登錄

選單

登錄

海擇短評 Haize Comment:

挪威郵輪集團(NYSE: NCLH)近期公告2023Q2財報,本季國際郵輪集團都迎接了疫情以來最好的一季,挪威郵輪也不例外。

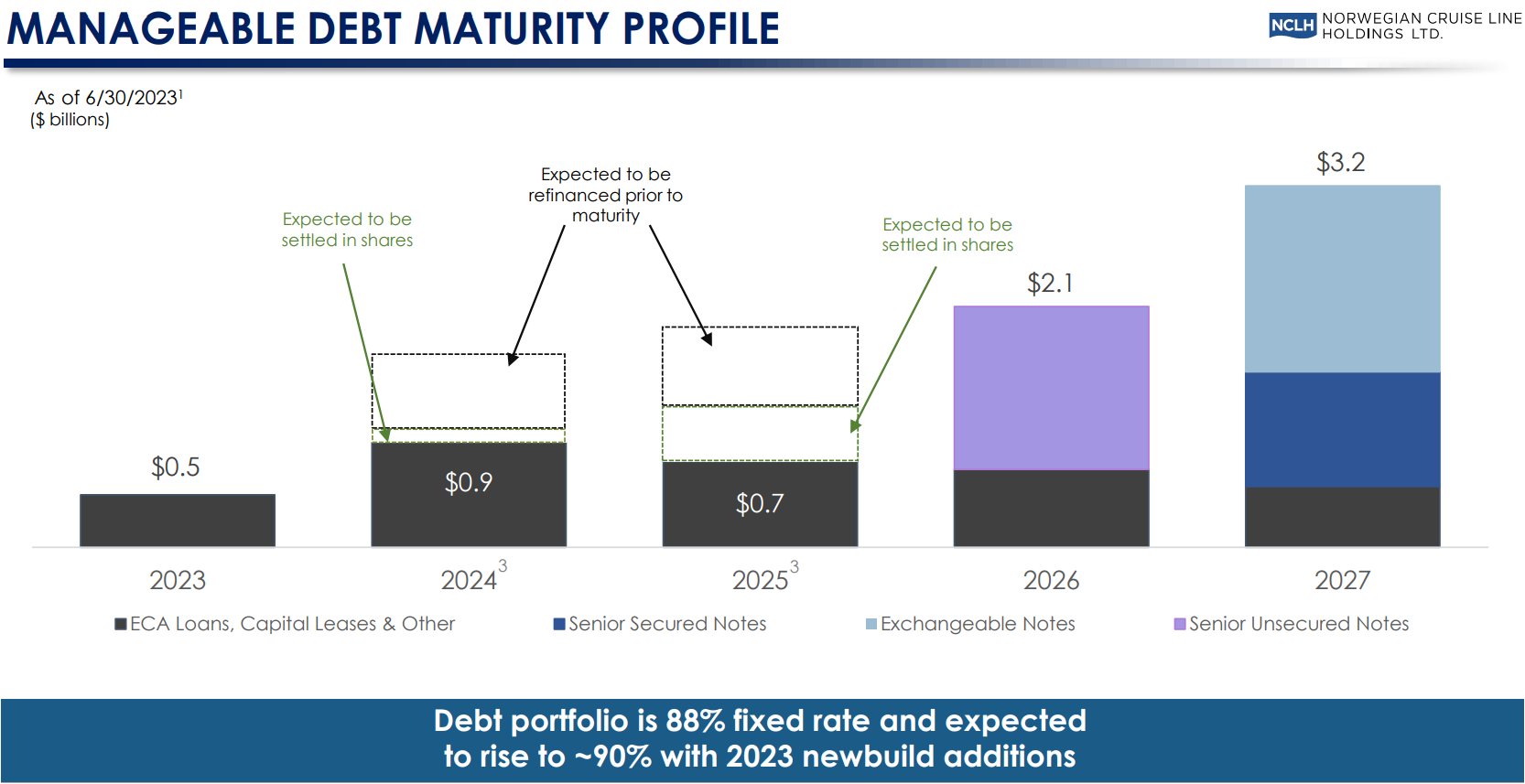

挪威郵輪本季共輸送旅客69.3萬人次,較2019年同期略高1.6%;Adjusted EBITDA為5.15億美元,是疫情後首次轉盈,也首次超過2019年同期(4.97億美元)。不過,如同此前在海擇觀點提過的,由於EBITDA不須計入因債務所需支出的利息,對當前的郵輪公司來說,EBITDA並不能真正反映運營現況,一間Adjusted EBITDA創新高的公司也完全可能因為無法支付龐大利息而陷於虧損;從淨利的角度來看會更為真實,而挪威郵輪本季淨利為8,612萬美元,低於2019年同期的2.4億美元。在同業之中,挪威郵輪的表現已經算很不錯,可做為參照的同業--嘉年華郵輪集團(NYSE: CCL),本季收入為49.1億美元,也略高於2019年同期的48.4億美元,但本季虧損4.1億美元,大幅低於2019年同期的盈利4.5億美元,中間主要差異就在於本季多了5.4億美元的利息支出,說嘉年華是幫銀行團打工也不為過。

相對於其他旅遊品類的上市公司,郵輪公司似乎更喜歡在財報公告前,遊走證交法的灰色地帶,用媒體資源強調各項財務數據的突破,但往往最後公告的財報又是另一個不同樣貌,因此導致投資人看預期時信心滿滿,但是財報結算時發現又是大額虧損的窘境。其實,只要關注好負債規模與燃油價格變動,郵輪公司的收入相對OTA與傳統旅行社更好判定。一般郵輪公司都會有較大量的超過50%的提前預訂訂單(挪威郵輪Q2有70%的訂單來自於銷售2024年和2025年的船票),這會導致一年後的艙位通常會有超過50%已提前預售(挪威郵輪Q2為60%),這表示郵輪公司對訂單的能見度會比其他旅游品類更高。因此,只要將銷售船票數、運力座位數、債務與其他數字建模,就可以大致判斷未來收入的上下限,而郵輪公司喜歡提前透露的習慣可以協助投資人下判斷。以挪威郵輪集團本季財報為例,海擇資本分享部分判斷收入與費用的經驗如下:

1. 收入= 輸送總旅客數 X 人均航行天數 X 每日均價 :這部分也可以用"船隻總艙房數 X 2 X 入住率 X 90 X 每日均價"推算,端看郵輪公司喜歡對投行提前公告哪些數據。由於郵輪只會先行透露有利數據,對於其他"忘記"的數據,就需要自行調研評估。比如郵輪公司會提到船票單價比2019年同期高40%、入住率100%、但可能會忘記提所控有的運力(郵輪總船隻數)已比2019年少了不少。

2. 最需注意的費用是負債:同樣的,公司在預期可能會提到EBITDA再創歷史新高,但是忘記提下季所必須償還的利息規模、本金數額以及債轉股對股本的稀釋;要償還的利息與本金會影響淨利高低,而股本稀釋則會影響本益比,兩者都會衝擊投資價值。疫情以來,公司也常說明員工數比2019年更精簡、食材運用比2019年更有效率、建立更多直銷渠道以減少廣告投放與通路分成費用,但考慮到各項成本/費用都在通膨,人力薪資、食材、媒體投放無一不是如此,實際上費用結算要比2019年低,都是非常困難的事。

----------

Norwegian Cruise Line Holdings (NYSE: NCLH) released its 2023 Q2 financial results, this has been the best quarter for cruise lines since the outbreak of the pandemic, with Norwegian Cruise Line being no exception.

Norwegian Cruise Line carried a total of 693,000 passengers this quarter, a slight increase of 1.6% compared to the same period in 2019; Adjusted EBITDA was $515 million, marking the first profit since the pandemic, and also exceeding the same period in 2019 ($497 million). However, as previously mentioned in the Haize Comment, net profit is more reflective of the true operating condition than EBITDA as the latter does not consider debt interest. Norwegian Cruise Line's net profit this quarter was $86.12 million, lower than the $240 million in the same period in 2019. Among its peers, Norwegian Cruise Line's performance has been quite good. A comparable peer -- Carnival Cruise Line Group (NYSE: CCL) -- had a revenue of $4.91 billion this quarter, slightly higher than the $4.84 billion in the same period in 2019, but had a loss of $410 million, significantly lower than the profit of $450 million in the same period in 2019, the main difference lies in the additional interest expenditure of $540 million this quarter. No wonder someone says that Carnival is practically working for banking groups.

In fact, by simply paying attention to the debt size and fluctuations in fuel prices, the revenue of cruise companies can be more easily calculated compared to OTAs and traditional travel agencies. Generally, cruise companies have a large number of advance bookings exceeding 50% (Norwegian Cruise Line had 70% of bookings for Q2 from the sale of tickets for 2024 and 2025), which leads to more than 50% of cabin space typically pre-sold a year in advance (60% for Norwegian Cruise Line in Q2). This means that cruise companies have higher visibility on bookings compared to other tourism products. Therefore, with ticket sales volume, seating capacity, debt, and other figures, we can roughly calculate the upper and lower limits of future revenue, and the cruise companies' habit of revealing information in advance can assist investors in making judgments. Taking the example of Norwegian Cruise Line Holdings' quarterly financial report, Haize Capital shares some experiences in calculating revenue and expenses as follows:

1. Revenue = Total Number of Passengers x Average Travel Days per Passenger x Average Daily Price. This can also be calculated as "Total Cabin Count x 2 x Occupancy Rate x 90 x Average Daily Price," depending on which data the cruise company prefers to release to the investment bank in advance. Since cruise companies tend to disclose favorable data first, any other "forgotten" data will need to be independently researched and assessed. For instance, the cruise company may mention that the ticket price is 40% higher than the same period in 2019, and the occupancy rate is 100%, but they may "forget" to mention that their capacity (total number of cruise ships) has been reduced considerably compared to 2019.

2. The expense that needs the most attention is the liabilities. Similarly, the company may anticipate announcing that EBITDA has reached a historical high, but forget to mention the interest size to be repaid next quarter, the principal amount, and the dilution of equity due to debt conversion. The interest and principal to be repaid will affect the net profit, while equity dilution will affect the price-to-earnings ratio; both will impact the investment value. Since the pandemic, the company has often stated that the number of employees is leaner than in 2019, the ingredients transport is more efficient, and more direct sales channels have been established to reduce advertising and channel-sharing costs. However, considering that all types of costs/expenses are inflating, including human wages, ingredients, and media placement, it is actually very difficult to end up with expenses lower than that in 2019.

----------

노르웨이 크루즈 홀딩스(NYSE: NCLH)는 2023년 2분기 재무 실적을 발표했다. 이는 코로나19가 폭발한 이래 크루즈회사의 실적이 가장 좋은 분기로서 노르웨이크루즈도 예외가 아니다.

노르웨이 크루즈는 이번 분기에 69만3,000명의 승객을 수송해 2019년 같은 기간에 비해 1.6% 증가했다. Adjusted EBITDA는 5억1,500만 달러로 코로나 사태 이후 첫 흑자이자 2019년 같은 기간(4억9,700만 달러)을 넘어섰다. 그러나 이전에 하이저 캐피털이 언급했듯이, 순이익은 EBITDA보다 부채 이자를 고려하지 않기 때문에 실제 경영 상황을 더 잘 반영한다. 노르웨이 크루즈의 이번 분기 순이익은 8,612만달러로 2019년 같은 기간(2억4,000만달러)보다 적었다. 동행 중 노르웨이 크루즈의 활약은 상당히 좋았다. 참고로 카니발 크루즈 그룹(NYSE: CCL)의 이번 분기 영업스익은 49억1,000만 달러로 2019년 동기(48억4,000만 달러)를 약간 웃돌았지만 4억1,000만 달러의 적자를 내 2019년 동기 이익(4억5,000만 달러)을 크게 밑돌았다. 주요 차이점은 카니발이 이번 분기에 5억4,000만 달러의 추가 이자를 지출했다는 것이다. 카니발이 실제로 은행그룹을 위해 아르바이트를 하고 있는 것이다.

실제로 온라인 여행사나 전통 여행사에 비해 부채 규모와 연료 가격 변동에만 관심을 기울이면 크루즈 회사의 영업수익을 더 쉽게 계산할 수 있다. 일반적으로 크루즈 회사들은 50%가 넘는 사전 예약(노르웨이 크루즈 회사의 2분기 예약의 70%가 2024년과 2025년의 선표 판매)을 하고 있으며, 이로 인해 50%가 넘는 선석은 보통 1년 전에 예매(노르웨이 크루즈 회사의 2분기는 60%가 있음)된다. 이는 다른 여행 상품에 비해 크루즈 선사들이 예약에 더 높은 가시성을 가지고 있다는 것을 의미한다. 그러므로 선표판매량, 좌석수, 채무 등 수치를 통해 우리는 대체적으로 미래 영업수익의 상한선과 하한선을 계산해낼수 있다. 크루즈 회사가 미리 정보를 공개하는 습관도 투자자들의 판단을 도울 수 있다. 노르웨이 크루즈 홀딩스의 이번 분기 재무 실적을 예로 들면, 하이저 캐피털은 영업수익과 비용을 계산한 경험을 공유했다.

1. 영업수익 = 총 승객 수 x 승객 한 명당 평균 여행 일수 x 평균 일일 요금. 이것 도 '총 객실 수 ×2 ×입주율 ×90 ×하루 평균 가격'로 계산할 수 있다. 이것은 구체적으로 크루즈 회사가 투자 은행에 어떤 데이터를 미리 발표하는 선호가 있는지에 달려 있다. 크루즈 회사들은 유리한 데이터를 먼저 공개하는 경향이 있기 때문에 다른 '잊혀진' 데이터에 대해서는 스스로 연구하고 평가해야 한다. 예를 들어, 크루즈 화사는 2019년 같은 기간보다 40% 높은 선표 단가와 100%의 투숙률을 언급할 수 있지만, 2019년에 비해 용량(유람선 총수)이 크게 줄었다는 것을 언급한 것을 '잊어버릴' 수도 있다.

2. 가장 주목해야 할 비용은 부채다. 마찬가지로 회사는 EBITDA가 사상 최고 수준을 기록했다고 발표할 수도 있지만, 다음 분기에 갚아야 할 이자 규모, 원금 금액, 채무 전환으로 인한 지분 희석을 언급한 것을 '잊어버렸'다. 상환해야 할 이자와 원금은 순이익에 영향을 주고 지분 희석은 수익률에 영향을 줄 것이다. 둘 다 투자 가치에 영향을 미칠 것이다. 코로나19 발생 이후 이 회사는 직원 수가 2019년보다 더 간소화되고 음식 원자재 운송 효율이 높으며 광고와 채널 비용을 줄이기 위해 더 많은 직접 판매 채널을 구축했다고 자주 밝혔다. 그러나 인건비, 식량 원자재 및 미디어 투입을 포함한 모든 유형의 원가/비용이 팽창하고 있다는 점을 고려할 때 실제로 2019년에 이보다 낮은 비용으로 결제하기가 어렵다.

文章鏈接 Hyperlink:https://www.nclhltd.com/investors/financial-information/financial-results

資料來源 Resource:NCLH

標籤 Label:Cruise NCLH RCL CCL