登錄

選單

登錄

海擇短評 Haize Comment:

Huazhu Hotels Group Ltd (NASDAQ: HTHT) recently disclosed its 2022Q3 earnings. Although the net profit has suffered a large loss, the operating profit is actually not bad, working hard during the pandemic. Some views shared by Haize Capital are as follows:

1. Regular operating profit: Huazhu’s Q3 GMV continued to grow YoY. Although the net loss reached RMB 710 million, it included RMB 310 million in unrealized losses on securities, RMB 360 million in exchange losses, and RMB 430 million in income taxes, the operating profit of RMB 500 million has reached 65% of the pre-pandemic historical high (RMB 775 million). Additionally, RevPAR(Revenue Per Available Room) for the quarter was 102% from the same period in 2019.

2. The scale of operation far exceeds that before the pandemic: as of the end of Q3, Huazhu owns 797,489 hotel rooms, increasing by 58% compared with 504,414 in the same period in 2019; the proportion of rooms in low-end hotels to mid-to-high-end hotels is 49:51, compared with 55:45 in the same period of 2019, and the product structure has also shifted to a higher unit price.

3. Overseas investment turned profit: This quarter, the Deutsche Hospitality brand acquired by Huazhu in Europe got out of the red for the first time, with EBITDA reaching RMB 94 million.

4. Faster layout in low-tier cities: From the perspective of the progress of newly signed hotels, the company announced that the H2 growth is about 80% of the normal period, but if China is divided into first-tier, second-tier cities and lower-tier cities, due to the stricter pandemic restrictions in first and second-tier cities, franchisees in lower-tier cities have higher confidence.

5. Q4 guidance is temporarily negative: Compared to Q3 RevPAR which has exceeded 2019, considering the tightening of winter pandemic controls, the company expects Q4 RevPAR in China to be about 70% to 75% of 2019.

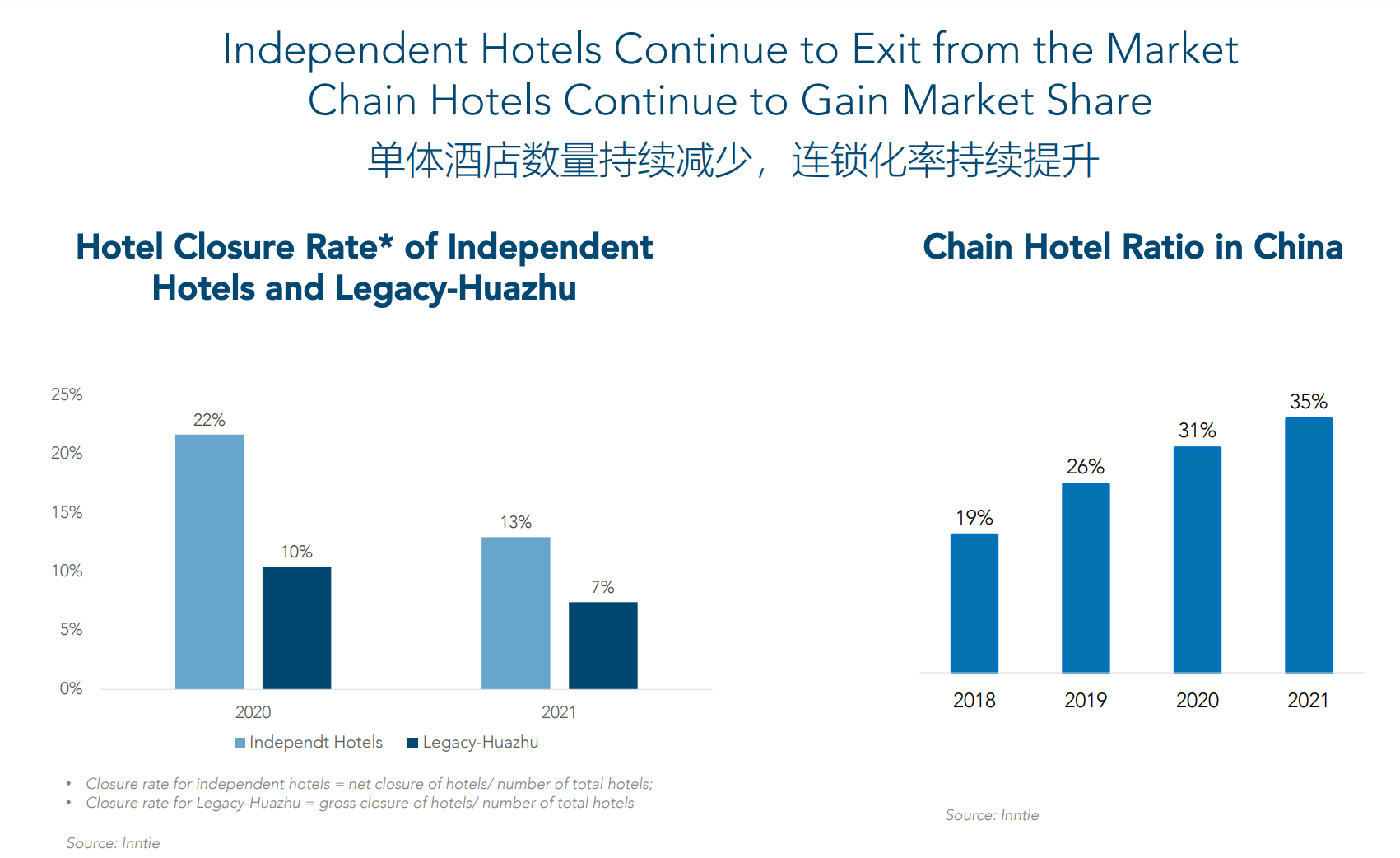

Summarizing the operating data of Huazhu Group since the pandemic, we believe that Huazhu is a company that has benefited from the pandemic. The main reason is that during the pandemic, independent hotels have weak anti-risk capabilities and are more likely to go bankrupt, which is more conducive to the development of chain hotels; the proportion of chain hotels in China's accommodation industry has increased from 19% in 2018 to 35% in 2021. Considering the stable franchise rate of 70% in the US hotel market, Chinese chain hotels may still have great growth opportunities, and Huazhu may be a company that will highly benefit from this trend.

----------

華住酒店集團(NASDAQ: HTHT)近期披露2022Q3財報,淨利雖然大幅虧損,但實際上運營利潤並不差,屬於一間在疫情間鴨子划水的公司。海擇資本分享部分觀點如下:

1. 運營利潤正常: 華住Q3的GMV繼續呈現YoY增長,雖然淨損達7.1億人民幣(以下同),但其中涵蓋3.1億的有價證券未實現損失、3.6億匯兌損失、4.3億所得稅,從運營利潤層面看盈利5.00億,已達疫情前歷史高點(7.75億)的65%。此外,本季的RevPAR為2019年同期的102%。

2. 運營規模遠超疫前:截至Q3結束,華住的的酒店客房數為797,489間,而2019年同期為504,414間,增長達58%;其中低端酒店與中高端酒店的客房數占比為49:51,2019年同期則為55:45,產品結構也往高單價改變。

3. 境外轉投資轉盈:本季華住在歐洲收購的Deutsche Hospitality品牌首度虧轉盈,EBITDA達9400萬人民幣。

4. 低線城市布局更快:從新簽約酒店進度而言,公司公告H2增速約為正常時期的80%,但若將中國區分為一線、二線城市和低線城市,由於疫情防控在一線和二線城市更為嚴謹,低線城市的加盟商的信心更高。

5. Q4預期暫偏負面:相對於Q3的RevPAR已超過2019年,基於冬季疫情防控趨嚴,公司預計Q4中國區的RevPAR約為2019年的70%至75%間。

盤點華住集團疫情以來的運營數據,我們認為華住屬於受惠於疫情的公司。主要原因是,疫情間單體酒店的抗風險能力較弱,更容易倒閉,更有利於品牌酒店發展;中國住宿業的連鎖酒店佔比從2018年的19%提升至2021年的35%,如果以美國酒店市場加盟連鎖率穩定在70%的高位來看,中國酒店品牌可能還有很大的成長機會,而華住可能會是高度受益於這個趨勢的公司。

----------

화주호텔그룹(华住, NASDAQ: HTHT)은 최근 2022년 3분기 실적을 발표했다. 비록 순이익이 비교적 큰 결손을 보았지만 코로나 기간의 노력운영을 거쳐 영업이익은 사실 괜찮았다. Haize Capital의 일부 관점은 다음과 같다.

1. 영업이익은 정상이다. 화주의 3분기 GMV는 전년 동기대비 계속 증가했다. 순손실이 7억1,000만 위안에 달했지만 미실현 유가증권 손실 3억1,000만 위안, 환차손 3억6,000만 위안, 소득세 4억3,000만 위안이 포함되어 있다. 5억 위안의 영업이익은 코로나 이전 역대 최고 수준(7억7,500만 위안)의 65%에 달했다. 또 이번 분기의 RevPAR은 2019년 동기보다 102% 증가했다.

2. 경영 규모가 코로나19 발생 이전을 훨씬 초과하다. 3분기가 끝날 때까지 화주의 호텔 객실 수는 797,489개로 2019년 동기의 504,414개에 비해 58% 증가했다. 저가형 호텔과 중고급 호텔의 객실 수 비율은 49: 51인데 2019년 동기에는 55: 45로 제품 구조도 높은 단가로 바뀌고 있다.

3. 해외투자가 흑자로 전환한다. 이번 분기에 화주는 유럽에서 인수한 Deutsche Hospitality는 처음으로 흑자로 전환했으며 EBITDA는 9,400만 위안에 달했다.

4. 저선 도시의 배치가 더 빠르다. 새로 계약한 호텔의 진전을 보면 회사는 하반기 성장속도를 정상시기의 80% 좌우로 선포했다. 그러나 만약 중국을 1, 2선과 저선 도시로 나눈다면 1, 2선 도시의 전염병예방통제가 더욱 엄격하기 때문에 저선 도시 가맹상들의 신심이 오히려 더욱 높다.

5. 4분기 실적 전망은 당분간 부정적이다. 겨울철 전염병 예방통제의 긴축을 고려할 때 이미 2019년을 넘어선 3분기 RevPAR에 비해 중국의 4분기 RevPAR은 2019년의 약 70~75% 사이로 예상된다.

코로나19 발생 이후 화주의 경영 데이터를 분석하면, 우리는 화주가 전염병으로부터 혜택을 받는 회사라고 생각한다. 주요 원인은 코로나19 발생 기간 독립 호텔의 위험 방지 능력이 약하고 파산하기 쉬운 반면에 호텔 체인의 발전에 유리하기 때문이다. 중국 숙박업에서 호텔 체인의 비율은 2018년 19%에서 2021년 35%로 높아졌다. 미국 호텔 시장의 70%의 안정적인 가맹률을 고려할 때, 중국 체인 호텔은 여전히 큰 성장 기회를 가질 수 있으며, 화주는 이러한 추세에 높은 혜택을 받는 회사일 수 있다.

資料來源 Resource:Huazhu Hotels Group Ltd

標籤 Label:Huazhu HTHT chain hotel COVID