登錄

選單

登錄

海擇短評 Haize Comment:

Airbnb(NASDAQ: ABNB)近期公告2023Q2財報,核心財務數據創下歷史次高,成績斐然。IPO兩年半以來,Airbnb基於與Booking的錯位競爭戰略,圍繞非標住宿完善用戶體驗,取得與Booking相同量級的市值;往好處看是在住宿的子領域築牆積量,Booking(NASDAQ: BKNG)在非標領域一季能有近億間夜量,竟也無法影響Airbnb的盈利能力;往壞處看,IPO已近三年,仍缺乏第二增長曲線,也無法縮短與Booking的距離,活動體驗市場全球火熱,但Airbnb在供給面仍然沒有新突破。如果Airbnb的財務數據都是Booking的一半,而雙方市值相同,長期來看,如果不是Booking市值往上,就是Airbnb要往下。海擇資本對季報的部分總結如下:

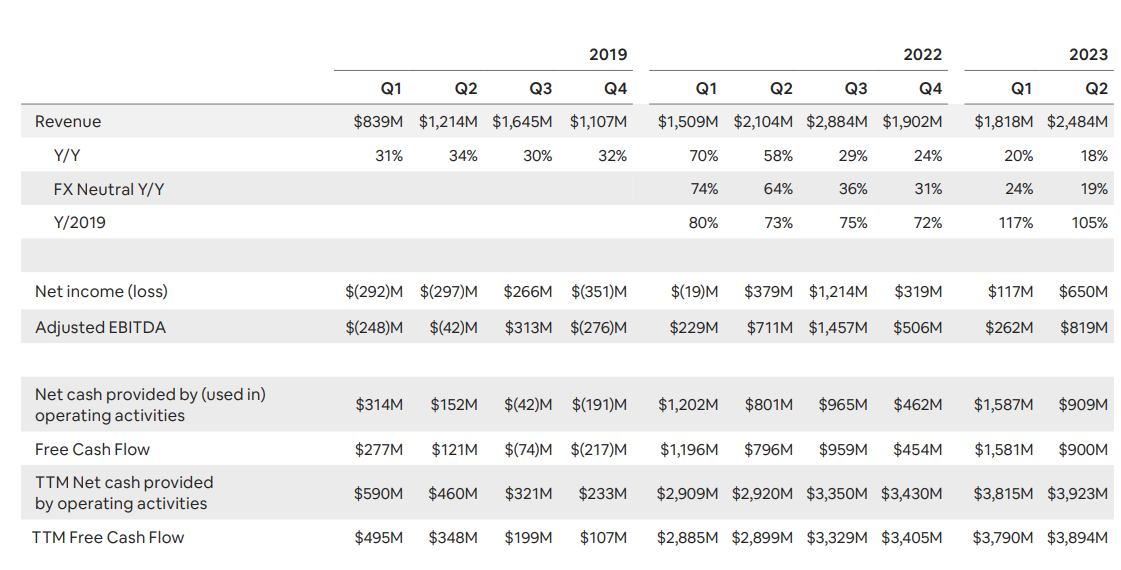

1. 核心財務創歷史次高:Airbnb本季交易額191.8億美元、收入24.8億美元、間夜量1.15億,三項數據YoY增速都超過10%且創歷史次高;其中亞太地區訂單交易額YoY增長超80%,遠高於平均值。公司Q2收入YoY增速18%,對Q3的收入預期則給到14%-18%。

2. 從供給面優化體驗:本季新增房源數YoY增長19%,季末活躍房源(1年內曾交易過至少1次)總數超過700萬套;從房源定位看,城市目的地增長20%,而度假目的地增長19%,基本一致。在當前弱經濟時代,公司認為服務不斷增加的價格敏感型客戶會是重點,並說明了方向--"如果我們生活在Airbnb價格不上漲而酒店價格繼續上漲的世界,Airbnb相對於酒店會變得更便宜,而酒店龐大的受眾群體都是Airbnb的潛在用戶(if we live in a world where Airbnb prices do not go up and the even remain flat or stable and hotels continue to rise, then Airbnb continues to become more affordable relative to hotels, which are still much larger audience than Airbnb)"。考慮到Airbnb中90%的房東是個人,它的方向有可能執行成功。

3. 對生成式AI觀點不同:相對於同業主要將生成式AI用於Chat Robot式的行程規劃,Chesky認為生成式AI在Airbnb的使用界面不應是聊天(Chat),應該是能結合文本、圖像與視訊的多重界面,且應該要能結合消費者與業主的過往經驗,並結合當地政策與時令現況做到推薦。Chesky並沒有就開發現況給到時間表。

4. 新市場仍集中於住宿:公司說明已對超過30天的長租產品提高開發優先級,認為這部分市場潛力一年有1億間夜,並促使業主將月租折扣從22%提升至50%。但對活動體驗產品供給面的開發,公司並未說明進度,僅強調95%用戶對體驗產品給到五星評價,我們認為Airbnb是被自己過往的完美綁住了。

----------

Airbnb (NASDAQ: ABNB) announced its 2023 Q2 financial results, with core figures reaching a historical second high, which is impressive. In the two and a half years since its IPO, Airbnb has achieved a market value on par with Booking through its dislocation competition strategy with Booking, focusing on improving user experience around alternative accommodations. On the positive side, Airbnb has achieved much in the field of alternative accommodation, and Booking (NASDAQ: BKNG), with nearly a hundred million alternative room nights this quarter, still can't impact Airbnb's profitability. On the negative side, nearly three years after its IPO, Airbnb still lacks a second growth curve and has been unable to close the gap with Booking. The market for experience/activity is booming globally, but Airbnb has not yet made new breakthroughs on the supply side. If Airbnb's financial data is half that of Booking's, and both have the same market value, in the long term, Booking's market value will go up, or Airbnb will go down. Haize Capital's summary of the quarterly report is as follows:

1. Core Financial Figures Reach Historical Second High: With a GMV of $19.18 billion, revenue of $2.48 billion, and room nights of 115 million this quarter, the three figures of Airbnb grew by more than 10% YoY, reaching a historical second high. Among them, the GMV from the Asia-Pacific region grew by over 80% YoY, far higher than the average. The company's Q2 revenue grew at a YoY rate of 18%, and the revenue guidance for Q3 is given at 14% to 18%.

2. User Experience Optimization from the Supply Side: The number of new listings this quarter grew by 19% YoY, and the total number of active listings (those traded at least once within a year) exceeded 7 million. In terms of geographic distribution of listings, urban destinations grew by 20%, while vacation destinations grew by 19%, roughly consistent. In the current weak economic era, the company believes that serving the increasing price-sensitive users will be a focus and explained the direction – "if we live in a world where Airbnb prices do not go up and even remain flat or stable, and hotels continue to rise, then Airbnb continues to become more affordable relative to hotels, which are still a much larger audience than Airbnb." Considering that 90% of hosts on Airbnb are individuals, this direction could potentially be successfully executed.

3. A Different Perspective on Generative AI: Unlike competitors who primarily use generative AI for chat robot-style trip planning, Chesky believes that the use of generative AI in Airbnb's user interface should not be confined to chat. Instead, it should be a multi-faceted interface that can combine text, images, and video, and should be able to integrate the past experiences of consumers and hosts, along with local policies and current conditions, to make recommendations. Chesky did not indicate a timeline for development.

4. New Market Still Concentrated on Accommodation: The company explained that it has raised the development priority for long-term rental products exceeding 30 days, believing that this segment has the potential for 100 million room nights per year, and encouraging hosts to increase monthly rental discounts from 22% to 50%. However, the company did not provide details on the progress of experience products, only emphasizing that 95% of users gave a five-star rating to experiences/activities. Perhaps Airbnb is constrained by its own past perfection.

----------

에어비앤비(Airbnb, NASDAQ: ABNB)는 2023년 2분기 재무실적을 발표했다. 핵심 데이터가 역대 두 번째로 기록한 것은 인상적이다. IPO가 된지 2년 반이 지난 Airbnb는 Booking과의 다른 경쟁 전략을 통해 비표준 숙박에 대한 사용자의 경험을 개선하는 데 집중하여 Booking과 비슷한 시가총액을 달성했다. 긍정적인 측면에서는 에어비앤비가 비표준 숙박 분야에서 큰 성과를 거둔 반면 부킹(Booking, NASDAQ: BKNG)은 이번 분기 비표준 숙박의 총 객실 이용 박수가 1억 개에 육박했지만 여전히 에어비앤비의 수익성에 영향을 미치지 못하고 있다. 부정적으로 볼 때, IPO가 된지 거의 3년이 지난 후에도 Airbnb는 Booking과의 격차를 좁힐 수없는 두 번째 성장 곡선이 부족하다. 체험/행사 시장은 전 세계적으로 왕성하게 발전하고 있지만 Airbnb는 아직 공급 방면에서 새로운 돌파를 이루지 못했다. 만약 Airbnb의 실적이 Booking의 절반이고 양자의 시가총액이 같다면 장기적으로 Booking의 시가총액은 상승하고 Airbnb의 시가총액은 하락할 것이다. 하이저 캐피털의 이번 분기 보고서에 대한 분석하고 요약은 다음과 같다.

1. 핵심 재무 데이터는 역사상 두 번째로 달했다. 이번 분기에 에어비앤비의 GMV는 191억8,000만 달러, 영업수익은 24억8,000만 달러, 총 객실 이용 박수는 1억1,500만 달러였다. 이 세 가지 수치는 전년 동기 대비 10% 이상 증가하여 사상 두 번째로 달했다. 그 중 아시아 태평양 지역의 GMV는 전년 대비 80% 이상 증가하여 평균보다 훨씬 높았다. 이 회사의 2분기 영업수익은 전년 동기 대비 18% 증가했고, 3분기 영업수익은 14%~18%로 예상됐다.

2.공급의 사용자 경험을 최적화한다. 이번 분기의 신규 주택 수는 전년 동기 대비 19% 증가했고, 활성 주택(1년 내에 적어도 한 번 거래된 주택) 총수는 700만 채를 넘었다. 주택원천의 지리적분포로 볼 때 도시목적지는 20% 늘어났고 휴가목적지는 19% 늘어났는데 량자는 기본적으로 일치했다.현재 경제가 부진한 시대에, 이 회사는 날로 증가하는 가격에 민감한 사용자에게 서비스를 제공하는 것이 중점이 될 것이라고 생각하고, 그 방향을 설명했다. '만약 우리가 Airbnb의 가격이 오르지 않지만 호텔 가격이 계속 오른 세계에 살다면 Airbnb의 가격은 계속 호텔 가격보다 더 실속있게 쌀 것이고, 호텔의 방대한 고객들은 여전히 Airbnb의 잠재적 사용자이다(if we live in a world where Airbnb prices do not go up and the even remain flat or stable and hotels continue to rise, then Airbnb continues to become more affordable relative to hotels, which are still much larger audience than Airbnb).' Airbnb의 집주인의 90%가 개인이라는 점을 고려하면 이 방향은 성공할 수 있을 것이다.

3. 생성식 인공지능에 대한 다른 견해: 동종업계의 경쟁사들이 주로 생성식 인공지능을 챗봇식의 여행 계획에 사용하는 것과 달리, Chesky는 Airbnb의 사용자 인터페이스에서 생성식 인공지능을 사용하는 것은 챗(Chat)에 국한되어서는 안 된다고 생각한다. 반면 문자, 이미지, 동영상을 결합할 수 있는 다중 인터페이스여야 하며, 소비자와 집주인의 과거 경험, 그리고 현지의 정책과 현황을 통합하여 여행에 대해 건의할 수 있어야 한다. Chesky는 이 제품 개발 일정을 제시하지 않았다.

4. 새로운 시장은 여전히 숙박에 집중되어 있다. 이 회사는 30일이 넘는 장기 임대상품에 대한 개발 우선순위를 높였으며, 이 세분화된 시장이 연간 1억 개의 객실 이용 박수를 보유할 잠재력이 있다고 보고 집주인에게 월세 할인을 22%에서 50%로 높이도록 독려했다고 설명했다. 이 회사는 체험 제품의 진전에 대한 세부 사항을 제공하지 않았다. 그러나 이 회사는 95%의 사용자가 체험/활동 제품에 대해 5성 평가를 내렸다고 강조했다. 우리는 Airbnb이 자신의 과거의 완벽한 제품 이미지에 의해 제한되었다고 생각한다.

文章鏈接 Hyperlink:https://investors.airbnb.com/home/default.aspx

資料來源 Resource:Airbnb

標籤 Label:ABNB Airbnb BKNG EXPE Vrbo Alternative Experiences