登錄

選單

登錄

海擇短評 Haize Comment:

攜程(NASDAQ: TCOM)近期公告2022Q3財報,淨收入創疫情以來新高,GAAP的運營利潤也在疫情以來首度轉盈。中國在Q4揭露了新局面,雖然官方防控尚未終結,但開放方向已明朗化,旅遊行業的後疫情之戰於焉開始,想彎道超車攜程的公司將陸續表態。

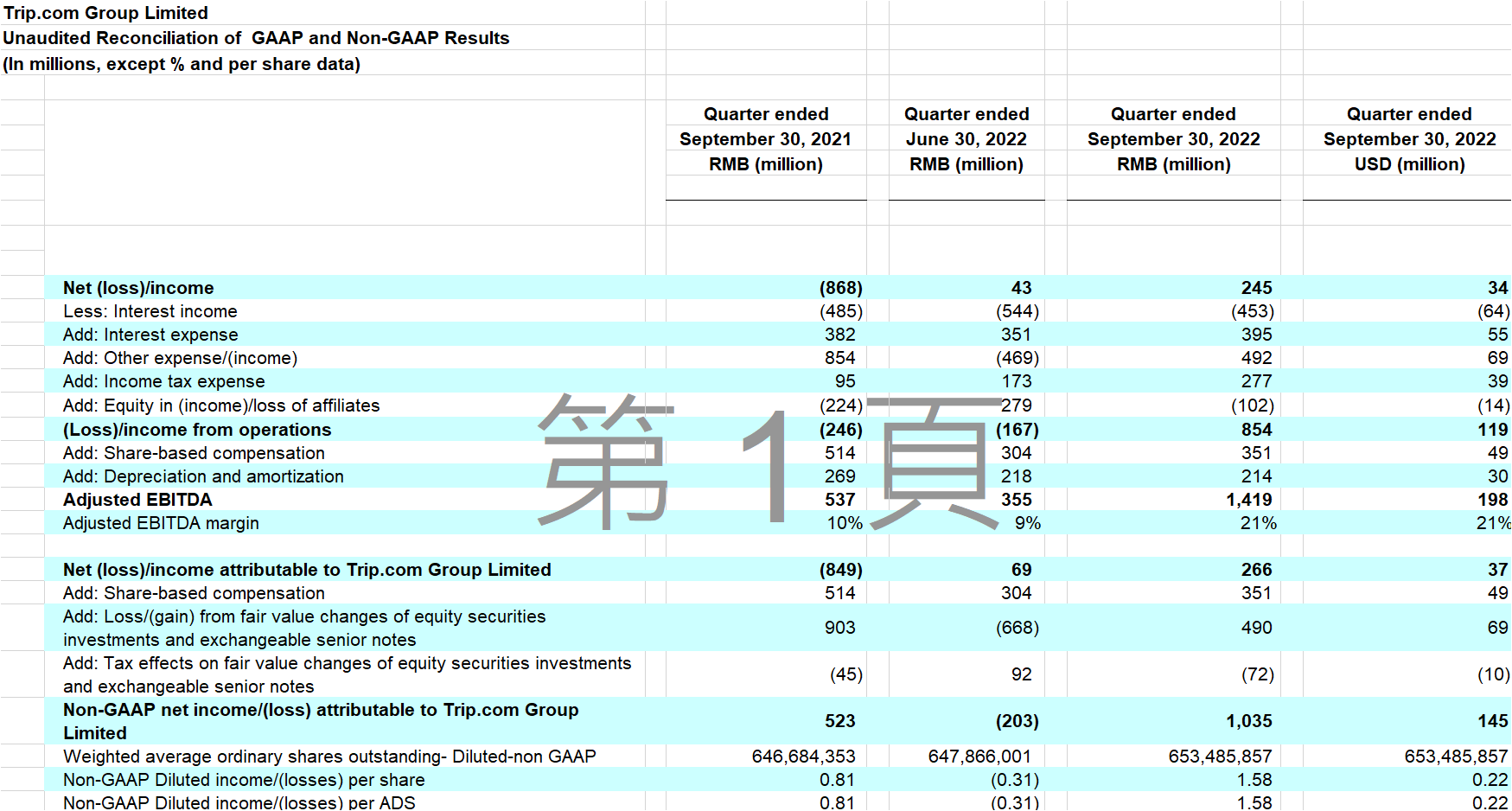

1. 疫情以來首度GAAP盈利:本季度攜程收入達69.0億元人民幣(以下同),GAAP的運營利潤首度轉正便盈利8.54億,是後疫情時期好的開始。與去年同期相比,本季收入增加29%,但運營費用僅增加9%,是盈利的主要原因;考慮到各國旅遊業目前對人力招募都偏向保守甚至缺工的態度,我們認為疫情後攜程的費用也會保持穩定,不會大規模暴升。

2. 機酒收入仍待恢復:從公司主營業務來看,Q3交通收入29.0億、住宿收入26.2億,兩者均為2019年的70%;由於國境尚未開放,這算是不錯的表現。

3. 國際酒店東南亞增速快:攜程Q3國際平台收入佔總收入的15%至20%,其中酒店間夜數較2019年同期增長超45%,印尼、馬來西亞、香港等地的酒店間夜均較2019年實現三位數增,這些區域在2019年雖然基數不大(香港受政治影響),但後勢可觀察。

4. 海外交通與活動亦有增長:國際平台的機票預訂量恢復到2019年同期的80%以上;海外活動體驗交易額創歷史新高。

5. 國內間夜單月超2019:攜程7月單月酒店間夜比2019年同期增長約20%,雖然8月回落,但高端酒店結合TripPLUS(類似Tripadvisor Plus)的銷售也值得觀察,也許Tripadvisor在歐美沒做成的事業,在亞洲攜程可以做成,畢竟這是強運營的產品模式。

6. Q4預期較弱:攜程基於冬季淡季,與第一波感染潮,對Q4沒有給到太高的預期。不過,疫情將過,再淡的旅遊季也會有黎明,重點在於後疫情新戰場即以什麼形式開啟廝殺。

----------

Trip.com (NASDAQ: TCOM) announces its 2022Q3 results, with net revenue hitting a new high since the pandemic and GAAP operating profit getting out of the red for the first time since the pandemic. China has revealed a new chapter in Q4, although the official pandemic control has not yet ended, the trend of opening up has become clear. The post-pandemic battle in the tourism industry has begun.

1. The first profitable GAAP since the pandemic: Trip’s revenue in this quarter reaches 6.90 billion yuan (the same below), and the GAAP operating profit reaches 854 million yuan, which is a good start for the post-pandemic period. Compared with the same period last year, revenue of this quarter has increased by 29%, but operating expenses increased by only 9%, which was the main reason for the profit; Considering that the tourism industry in various countries is currently conservative in manpower recruitment and labor shortage, we believe that Trip’s expenses will remain stable after the pandemic and will not skyrocket on a large scale.

2. Revenue from air tickets and hotels still needs to recover: from the perspective of the company’s main business, Q3 mobility revenue was 2.90 billion and accommodation revenue was 2.62 billion, both of which were 70% of 2019; since China's border has not yet been opened, this is a good performance.

3. The international hotels growth in Southeast Asia is fast: The company's Q3 international platform revenue accounts for 15% to 20% of total, of which the number of hotel room nights has increased by more than 45% over the same period in 2019. Hotel room nights in Indonesia, Malaysia, Hong Kong and other places have all achieved triple-digit growth over 2019, although the base in these regions is not large in 2019 (Hong Kong is affected by politics), we can track the future trend.

4. Overseas transportation and activities have grown: the flight booking volume on international platforms has recovered to more than 80% of the same period in 2019; the GMV of overseas activity/experience has reached a record high.

5. Single month domestic hotel room nights exceeded 2019: Trip’s hotel room nights in July increased by about 20% compared with the same period in 2019. Although it fell back in August, the sales of high-end hotels combined with TripPLUS (similar to Tripadvisor Plus) is worth tracking. Maybe What Tripadvisor failed to achieve in Europe and the United States, Trip can make it in Asia. After all, this is a product model with strong operations.

6. Weak guidance for Q4: Based on the winter off-season and the first wave of infections, Trip.com did not give highly positive guidance for Q4. However, the pandemic will end, and there will be a dawn in the weakest tourist season. The key lies in the competition in the new post-pandemic era.

----------

Trip.com(NASDAQ: TCOM)은 2022년 3분기 실적을 발표했다. 순수익은 코로나 사태 이후 최고치를 기록했고, GAAP 영업이익은 코로나 사태 이후 처음으로 흑자로 돌아섰다. 중국은 4분기에 새로운 장을 열었다. 코로나19의 방역통제는 아직 공식적으로 끝나지 않았지만 개방의 추세는 가시화되었다. 포스트 코로나 시대 관광업의 전투가 시작됐다.

1. 코로나 사태 이후 처음으로 GAAP 이윤을 실현했다. 이번 분기 Trip.com의 매출은 69억 위안, GAAP의 영업이익은 8억 5,400만 위안으로 포스트 코로나 시기에 좋은 출발을 했다. 전년 동기 대비 이번 분기 매출은 29% 증가했지만, 영업비용은 9% 증가하는 데 그쳤다. 이것은 흑자로 돌아선 주요 원인이다. 현재 각국 관광업의 인력 채용에 대한 태도가 비교적 보수적이라는 점을 고려할 때, 우리는 포스트 코로나 시대 Trip.com의 비용이 안정적으로 유지될 것이며, 대규모로 치솟지는 않을 것이라고 생각한다.

2. 항공권과 호텔 수입은 여전히 회복되어야 한다. 회사의 주요 영업 업무를 보면, 3분기 교통이동 수입은 29억 위안, 숙박 수입은 26억 2,000만 위안으로 모두 2019년의 70%였다. 중국은 입국이 아직 개방되지 않았기 때문에, 이것은 매우 좋은 표현이었다.

3. 동남아시아 지역의 국제 호텔의 성장 속도가 매우 빠르다. Trip.com의 3분기 국제플랫폼 수입은 총수입의 15~20%를 차지했는데 그중 호텔객실의 숙박수는 2019년 동기대비 45%를 초과했다. 인도네시아, 말레이시아, 홍콩 등 지역의 호텔 객실 숙박수는 2019년에 모두 세 자릿수 증가를 기록했다. 이들 지역은 2019년 기준수가 크지 않지만 (홍콩은 정치적 영향을 받기 때문에) 우리는 미래의 추세를 주시할 수 있다.

4. 해외 교통과 여행 활동이 모두 증가했다. 국제 플랫폼의 항공권 예약량은 2019년 동기대비 80% 이상으로 회복됐다. 해외 액티비티 체험 GMV은 사상 최고를 기록했다.

5. 국내 월간 호텔 객실 숙박수가 2019년을 넘어섰다. Trip.com의 7월 호텔 객실 숙박수는 2019년 같은 기간에 비해 약 20% 증가했다. 8월에는 하락했지만 프리미엄 호텔과 TripPLUS(Tripadvisor Plus와 유사) 매출은 주목할 만하다. Tripadvisor가 유럽과 미국에서 이루지 못한 성과는 Trip.com이 아시아에서 성공할 수 있다. 결국 이것은 강한 운영 능력을 가진 제품 모델이다.

6. 4분기 실적 전망이 부진하다. 겨울 비수기와 대규모 감염 충격의 첫 번째 파동에 기초하여, Trip.com은 4분기 실적 가이던스에 대해 큰 기대를 하지 않고 있다. 그러나 포스트 코로나 시대 가장 약한 관광철에도 새벽이 찾아올 것이다. 관건은 포스트 코로나 시대의 경쟁이 어떤 형식으로 시작되느냐에 있다.

文章鏈接 Hyperlink:https://investors.trip.com/

資料來源 Resource:Trip.com

標籤 Label:Trip.com TCOM China TripPLUS flight accommodation post-pandemic