登錄

選單

登錄

海擇短評 Haize Comment:

華住集團(NASDAQ: HTHT)近期公告2022Q4財報,由於中國Q4封控趨嚴,中國境內的淨利仍處於虧損,但境外所收購事業已虧轉盈。疫情三年,公司在中國的多品牌與下沉市場頗有所成,後疫情可望收割,但歐洲在當前地緣政治氛圍下,不會是最好的國際化場域。海擇資本節錄部分觀點如下:

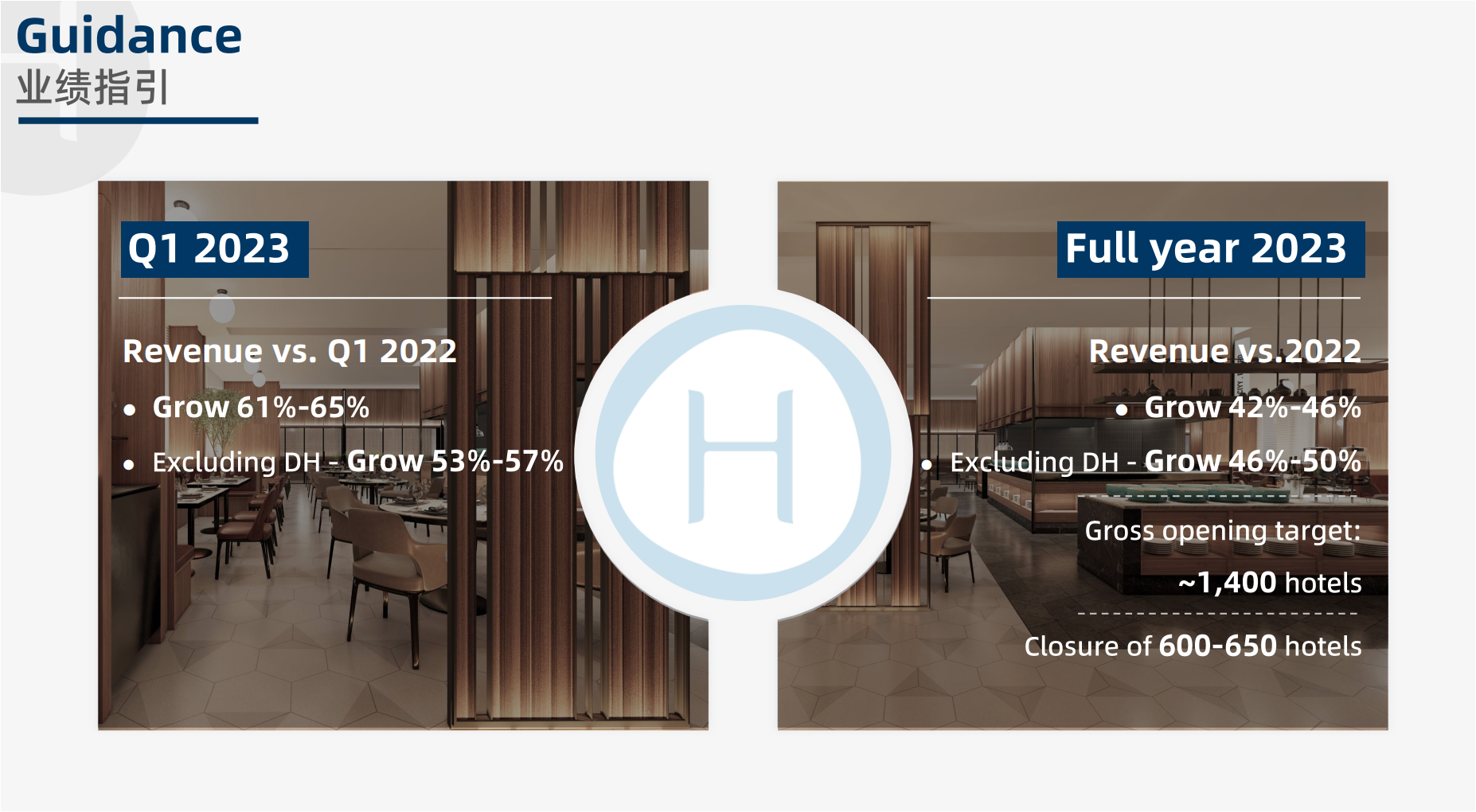

1. Q4虧損為近期低點:華住Q4基於GAAP會計準則淨損1.27億人民幣,淨損較Q3及去年同期低,Adjusted EBITDA則盈利3.98億元人民幣。Q4封控雖然趨嚴,但華住在中國的RevPAR已連續數月復甦,去年10月、11月、12月的RevPAR分別恢復到2019年同期的74%、87%、91%,而今(2023)年1月和2月則更推高至96%與140%。

2. 中高端多品牌遍地開花:疫情三年間,華住除了酒店的總覆蓋數(8,543家)與客房數(809,478間)有長足增長,分別比2019年同期增加52%與51%;在中高端的布局也增加不少,2022年底的中高端酒店達3,595間,佔整體的42%,而2019年底的中高端酒店為2,133間,佔整體的38%。雖然從佔比看相差不大,但從城市看,華住是在低線城市新增了經濟酒店,而主要城市則移除經濟酒店改設中高端酒店。

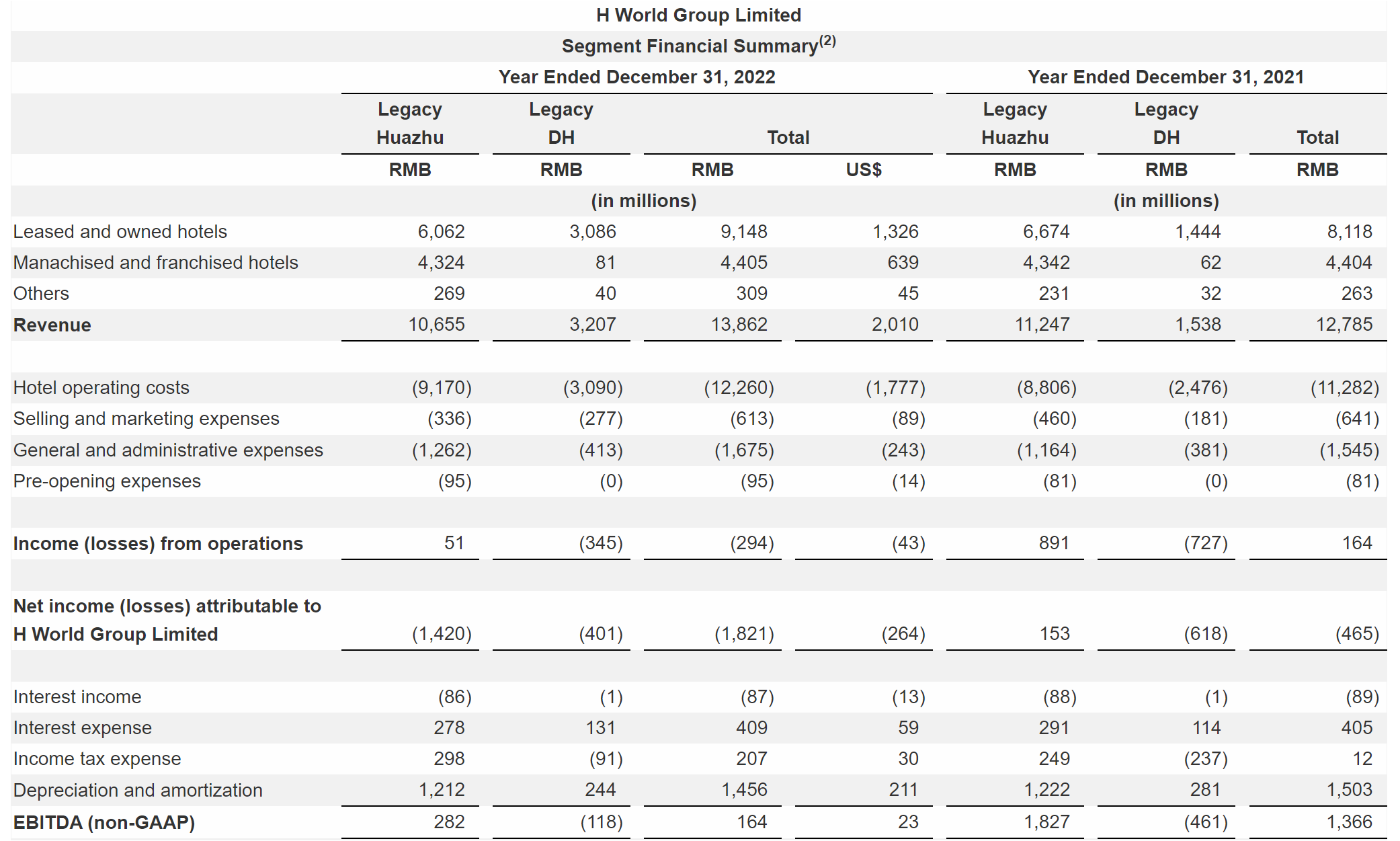

3. 境外虧轉盈:華住自收購德意志酒店集團(DH, DeutscheHospitality)以來,全年首度盈利,Adjusted EBITDA盈利1.34億元人民幣。華住雖然證明了能盤活虧損資產的運營能力,但在當前地緣政治氛圍下,歐洲不會是最好的國際化場域,或許東南亞、中東、南美,會更適合華住伸展。

4. 消費復甦或可期待:華住針對2023Q1與2023全年,分別給到YoY增長53%-57%與46-50%的預期;由於2022Q1與2022全年都比2019年好,實質上等於是比2019Q1至少增長72%、比2019全年至少增長81%,這是很不錯的預期了。從市值看,投資人目前似乎並不認同華住的高成長,後續值得跟進觀察。

----------

Huazhu Hotels Group(NASDAQ: HTHT) announced its 2022Q4 financial results, with net profit in China still in the red due to tighter COVID policies, but the acquired business outside of China has turned a loss into a profit. In the three years of the pandemic, the company's multi-brand and low-end market in China has made an achievement, and it is expected to harvest after the pandemic, but Europe is not the best market for internationalization under the current geopolitical atmosphere. Some views by Haize Capital are as follows:

1. Q4 loss is a recent low: Q4 GAAP-based net loss of Huazhu is RMB127 million, a lower net loss than Q3 and the same period last year, Adjusted EBITDA made a profit of RMB 398 million. Despite the tightening COVID control in Q4, Huazhu's RevPAR in China has recovered for several months in a row. RevPAR in October, November and December of last year recovered to 74%, 87% and 91% of the same period in 2019 respectively, and pushed up to 96% and 140% in January and February of this year (2023).

2. Mid-to-high-end multi-branding is blooming everywhere: During the three years of the pandemic, in addition to the significant growing number of hotels(8,543) and rooms (809,478), an increase of 52% and 51% respectively compared with the same period in 2019; the layout of mid-to-high-end has also expanded a lot, with 3,595 mid-to-high-end hotels at the end of 2022, accounting for 42% of the total, while there were 2,133 mid-to-high-end hotels at the end of 2019, accounting for 38% of the total. Although the proportions have no big gap, in terms of cities, Huazhu is adding budget hotels in low tier cities, while replacing budget hotels with mid- to high-end hotels in major cities.

3. Overseas business loss to profit: Since the acquisition of DeutscheHospitality, Huazhu made its first profit for the year, with Adjusted EBITDA profit of RMB134 million. Although Huazhu has proven its ability to revitalize loss-making assets, Europe is not the best place for internationalization in the current geopolitical climate, perhaps Southeast Asia, the Middle East and South America would be more suitable for Huazhu's expansion.

4. Consumption recovery may be promising: For 2023Q1 and 2023 full year, Huazhu has given the guidance of 53%-57% growth YoY and 46-50% growth YoY respectively; as 2022Q1 and 2022 full year are better than 2019, it is at least an increase of 72% compared to 2019Q1 and an increase of 81% compared to 2019 full year, which is a highly positive guidance. From the market value, it seems that the potential of Huazhu has yet to be recognized by investors, it is worth to follow up.

----------

화주호텔그룹(NASDAQ: HTHT)은 2022년 4분기 재무실적을 발표했다. 4분기 코로나 예방 · 통제 정책의 영향으로 중국 시장의 순이익은 여전히 적자 상태지만 해외 사업은 흑자로 돌아섰다. 코로나 발생 3년 동안 회사는 중국의 멀티 브랜드와 저가시장에서 성과를 거두었고 포스트 코로나 시기에 수확이 기대되지만 현재 지연정치적 분위기에서 유럽은 국제화의 가장 좋은 시장이 아니다. 하이저 캐피털의 일부 관점은 다음과 같다.

1. 4분기 적자는 최근 최저치를 기록했다. GAAP 회계 준칙에 근거하여 화주의 4분기 순손실은 인민폐 1억 2,700만 위안으로 순손실은 3분기와 전년 동기대비 낮았고 Adjusted EBITDA는 3억 9,800만 위안의 흑자를 냈다. 4분기 코로나 예방 · 통제가 엄격했지만 중국 시장의 RevPAR은 수개월 연속 회복됐다. 지난해 10월과 11월, 12월 RevPAR는 2019년 같은 기간의 74%, 87%, 91%로 회복했다가 올해(2023년) 1월과 2월에는 각각 96%, 140%로 반등했다.

2. 중고급 멀티 브랜드가 도처에 꽃을 피우다. 코로나 3년 동안 호텔 수 (8,543개) 와 객실 수(809,478개)가 눈에 띄게 늘었다. 2019년 같은 기간에 비해 각각 52%, 51% 증가했다. 이 외에도 중고급 호텔 배치도 적지 않게 확대됐다. 2022년 말 중고급 호텔은 3,595개로 42%를 차지한다. 이에 비해 2019년 말 중고급 호텔은 2,133개로 38% 를 차지했다. 비록 비례격차가 크지 않지만 도시를 보면 화주는 저선도시에서 경제형호텔을 증가시켰고 주요도시에서는 중고급호텔로 경제형호텔을 대체했다.

3. 해외 사업은 적자에서 흑자로 전환됐다. 도이치 호스피탈리티(DH, DeutscheHospitality)를 인수한 이래 화주호텔은 년내 첫 이윤을 실현했으며 Adjusted EBITDA의 이윤은 1억 3,400만 위안이였다. 비록 화주가 이미 결손자산을 활성화하는 능력을 증명하였지만 현재의 지연정치적 분위기에서 유럽은 국제화의 가장 좋은 장소가 아니다. 아마도 동남아시아, 중동, 남미는 화주의 확장에 더 적합할 것이다.

4. 소비가 살아나거나 희망이 있다. 화주는 2023년 1분기와 2023년 한 해 동안 각각 전년 동기 대비 53~57%, 46~50% 성장할 전망을 지도했다. 2022년 1분기는 2019년 같은 기간에 비해 최소 72% 증가했다. 2022년 한 해는 2019년 한 해와 비교해 81% 증가했다. 이것은 매우 적극적인 지도다. 시가로 볼 때 화주의 잠재력은 아직 투자자의 인정을 받지 못한 것 같아 더 지켜볼 필요가 있다.

文章鏈接 Hyperlink:https://ir.hworld.com/news-releases/news-release-details/h-world-group-limited-reports-fourth-quarter-and-full-year-2022

資料來源 Resource:Huazhu

標籤 Label:HTHT Hotel Investment Post-Pandemic