登錄

選單

登錄

海擇短評 Haize Comment:

國際GDS公司Sabre(NASDAQ: SABR)近期公告大幅優於預期的2023Q2財報,同時也對Q3、Q4財測給到正面預期,股市市值單日大漲33%。海擇資本分析公司財報部分亮點如下:

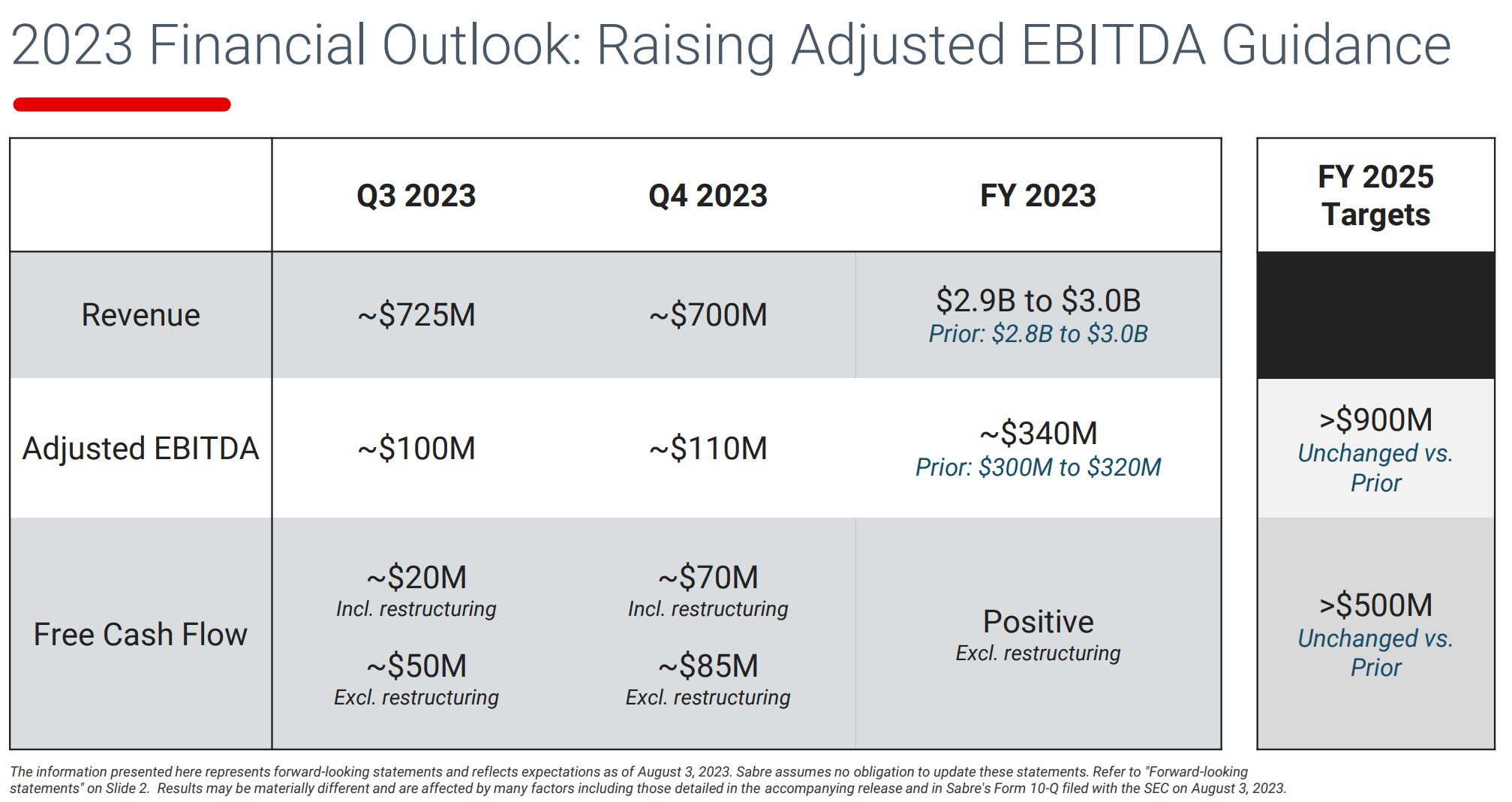

1. 財報大幅增強投資人信心:相對原有Adjusted EBITDA為4,500萬,實際公告的結算為7,305萬,較預期高出62%。同時也重申Q3與Q4財測分別為1億美元與1.1億美元,在Q2財報超乎預期後,下半年的財測看來也較為可信。

2. 住宿事業虧轉盈:Sabre的住宿事業本期宣告單獨結算後的Adjusted EBITDA為150萬美元,首次虧轉盈。從規模看,其實該事業仍然不大,本季收入7,667萬美元僅比2019年同期增長4%,約佔集團整體收入的10%,只能說已具有自負盈虧的能力。

3. 運營最大難題在於利息支出:一間季度收入7.4億美元,Adjusted EBITDA能賺7,300萬的公司,是怎麼做到虧損1.3億美元,淨損率為17.5%的?最核心的原因是歷經疫情,Sabre身上掛著太多的負債,Q2的利息支出就有1.06億。按財報海擇資本推算2023全年利息費用為3.75 億美元,就算Adjusted EBITDA如更新財測達到3.40億美金,GAAP角度的結算仍然會是虧損。

4. 市值增長的三大挑戰:Sabre目前市值約16億美元,今年Adjusted EBITDA預期3.4億,2025年預期9億,從EBITDA本益比的角度看當然非常便宜;GDS行業算是微利,航空公司用戶的進入門檻又很高,這都是Sabre在後疫情時間的優勢。

不過,投資人期待的終歸還是GAAP下能盈利,Sabre的最終挑戰在於三點,其一,隨著原有CB不斷到期,好處是不用再支付優先股股息,但壞處是優先股轉換為普通股後,股本會快速膨脹,比如Q3的9月1日起,股本會一次增加4,700萬股,接下來幾年股本不斷膨脹後,公司就顯得沒那麼便宜了;其二,公司派發的股期權也不反映在EBITDA中,從2023年財報看,已沒有如同2022年大幅增列的現象,未來尚待觀察;其三,由於GDS行業本身微利,盈利終歸還是要多產品線與規模效應,Sabre在Q3輸送旅客數1.72億,已達2019年同期的96%,但收入7.4億美金只有2019年同期的74%,產品結構仍需優化。

----------

GDS operator Sabre (NASDAQ: SABR) announces its Q2 2023 financial results, significantly outperforming expectations, and also released positive forecasts for Q3 and Q4, with stock market value soaring 33% in a single day. The insights by Haize Capital are as follows:

1. Financial results greatly boost investor confidence: The original Adjusted EBITDA was $45 million, while the actual announced settlement was $73.05 million, 62% higher than expected. The company also reaffirmed its Q3 and Q4 financial forecasts at $100 million and $110 million, respectively. Given that the Q2 financial report exceeded expectations, the financial forecasts for the second half of the year appear to be credible.

2. Accommodation Business Turns Profitable: Sabre's accommodation business announced a stand-alone Adjusted EBITDA of $1.5 million for this period, turning profitable for the first time. In terms of size, this business is still not substantial. The revenue for this quarter of $76.67 million represents a mere 4% growth compared to the same period in 2019, accounting for approximately 10% of the group's overall revenue. It can only be said that the business now has the ability to sustain itself financially.

3. The Biggest Operational Challenge Lies in Interest Expenses: How does a company with quarterly revenue of $740 million and Adjusted EBITDA of $73 million incur a loss of $130 million, with a net loss rate of 17.5%? The core reason is that, after going through the pandemic, Sabre is burdened with heavy debt, with Q2 interest expenses alone amounting to $106 million. Based on the financial report, Haize Capital estimates that the total interest expense for 2023 will be $375 million. Even if the Adjusted EBITDA could reach the updated forecast of $340 million, the settlement from a GAAP perspective will still be a loss.

4. Three Major Challenges to Market Value Growth: Sabre's current market value is around $1.6 billion, with an expected Adjusted EBITDA of $340 million this year and $900 million expected in 2025. From an EBITDA P/E ratio perspective, it certainly appears very cheap; the GDS industry has slim margins, and the entry threshold for airline customers is high, both of which are advantages for Sabre in the post-pandemic period. However, what investors ultimately expect is profitability under GAAP. Sabre's final challenges lie in three areas:

a. As the CBs (Convertible Bonds) continue to mature, although there's no need to pay preferred stock dividends anymore, the rapid conversion of preferred stocks into common stocks will cause rapid dilution of equity. For example, starting on September 1, the capital will increase by 47 million shares at once, and after continuous expansion over the next few years, the company will not be cheap anymore.

b. The stock options distributed by the company are not reflected in EBITDA, it remains to be observed in the future .

c. Because the GDS industry itself has slim margins, profitability ultimately requires multiple product lines and scale effects. Sabre's number of passengers transported in Q3 was 172 million, reaching 96% of the same period in 2019, but the revenue of $740 million was only 74% of the same period in 2019. The product structure still needs optimization.

----------

GDS 사업자인 Sabre(NASDAQ: SABR)는 2023년 2분기 재무 실적을 발표했다. 실적이 예상을 현저히 상회하다. 그리고 Sabre는 3분기와 4분기에 대한 전망을 발표했다. 주식 시가가 하루 만에 33% 크게 올랐다. 하이저 캐피털의 견해는 다음과 같다.

1. 재무 실적은 투자자들의 신뢰를 크게 진작시켰다. Adjusted EBITDA는 4,500만 달러였으나 실제 결제된 금액은 7,305만 달러로 예상보다 62% 많았다. 이 회사는 또한 3분기와 4분기 재무 전망을 각각 1억 달러와 1억1,000만 달러로 재확인했다. 2분기 재무실적이 전망을 뛰어넘었다는 점을 감안하면 하반기의 실적 전망은 신뢰할 수 있는 것으로 보인다.

2. 숙박사업이 흑자로 돌아섰다. Sabre의 숙박 사업은 이 분기의 Adjusted EBITDA가 150만 달러로 처음으로 흑자로 돌아섰다고 발표했다. 규모로 말하자면, 이 사업은 아직 크지 않다. 이번 분기의 영업수익은 7,667만 달러로 2019년 동기 대비 4% 증가에 그쳐 그룹 총영업수익의 약 10%를 차지했다. 이 회사는 지금 손익을 스스로 책임질 능력이 있다고 말할 수밖에 없다.

3. 운영의 가장 큰 어려움은 이자 지출이다. 분기 매출액이 7억4,000만 달러, Adjusted EBITDA가 7,300만 달러인 한 회사가 어떻게 1억3,000만 달러의 손실과 순손실률이 17.5%에 달할 수 있겠는가? 코로나 사태를 겪은 뒤 Sabre는 2분기 이자 지출만 1억600만 달러에 달할 정도로 큰 빚을 지고 있기 때문이다. 재무보고서에 따르면 하이저 캐피털은 2023년 이자 지출 총액이 3억7,500만 달러에 이를 것으로 전망했다. Adjusted EBITDA가 예측 된 3억4,000만 달러에 도달 할 수 있다 하더라도 GAAP 관점에서 결제 금액은 여전히 손실이 될 것이다.

4. 시장가치 성장의 세 가지 도전: Sabre의 현재 시가총액은 약 16억달러이며, 올해 Adjusted EBITDA는 3억4,000만달러, 2025년에는 9억달러로 예상된다. EBITDA 수익률의 관점에서 볼 때, 현재의 시가 평가액은 분명히 낮은 편이다. GDS 업계는 이윤이 적고 항공사 사용자의 진입 문턱도 높다. 이 두 가지 모두 포스트 코로나 시기에 Sabre의 장점이다. 그러나 투자자들이 궁극적으로 기대하는 것은 GAAP에서의 수익성이다. Sabre의 과제는 다음과 같은 세 가지다.

첫째, 전환사채가 계속 만기가 도래함에 따라 우선주 배당금을 더 이상 지급할 필요가 없지만 우선주를 보통주로 빠르게 전환하면 지분이 빠르게 희석될 수 있다. 예를 들어, 9월 1일부터 회사는 4,700만 주를 한꺼번에 증자할 것이며, 향후 몇 년 동안 지속적인 확장을 거쳐 이 회사의 주가는 더 이상 싸지 않을 것이다.

둘째, 회사가 배정한 스톡옵션은 EBITDA에 반영되지 않았으며 앞으로 지켜봐야 한다.

셋째, GDS 업계 자체의 이윤이 적기 때문에 이윤은 최종적으로 여러 제품 라인과 규모 효과가 필요하다. Sabre의 3분기 여객 수송량은 1억7,200만명으로 2019년 같은 기간의 96%에 달했지만, 7억4,000만달러의 영업수익은 2019년 같은 기간의 74%에 그쳤다. 제품 구조는 여전히 최적화되어야 한다.

文章鏈接 Hyperlink:https://investors.sabre.com/events-%26-presentations

資料來源 Resource:Sabre

標籤 Label:GDS SABR Amadeus Airlines Debt