)はこのほど、2021年第4四半期決算を発表した。2021Q4の営業成績が良好で、2022Q1の業績予想についても楽観的だった。ただし、ウクライナ情勢による業績への影響について、Bookingの回答は説得力が弱かった。Airbnbの競争に対して、Bookingは投資とワンストップサービスで成長の道を模索し続ける。私たちは海擇資本の研究の重点を一部抜粋すると次のようになる。

1、2021年第4四半期の業績成果。Q4におけるBookingの販売泊数は1億5000万泊で、2019年同期の79%となった。EBITDAは9億4000万ドルで、2019年同期の73%となった。

2、2022年第1四半期の業績予想。同社は2022Q1全体の業績予想を正式に開示しておらず、電話会議で一部のデータを説明するにとどまっている。2022Q1の販売泊数は2019年同期より10 ~ 15%低い可能性がある。また、2022Q2の取引額ついては、2019年同期を上回って、うち西ヨーロッパ市場が倍以上に伸びる見込みである。2019年は西ヨーロッパがBookingの主な販売市場であったことを考えれば、これは非常に楽観的な見通しだ。

3、同業他社との競争。Airbnbが開示した業績予想によると、2022Q1の収入は2019年同期比70%程度増加する。Bookingの2019年の業績の絶対値が非常に大きいことを考慮すると、2022Q1に複数の指標では依然としてAirbnbの約2倍になると推定される。そのため、両社の差は明らかに縮まっていない。世界トップ2と言われるOTAであるブーキングとAirbnbの合計販売泊数の増加は、両社の競争により、他の同業他社の市場シェアが今後低下することを意味している。

4、ワンストップサービスの進展状況。Bookingがこれまで言及していた「Connected Trip」事業は現在、アクティビティ・体験やレンタカーから航空券販売へ焦点が変わっている。航空券事業は現在34カ国をカバーしており、業務量は2019年比104%増加した。新規事業としては不合格の成績だが、コロナ禍による航空産業への影響が宿泊産業への影響よりも大きいことを考えると、2022年がBookingの航空券事業を観察する大切な時期となる。

5、ウクライナ情勢。戦争は観光産業の天敵だ。最近、投資家の関心が高まっているウクライナ情勢について、Bookingは「ロシアとウクライナの目的地市場として見ると、その地域の取引額が全体に占める割合が一桁(If we look at Russia and Ukraine combined as destination markets,they represent a very low single-digit percentage of our total gross bookings)であり、 2022年がどうなるか予測しにくい。そのような答えはあまり満足のいくものではないかもしれないが、Glenn FogelはCEOであり、霊媒師や預言者ではない。

欧米市場でのBookingとAirbnbの戦いは、本質的には、Airbnbの販売泊数が2倍に成長してBookingと同等の規模になるときに、AirbnbのビジネスモデルでBookingよりも高い利益率を出せるかどうかにかかっている。私たちはAirbnbならできると信じている。ただし、現時点では両社はお互いに完全にベンチマークすることができない。Airbnbは、SKU数が比較的少なく、物件在庫が独占的で、粗利益率が高い市場を選択している。Bookingはその逆で、利益を生み出すことができればその事業を行う。Airbnbがchannel managerでBookingの在庫を販売しても、Bookingが気にしていないかもしれない。このような戦略が市場シェアを最大化するからだ。Airbnbは2022Q1の収入が70%増の14億ドルになっても、Bookingの本業の宿泊事業の収入は28億ドル、広告などのその他の収益を合わせると33億ドルを超える可能性がある。もちろんAirbnbの強みはどんどん事業範囲を拡大していることだ。最終的な結果として、両社間の競争が激しくなり、他の同業者はパラダイムシフトしなければ 取り残されてしまう。

----------

The competition between Booking and Airbnb in Europe and the United States, from a financial point of view, is essentially when the room nights of Airbnb has doubled to the size of Booking, with Airbnb's business model, whether Airbnb could maintain more profitable than Booking, we believe the answer is Yes. However, now the two sides are not fully benchmark against each other. Airbnb chooses a market with a relatively small total number of SKUs, exclusive inventory, and high gross profit, while Booking, on the contrary, will do as long as the ROI can make money. We don't think that Booking would mind if Airbnb distributes its properties through channel managers. This strategy can maximize market share. Even if Airbnb’s revenue could increase by 70% to $1.4 billion in 2022Q1, Booking’s hotel industry revenue may still hold $2.8 billion, plus other revenue such as advertising would exceed $3.3 billion. Of course, Airbnb's strength is constantly expanding, the final result is that the two sides will compete fiercely, and the rest peers of the industry would be marginalized if they don't transform.

文章鏈接 Hyperlink:https://ir.bookingholdings.com/press-releases

資料來源 Resource:Bookingholdings

標籤 Label: Booking Airbnb Connected Trip Glenn Fogel Russia-Ukraine conflict ABNB BKNG