登錄

選單

登錄

海擇短評 Haize Comment:

中國最大網約車平台滴滴出行(OTCMKTS: DIDIY)近期公告2023Q1財報,這是滴滴自美國紐交所退市後首次公告財報。財報與滴滴本身過往相比,並不算有大幅增長,規模與Uber相比也落於下風,不過若強監管確實結束,猛虎出閘的態勢仍值得關注。海擇資本披露部分觀點如下:

1. 強監管終於結束:滴滴出行此前因為違反中國網路安全及數據風險等問題,被官方強制下架App,並由網信辦、公安部及國家安全部等七個部門進駐安全審查,歷經18個月後,終於在今年Q1重新上架App;考量到滴滴終於重新公告財報,強監管似有塵埃落定之勢。

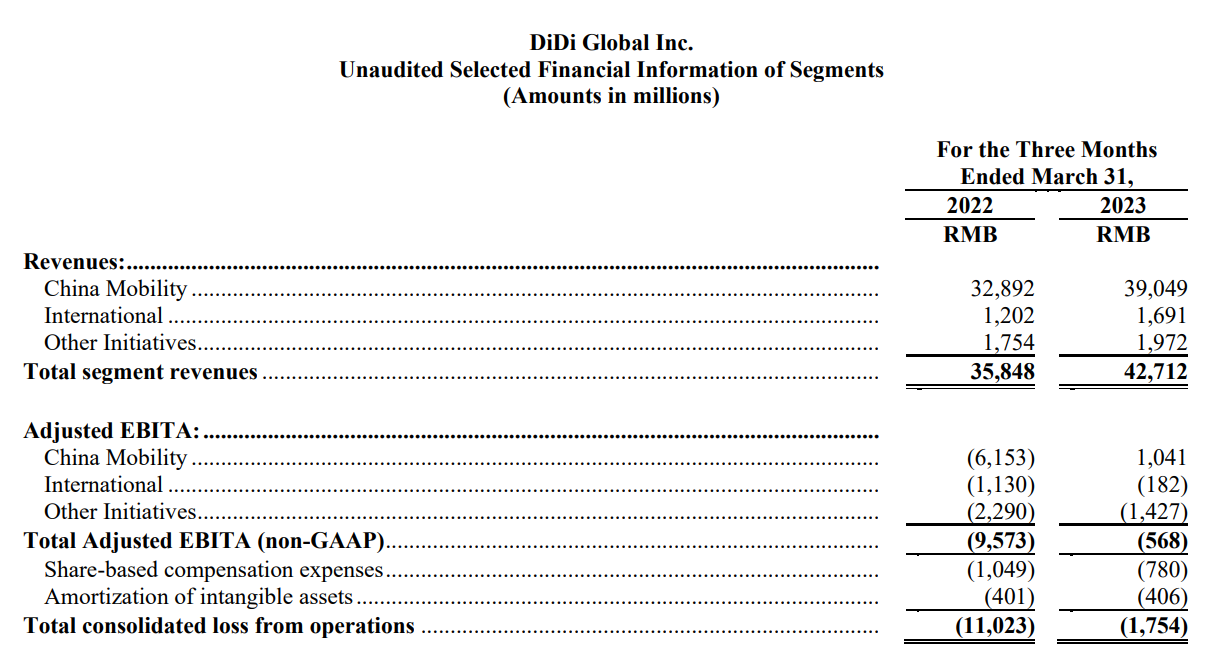

2. 網約車數據持平:滴滴本年Q1收入為427億人民幣,YoY增長19.1%,唯若與2021年IPO當年的Q1數據(422億人民幣)相比,僅增長1.2%;而Q1虧損9.1億人民幣,雖較2022年同期虧損160.7億人民幣大幅減少94.3%,唯與2021Q1相比,則轉盈為虧,當時的盈利為55億人民幣。從壞處看當然是幾年間Uber(NYSE: UBER)高歌猛進,滴滴毫無成長;但從好處看滴滴也沒有從中國網約車產業的版圖消失,仍有強大的競爭能力。

3. 國際化事業仍欠東風:滴滴的國際化在這兩年似乎不溫不火。從交易額看,滴滴的國際事業(主要在巴西與墨西哥)Q1交易額為137.5億人民幣,與其中國區網約車事業相比,已達其交易額的23.3%,規模並不小;但若從收入看,國際事業收入16.9億人民幣,僅達中國網約車事業收入的4%,這表示滴滴如果真的重視國際化,恐怕還需要更高的投入,不然就是斷然止損,以目前的投入態勢來看,國際化事業無法對集團轉盈帶來太大幫助。

4. 國際競品交易規模較大:Uber的Q1收入為88.2億美元,換算為人民幣,約比滴滴高48%,雖然雙方為相同量級,也不是滴滴能快速趕追的程度;不過若從活躍的角度看,Uber的MAPCs(Monthly Active Platform Consumers)為1.3億;滴滴本季未公告活躍數,但依2021Q1數據,滴滴在中國區的月活躍為1.56億,若以相同口徑對比,推估雙方差距不大。

----------

China's largest ride-hailing platform, DiDi Chuxing (OTCMKTS: DIDIY), recently announced its Q1 2023 earnings. This is the first financial report since DiDi's delisting from the NYSE. The report shows no significant growth compared to DiDi's own past performance, and the size is also inferior compared to Uber. However, if the strong supervision indeed ends, the situation of DiDi, like a tiger unleashed, is still worth noting. The following are some views disclosed by Haize Capital:

1. The end of strong regulation: DiDi was previously forced to remove its app due to violations of China's internet security and data risk issues, and seven departments, including the Cyberspace Administration, the Ministry of Public Security, and the National Security Department, conducted a security review. After 18 months, the app was finally relisted in Q1 of this year. Considering that DiDi has finally announced its financial report again, it seems that the era of strong regulation may have settled.

2. The performance is steady: DiDi's Q1 revenue this year was 42.7 billion RMB, a YoY increase of 19.1%. However, compared with the 42.2 billion RMB in Q1 2021 (the year of IPO), it only increased by 1.2%. The Q1 loss was 910 million RMB, which is a significant decrease of 94.3% compared to the loss of 16.07 billion RMB in Q1 2022. But compared to Q1 2021, it turned from a profit of 5.5 billion RMB into a loss. On the downside, of course, Uber (NYSE: UBER) has been making great strides over the years, while DiDi has seen no growth. But on the upside, DiDi has not disappeared from the map of China's ride-hailing industry and still has strong competitive power.

3. Global business still lacks momentum: DiDi's internationalization seems lukewarm in the past two years. The GMV of DiDi's international business (mainly in Brazil and Mexico) in Q1 was 13.75 billion RMB, representing 23.3% that of its ride-hailing business in China, the size is not small. However, the revenue of the global business was 1.69 billion RMB, only 4% that of in China. This implies that if DiDi really values internationalization, it might need more investment, otherwise it should cut its losses decisively. As it stands, the current level of investment in the international business seems having little help to the group's return to profitability.

4. International competitor has a larger transaction volume: Uber's Q1 revenue was $8.82 billion, which converted into RMB is about 48% higher than DiDi's. Even though they are of the same order of magnitude, it's not a gap that DiDi can quickly close. However, in terms of active users, Uber's MAPCs (Monthly Active Platform Consumers) stand at 130 million, DiDi did not announce the number of active users for this quarter, but according to the data from Q1 of 2021, DiDi's monthly active users in China was 156 million. If we compare them on the same basis, it is estimated that the gap between the two is not significant.

----------

중국 최대 온라인 차량 예약 플랫폼인 디디추싱(滴滴出行, OTCMKTS: DIDIY)은 최근 2023년 1분기 실적을 발표했다. 이것은 디디가 뉴욕증권거래소에서 상장폐지된 이래 발표한 첫 재무보고서이다. 보고서에 따르면 디디 자신의 과거 실적에 비해 성장이 뚜렷하지 않고 규모도 우버보다 못하다. 그러나 강한 규제가 실제로 끝난다면 디디는 '맹호가 수문을 나서는'것처럼 여전히 주목할 만하다. 다음은 하이저 캐피털이 공개한 일부 관점이다.

1.강한 감독관리 종료함: 디디는 이전에 중국의 인터넷 안전과 데이터 위험 문제를 위반하여 어쩔 수 없이 그 응용을 하차했다. 인터넷정보사무실, 공안부, 국가안전부 등 7개 부문은 그에 대해 안전심사를 진행했다. 18개월 후, 이 앱은 마침내 올해 1분기에 다시 출시되었다. 강한 규제는 디디가 재무제보를 다시 발표함에 따라 끝난 것 같다.

2.평범한 실적: 디디의 올해 1분기 수입은 427억 위안으로 전년 동기 대비 19.1% 증가했다. 그러나 2021년 1분기(IPO 당시) 422억 위안과 비교하면 1.2% 늘어나는 데 그쳤다. 1분기 적자는 9억1,000만 위안으로 2022년 1분기 적자 160억7,000천만 위안보다 94.3% 대폭 줄었다. 그러나 2021년 1분기와 비교하면 55억 위안의 이익에서 적자로 돌아섰다. 물론 불리한 점은 우버(NYSE: UBER)의 실적이 수년간 성큼성큼 나아갔지만 디디는 성장하지 못했다는 점이다. 그러나 좋은 면에서 볼 때 디디는 중국 인터넷 차량예약업의 판도에서 사라지지 않고 여전히 강대한 경쟁력을 갖고있다.

3.글로벌 사업은 여전히 동력이 부족함: 디디의 국제화는 지난 2년 동안 미온적인 것 같다. 디디의 1분기 국제사업(주로 브라질과 멕시코) GMV는 137억5,000만 위안으로 국내 온라인 차량 예약 사업의 23.3%를 차지해 규모가 작지 않다. 그러나 국제사업 수익은 16억9,000만 위안으로 중국 시장 실적의 4%에 불과하다. 이것은 만약 디디가 정말 국제화를 중시한다면, 그것은 더 많은 투입을 필요로 할 수도 있고, 그렇지 않으면 그것은 과감하게 손실을 멈춰야 한다는 것을 의미한다. 현재 상황으로 볼 때, 국제 사업의 투자 수준은 그 그룹의 수익 회복에 그다지 도움이 되지 않는 것 같다.

4.국제 경쟁사의 거래량이 더 큼: 우버의 1분기 수입은 88억2,000만 달러로 위안화로 환산하면 디디보다 약 48% 높다. 비록 그것들은 규모에서 같지만, 이것은 디디가 신속하게 메울 수 있는 차이가 아니다. 그러나 사용자 활동도는 우버의 MAPCs(Monthly Active Platform Consumers)가 1억3,000만 명이고, 디디는 이번 분기의 활성 사용자 수를 발표하지 않았지만, 2021년 1분기에 따르면 디디의 중국 내 월간 활성 사용자는 1억5,600만 명이다. 만약 우리가 같은 기초에서 그것들을 비교한다면 량자간의 격차는 그리 뚜렷하지 않을 것이다.

文章鏈接 Hyperlink:https://ir.didiglobal.com/financials/sec-filings/default.aspx

資料來源 Resource:Didi

標籤 Label:Didi DIDIY Ride-hailing Regulation