登錄

選單

登錄

海擇短評 Haize Comment:

同程旅行(HK: 0780)近期公告2023Q1財報。同程Q1交易額與Adjusted EBITDA同創歷史新高,多項運營指標相對2019年同期也大有好轉,近年同程在行銷上投入不少費用發展微信小程序外的通路,這些月活是否能轉化成出境遊相關的收益,可能是同程未來能否再上一層樓的關鍵。海擇資本的部分觀點如下:

1. 財務表現創歷史新高:本季同程總交易額572億人民幣,YoY增長77%,較2019年同期增長59%;Adjusted EBITDA為7.3億人民幣,YoY增長67%,較2019年同期增長19%。僅憑中國境內業務就能讓同程盈利創下歷史新高,是同程本期的重要里程碑。

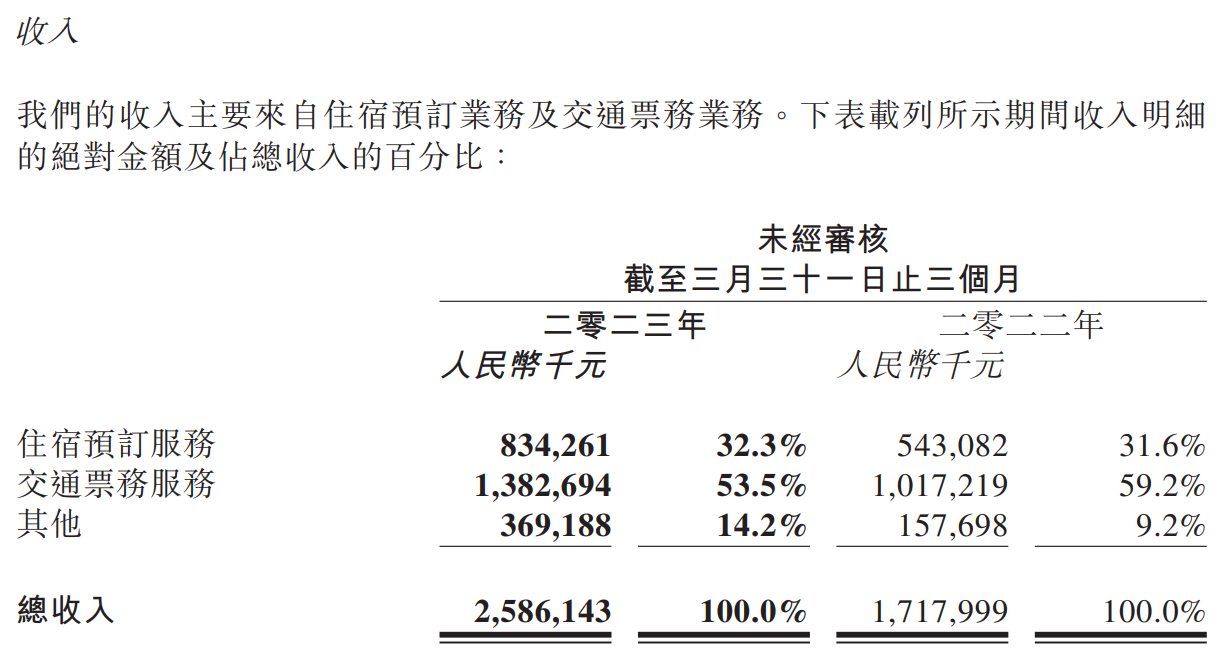

2. 住宿事業成效高:2019Q1時,同程住宿預訂服務收入僅有交通票務收入的39%,本季同程住宿預訂服務收入8.3億人民幣,已達交通票務收入的60%,這是疫情間同程最突出的改變。而Q1的其他收入已達3.7億人民幣,是2019年同期的10倍以上,這部分涵蓋了廣告、酒店管理與景點門票等收入。

3. 低單價用戶群廣:同程近年大力推展火車票、汽車票這類低單價的交通產品,以增加獲客與用戶覆蓋,Q1平均月付費用戶Q1已達4,140萬人,較2019年同期增長79%。從客單價看,2019Q1每個月付費用戶產生的交易額為520元人民幣,產生的收入為26元;而在2023Q1對應的交易額與收入則分別為461元與21元;雖然與2019年相比分別下降12%與20%,倒不算嚴重,這些用戶可視為同程的資產。

4. 行銷投入轉化率是關鍵:若將2019Q1與本季的損益表對比,可以發現在收入增長45%的基礎上,本季研發與行政的費用甚至比2019年低,降本的能力很突出;而本季行銷費用9.7億人民幣則比2019年同期增長106%,是增速最大的部份;在微信小程序之外的新通路是否能有好結果,應該是決定同程在後疫情能否新爆發力的關鍵。

----------

Tongcheng Travel (HK: 0780) releases its Q1 2023 financial results. Both the Q1 GMV and adjusted EBITDA have set new historical highs. Multiple operational metrics have significantly improved compared to the same period in 2019. In recent years, Tongcheng has invested significantly in expanding channels beyond WeChat mini programs. Whether these investments can be exchanged for outbound travel revenue might be key to Tongcheng's potential future growth. Here are some viewpoints from Haize Capital:

1. Financial performance sets a new historical record: Tongcheng's total GMV for this quarter was 57.2 billion RMB, an increase of 77% YoY and a 59% growth compared to the same period in 2019. The adjusted EBITDA was 730 million RMB, a YoY increase of 67% and a 19% growth from the same period in 2019. The fact that Tongcheng can set a new profit record with just domestic business in China represents an important milestone in this period.

2. Excellent in accommodation business: In Q1 2019, Tongcheng's hotel booking revenue was only 39% that of ticketing. This quarter, the hotel booking revenue reached 830 million RMB, representing 60% of ticketing revenue. This is the most notable change for Tongcheng during the pandemic. Moreover, other revenue in Q1 has reached 370 million RMB, more than 10 times that of the same period in 2019, including revenue from advertising, hotel management, and attraction ticket sales.

3. Wide range of user groups with low ATV(Average Transaction Value): Tongcheng has been vigorously promoting low-priced transportation products such as train and bus tickets in recent years to increase customer acquisition and user coverage. The average number of monthly paying users in Q1 has reached 41.4 million, an increase of 79% compared to the same period in 2019. In terms of ATV, the transaction volume generated by each monthly paying user was 520 RMB in Q1 2019, generating revenue of 26 RMB. In Q1 2023, the corresponding transaction volume and revenue were 461 RMB and 21 RMB respectively; although these figures represent a decrease of 12% and 20% respectively compared to 2019, the decrease is not severe, and these users can be considered as assets for Tongcheng.

4. Conversion rate of marketing investment is key: Comparing the income statement for Q1 2019 with this quarter, we can see that despite a 45% increase in revenue, the costs for research and administration this quarter are even lower than in 2019, demonstrating high efficiency of cutting costs. Meanwhile, the marketing expenses for this quarter were 970 million RMB, an increase of 106% compared to the same period in 2019, making it the area with the greatest growth. Whether the new channels beyond WeChat mini programs can yield good results should be a key determinant of whether Tongcheng can show new vitality post-pandemic.

----------

퉁청여행(同程旅行, HK: 0780)은 2023년 1분기 재무 실적을 발표했다. 1분기 GMV와 Adjusted EBITDA는 모두 사상 최고치를 기록했다. 2019년 같은 기간에 비해 여러 운영지표가 눈에 띄게 호전됐다. 최근 몇 년 동안 퉁청여행은 위챗 미니 프로그램 이외의 경로를 확장하는 데 대량의 자금을 투입했다. 이러한 투자가 해외여행 관련 영업수익으로 전환될 수 있을지는 퉁청여행의 미래 잠재적 성장의 관건이 될 수 있다. 다음은 하이저 캐피털의 일부 관점이다.

1. 재무 실적이 새로운 기록을 세웠다. 퉁청여행의 이번 분기 총 GMV는 572억 위엔으로 전년 동기 대비 77%, 2019년 동기 대비 59% 증가했다. Adjusted EBITDA는 7억3,000만 위엔으로 전년 동기 대비 67%, 2019년 동기 대비 19% 증가했다. 퉁청여행이 중국 국내 사업만으로 새로운 이윤 기록을 세울 수 있었던 것은 이 시기의 중요한 이정표다.

2. 숙박 사업이 뛰어나다. 2019년 1분기 퉁청여행의 호텔 예약 영업수익은 티켓 영업수익의 39%에 불과했다. 이번 분기에 호텔 예약 영업수익은 8억3,000만 위엔으로 티켓 영업수익의 60%를 차지한다. 이는 코로나 동안 퉁청여행의 가장 뚜렷한 변화다. 또한 1분기의 기타 영업수익은 3억7,000만 위엔으로 2019년 같은 기간의 10여 배에 달했으며, 광고, 호텔 관리, 관광지 입장권 판매 영업수익을 포함했다.

3. ATV(Average Transaction Value) 사용자 그룹: 퉁청여행은 최근 몇 년 동안 기차, 버스 승차권 등 저가 교통 상품을 대대적으로 보급하여 고객 획득량과 사용자 커버리지를 증가시켰다. 1분기 월평균 유료 가입자 수는 4,140만명으로 2019년 같은 기간보다 79% 증가했다. ATV의 경우 2019년 1분기 월간 유료 가입자가 발생한 거래량은 520위엔, 발생한 영업수익은 26위엔이었다. 2023년 1분기에 대응한 거래액과 영업수익은 각각 461위엔과 21위엔이다. 이 수치는 2019년에 비해 각각 12%, 20% 감소했지만 하락은 심각한 편은 아니다. 이러한 사용자는 퉁청여행의 일정 자산으로 간주될 수 있다.

4. 마케팅 투자의 전환율이 관건이다. 2019년 1분기 손익계산서와 이번 분기를 비교해보면 영업수익이 45% 증가했지만 이번 분기의 연구와 관리 원가는 2019년보다 낮아 원가를 낮추는 성과를 보였다. 이와 동시에 이번 분기의 마케팅 비용은 9억7,000만 위엔으로 2019년 같은 기간에 비해 106% 성장하여 가장 빨리 증가되였다. 위챗 미니 프로그램 이외의 새로운 경로가 좋은 효과를 낼 수 있을지는 포스트 코로나 시대 퉁청여행의 경로가 새로운 활력을 발산할 수 있을지를 결정하는 관건적인 요소일 것이다.

文章鏈接 Hyperlink:https://www.tongchengir.com/hk/investor-relations/announcements-circulars/

資料來源 Resource:Tongcheng

標籤 Label:0780 Hotel Transportation Marketing China