登錄

選單

登錄

海擇短評 Haize Comment:

在美國上市的旅遊類公司今年以來市值一片大好之際,GDS公司Sabre(NASDAQ: SABR)近期公告2022Q4財報後,果然不出意外的又出意外,盤中跌幅峰值25%,收盤大跌19%,這間公司發生了重大風險嗎?海擇資本的觀點如下:

1. EBITDA大幅偏離預期:公司Q4財報公告單季Adjusted EBITDA盈利147萬美元,相對原本預期盈利3,000萬美元大幅減少。由於此前11月初公告Q3財報時,未有任何預警,公司也說明亞洲航空運力Q4繼續復甦,情勢一片大好。Sabre在前三季已盈利6,387萬美元,對Q4的預期也很樂觀,因此財報公告後跌破眾人眼鏡,股價大跌並不奇怪。

2. 2022年體質好轉:回顧Sabre在2022Q1時給的全年預期可以發現,當時高標預期Adjusted EBITDA盈利1.65億美元,中標預期盈利1,500萬美元,低標預期虧損8,500萬美元,最後全年結算盈利6,534萬美元。其實公司的財務表現並未脫離原本的預期範圍,只能說前三季給了太高的預期,Q4未達預期讓投資人大失所望。

3. Sabre的財測可信度一直是個問題:Sabre在科技上是一間技術紮實穩健的GDS公司,後疫情時期依然有價值,即便有航空公司想轉用NDC(New Distribution Capability),在當前生態下,最理智的決定也是使用GDS公司提供的NDC服務,仍然無法擺脫Amadeus(BME: AMS)與Sabre而存在。然而,在過去的海擇觀點,我們也提過,在市值變動上,Sabre一直是家神操作的公司,即便放大到全世界,它也是唯一的一家在2022年就公告2025年財測的公司,而且指標還很激進,2025年的Adjusted EBITDA預期為13億美金,考慮到2022年結算連1億美金都不到,只能說是自信爆棚。

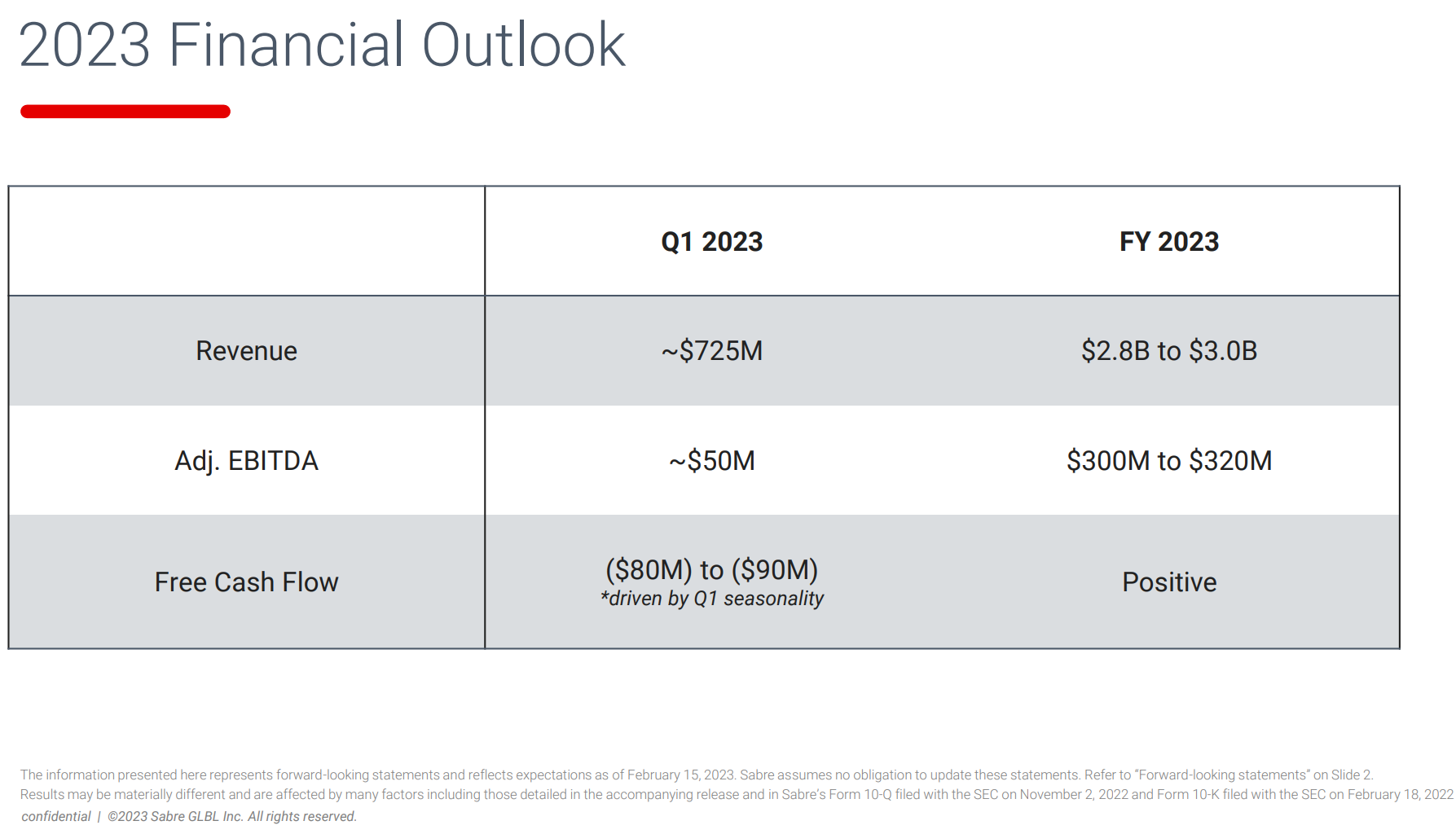

簡單來說,這次Sabre市值暴跌,其實可以视為投資人對公司今年財務預期的人氣投票。亦即,Sabre說2023年Q1的Adjusted EBITDA為5,000萬美元,全年3.2億美元,你信嗎?(其實Q1的部份我們信)。

----------

At a time when the market value of US-listed tourism companies has been booming this year, GDS company Saber (NASDAQ: SABR) recently announced its 2022Q4 earnings. The result, out of the blue as you may have expected. The peak drop of the day was 25%, and the closing price fell 19%. Is there a major risk in this company? The view of Haize Capital is as follows:

1. EBITDA greatly deviates from the guidance: the company’s Q4 earnings announced a single-quarter Adjusted EBITDA profit of $1.47 million, significantly decreasing from the previous expecting profit of $30 million. Since there was no alert when the Q3 earnings were released in early November, the company also stated that the air capacity in Asia continued to recover in Q4, the outlook at that time seemed very good. Saber has made a profit of $63.87 million in the first three quarters, and also has a positive guidance for Q4. Therefore, it is not surprising that Saber's stock price fell sharply after the company released Q4 earnings.

2. Company operation has iImproved in 2022: Looking back at the full-year forecast given by Saber in 2022Q1, it can be found that the maximum forecast of Adjusted EBITDA was a profit of $165 million, the median forecast was a profit of $15 million, and the minimum forecast was a loss of $85 million; in the end, the whole year settlement was a profit of $65.34 million. In fact, the company's financial performance has not deviated from the original forecast range. We can only say that the company gave too optimistic expectations in the first three quarters, and investors were greatly disappointed by Q4's failure to meet expectations.

3. The reliability of Sabre's financial forecast has always been a problem: Sabre is a GDS company with solid and stable technology, and has a value in the post-pandemic era. Some airlines may want to adopt NDC (New Distribution Capability), but under the current circumstances, the most sensible decision is to use GDS companies' NDC service, airlines still cannot abandon Amadeus (BME: AMS) and Sabre. However, we also mentioned in the past Haize Comment that Sabre has always been a peculiar and radical company in terms of market value changes. Looking at the world, Sabre is the only company that would give 2025 financial guidance in 2022, and the figures were very aggressive. Its forecast of 2025 adjusted EBITDA is $1.3 billion, considering that the settlement in 2022 is less than $100 million, we can only say the company is full of confidence.

To put it simply, the plunge in Saber's market value this time can actually be regarded as the result of investors' voting on the company's financial forecast for this year. In other words, Saber said that the Adjusted EBITDA of 2023Q1 is $50 million, and the annual figure will be $320 million. Do you believe it? (In fact, we believe in the part of Q1).

----------

올해 미국에 상장된 여행사들의 시가총액이 높아지는 가운데 GDS 회사 Sabre(NASDAQ: SABR)는 최근 2022년 4분기 실적을 발표했다. 결과는 뜻밖이었다. 이날 최고 낙폭은 25%, 종가는 19% 하락 마감했다. 이 회사에 중대한 위험이 존재한가? Haize Capital의 관점은 다음과 같다.

1. EBITDA는 전망에서 크게 벗어났다. 회사의 4분기 재무실적은 분기별 Adjusted EBITDA 이익이 147만 달러로 당초 예상했던 3,000만 달러보다 크게 감소했다고 발표했다. 11월 초 3분기 실적 발표에서 아무런 경보가 없었기 때문에, 회사는 동시에 아시아 지역의 항공 수송력이 4분기에 계속 회복될 것이며, 당시의 전망은 매우 좋았던 것 같다고 밝혔다. Sabre의 지난 3분기 이익은 6,387만 달러였으며 4분기에 대한 전망도 낙관적이었다. 따라서 Sabre가 4분기 수익을 발표한 후 주가가 크게 하락한 것도 이상할 것이 없다.

2. 회사 운영은 2022년에 개선되었다. Sabre가 2022년 1분기에 제시한 연간 전망을 돌이켜보면 Adjusted EBITDA의 최고 전망치는 1억 6,500만 달러, 중위수 전망치는 1,500만 달러, 최저 전망치는 -8,500만 달러라는 것을 알 수 있다. 결국 연간 결산이익은 6,534만 달러였다. 사실 회사의 재무 실적은 당초 전망 범위를 벗어나지 않았다. 회사가 지난 3분기에 지나치게 낙관적인 전망을 내놓았고, 4분기에 기대에 미치지 못해 투자자들을 매우 실망시켰다고 말할 수밖에 없다.

3. Sabre 재무 예측의 신뢰성은 항상 문제였다. Sabre는 기술이 탄탄하고 안정적인 GDS 회사로 포스트 코로나 시대에 가치가 있다. 일부 항공사는 NDC(New Distribution Capability)를 채택하고 싶을 수도 있다. 하지만 현재 상황에서 가장 현명한 결정은 GDS사가 제공하는 NDC 서비스를 사용하는 것이다. 항공사는 여전히 Amadeus(BME: AMS)와 Sabre를 포기할 수 없다. 그러나 우리는 과거 코멘트에서도 Sabre가 시장 가치 변화에 있어서 특이하고 급진적인 회사였다고 언급했다. 전 세계를 내다보면 Sabre는 2022년에 2025년의 재무전망을 준 유일한 회사이며 이런 수자는 모두 매우 급진적이다. 2025년 Adjusted EBITDA의 전망은 13억 달러다. 2022년 결산이 1억 달러 미만이라는 점을 감안하면 회사가 지나치게 자신감을 갖고 있다고 할 수밖에 없다.

간단히 말해서, Sabre의 이번 시가총액 폭락은 사실상 투자자들이 이 회사의 올해 재무 전망에 대한 투표 결과로 볼 수 있다. Sabre가 2023년 1분기에 Adjusted EBITDA가 5,000만 달러, 연간 Adjusted EBITDA가 3억2,000만 달러에 이를 수 있다고 밝혔다면, 믿을 수 있는가?(사실, 우리는 1 분기의 예상을 믿는다.)

文章鏈接 Hyperlink:https://investors.sabre.com/events-%26-presentations

資料來源 Resource:Sabre

標籤 Label:tourism GDS SABR