登錄

選單

登錄

海擇短評 Haize Comment:

Tripadvisor(NASDAQ: TRIP)近期公告2022Q4財報,新CEO Matt Goldberg在2022年底,似乎終於明確了未來要走的路:短期自省在酒店領域終難與OTA匹敵,中期看玩樂體驗的成長極限,長期試圖靠AI再創媒體價值。海擇資本分享部分觀點如下:

1. 盈利復甦弱於收入:Tripadvisor的Q4收入為3.54億美元,已達到2019年的106%;不過Adjusted EBITDA為4,300萬,僅為2022Q3的37%,2019Q4的47%,主要原因在於高margin的酒店事業復甦太弱,在玩樂體驗也必須不斷進行投入。

2. 酒店事業復甦慢:Q4做為Tripadvisor核心的酒店事業收入約為2019年同期的85%,在Booking(NASDAQ: BKNG)、Airbnb(NASDAQ: ABNB)這些主要跨國OTA的收入與間夜都能不亞於2019年同期的背景下,已可斷定Tripadvisor做為媒體的價值已不如2019年,而且短期間無法逆轉局勢,這甚至與公司是否願意再投入Tripadvisor Plus的關係也不大。

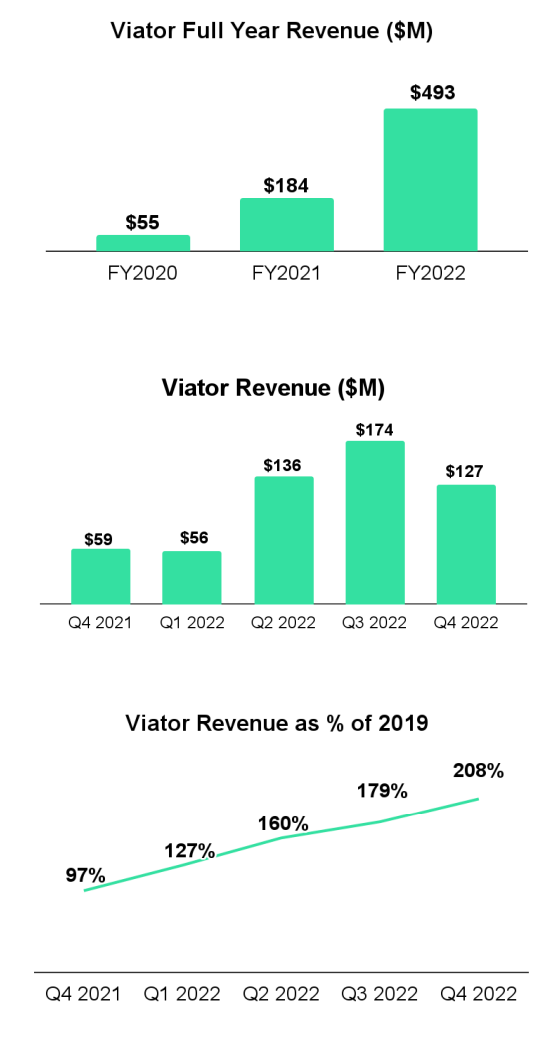

3. 體驗收入高增長的背後: Tripadvisor在2022年的最大亮點,就是Viator繼續在交易額與收入創下新高,全年交易額與收入分別為27億美元與4.93億美元,各為2019年186%與171%。公司認為2025年該市場產值將超過2,750億美元,由於約70%仍處於線下狀態,對於專長於線上的Tripadvisor是重要的機會。不過這個領域的競爭仍然非常激烈,很多同業仍不盈利,Viator能為消費者與合作夥伴長期提供什麼獨到的價值、何時才能在財務面規模盈利,這仍然是個問題。

4. 嘗試以AI重塑媒體價值:最近ChatGPT受到重視,在財報會議提及將步入Generative AI的公司很多,Tripadvisor並不特殊。但值得留意的是,Tripadvisor擁有超過10億條評論為核心的龐大內容資產,如果公司能將數據和內容接入適合的第三方技術,完成新一代的AI旅遊顧問,成為真正的Trip"Advisor",也許能以更個性化的方式滿足旅行者,協助其做旅行決策,或許真能會成為Tripadvisor重造媒體價值的機會,這並不容易,但至少其資源比純粹以交易為主的OTA豐富。

----------

Tripadvisor (NASDAQ: TRIP) announces its 2022Q4 earnings. At the end of 2022, its new CEO Matt Goldberg seems to have finally determined the direction of the future: in short-term, to introspect that it would be difficult to compete with OTAs in the hotel field; in mid-term, to discover the growth limit of experience/activity, and in long-term tries to create media value again relying on AI . Some views shared by Haize Capital are as follows:

1. Profit recovery is weaker than revenue: Tripadvisor’s Q4 revenue was $354 million, which has reached 106% of 2019; however, the Adjusted EBITDA of $43 million was only 37% of 2022Q3 and 47% of 2019Q4. The main reason is that the recovery of the high-margin hotel business is too weak, and continuous investments have been made in the experience/activity business.

2. The recovery of the hotel business is slow: as the core of Tripadvisor, the Q4 hotel business revenue was about 85% of the same period in 2019, while the revenue and room nights of major multinational OTAs such as Booking (NASDAQ: BKNG) and Airbnb (NASDAQ: ABNB) were neither weaker than the same period in 2019, it can be concluded that the value of Tripadvisor as a media is not as good as in 2019, and the situation cannot be reversed in a short period of time. This does not even have much to do with whether the company is willing to invest in Tripadvisor Plus again.

3. Behind the high growth of experience revenue: The brightest spot of Tripadvisor in 2022 is that Viator continues to hit new highs in GMV and revenue, the annual GMV of $2.7 billion and revenue of $493 million have reached 186% and 171% of 2019 respectively. The company believes that the value of experience/activity will exceed $275 billion in 2025. Since about 70% of the market has yet to be digitized, making it an important opportunity for Tripadvisor, which specializes in online. However, the competition in this field is still very fierce, and many peers are still not profitable. What unique value Viator can provide consumers and partners in the long run, and when will it be profitable financially are still questions.

4. Try to reshape media value relying on AI: ChatGPT has received attention recently, many companies mentioned that they will step into Generative AI, and Tripadvisor is no exception. But it is worth noting that Tripadvisor has a huge content asset with more than 1 billion reviews as the core. If the company can connect data and content to suitable third-party technology, create a new generation of AI travel consultants and become a real Trip "Advisor" , may be it could satisfy travelers in a more personalized way and assist them in making travel decisions, this may really become an opportunity for Tripadvisor to recreate the value of media. This is not easy, but at least its resources are more abundant than OTAs that are purely selling products.

----------

Tripadvisor(NASDAQ: TRIP)는 2022년 4분기 실적을 발표했다. 신임 CEO Matt Goldberg는 2022년 말에 마침내 미래의 방향을 정한 것 같다. 그는 단기에는 호텔 분야에서 OTA와의 경쟁이 어려울 것을 생각한다. 중기에는 체험/활동의 성장 한계를 발견한다. 장기에는 인공지능에 의존하여 미디어 가치를 재창조한다. Haize Capital의 관점은 다음과 같다.

1. 이윤 회복이 수입보다 약하다. Tripadvisor의 4분기 수입은 3억 5,400만 달러로 2019년의 106%에 달했다. 그러나 4,300만 달러의 Adjusted EBITDA는 2022년 3분기의 37%, 2019년 4분기의 47%에 그쳤다. 주요 원인은 이윤이 높은 호텔 업무의 회복이 너무 부진하기 때문에 체험/활동 업무에 지속적으로 투입해야 한다.

2. 호텔 업무의 회복이 더디다. Tripadvisor의 핵심인 4분기 호텔 사업 수입은 2019년 동기의 약 85%인데 Booking(NASDAQ: BKNG)과 Airbnb(NASDAQ: ABNB) 등 주요 다국적 OTA의 수입과 룸나잇은 2019년 동기대비 낮지 않다. Tripadvisor의 가치가 미디어로서 2019년보다 못하다는 결론을 내릴 수 있다. 그리고 이런 상황은 단시간에 역전될 수 없다.심지어 이 회사가 Tripadvisor Plus에 다시 투자하기를 원하는지와도 큰 관계가 없다.

3. 체험 매출 고성장의 배후: Tripadvisor 2022년의 가장 큰 하이라이트는 Viator의 GMV와 매출이 지속적으로 최고치를 경신하고 있으며, 연간 27억 달러의 GMV와 4억 9,300만 달러의 매출은 각각 2019년의 186%와 171%에 달한다. 이 회사는 2025년까지 체험/활동의 가치가 2,750억 달러를 넘을 것으로 보고 있다. 시장의 약 70%가 아직 디지털화되지 않았기 때문에 온라인 사업을 전문으로 하는 Tripadvisor에게 중요한 기회다. 그러나 이 분야의 경쟁은 여전히 매우 치열하며 많은 동업자는 여전히 수익을 내지 못하고 있다. 장기적으로 Viator가 소비자와 파트너에게 어떤 독특한 가치를 가져다 줄 수 있는지, 언제 재무적으로 이익을 낼 수 있을지는 미지수다.

4. AI에 의존하여 미디어 가치를 재창조하려고 시도한다. ChatGPT가 최근 주목을 받고 있다. 많은 회사들이 생성식 AI에 진입할 것이라고 언급하고 있으며, Tripadvisor도 예외는 아니다. 그러나 Tripadvisor는 10억 명이 넘는 리뷰를 핵심으로 하는 방대한 콘텐츠 자산을 보유하고 있다는 점에 주목할 필요가 있다. 이 회사가 데이터와 콘텐츠를 적절한 타사 기술과 연결하여 차세대 AI 여행 컨설턴트를 만들어 진정한 Trip 'Advisor'가 될 수 있다면, 더 개성화된 방식으로 여행자를 만족시키고 여행 결정을 내릴 수 있도록 도울 수 있을 것이며, 이는 정말 Tripadvisor가 미디어 가치를 재창조할 수 있는 기회가 될 수 있을 것이다. 이것은 쉽지 않지만 적어도 단순히 제품을 파는 OTA보다 자원이 더 풍부하다.

文章鏈接 Hyperlink:https://ir.tripadvisor.com/events-and-presentations

標籤 Label: TRIP Hotel Experience Viator AI