登錄

選單

登錄

海擇短評 Haize Comment:

近期南韓電商Coupang(NYSE: CPNG)公告2023Q2財報,收入與淨利再創新高,活躍用戶也有所增長,公司在電商商業模式中,除了原本對C端的產品,也開始推動對B端(供應商)的服務;另外在國際化的布局中,Coupang與SEA(NYSE: SE)這兩家300億美元量級的公司,在台灣市場的駁火則可能開始升級。海擇資本披露部分觀點如下:

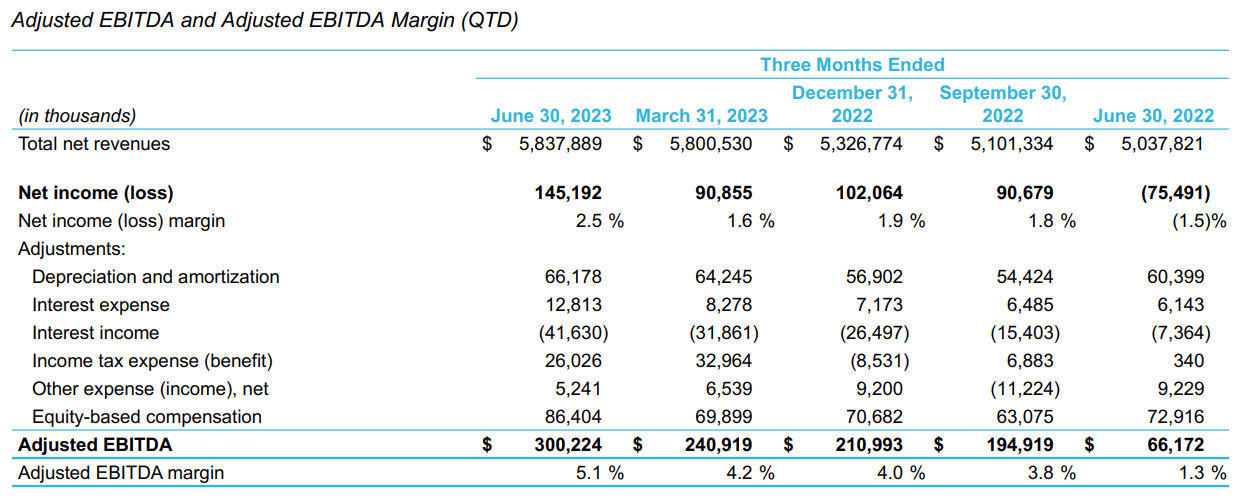

1. 收入/淨利同創歷史新高:本季Coupang收入(58.38億美元)與淨利(1.45億美元)雙雙創下歷史新高。不過,由於收入QoQ僅增長1%不到,淨利推高的原因更偏向費用控管得宜,本季營業費用比2022年同期還低了13%,對增長機會也偏向節制且針對性的投入資本支出。

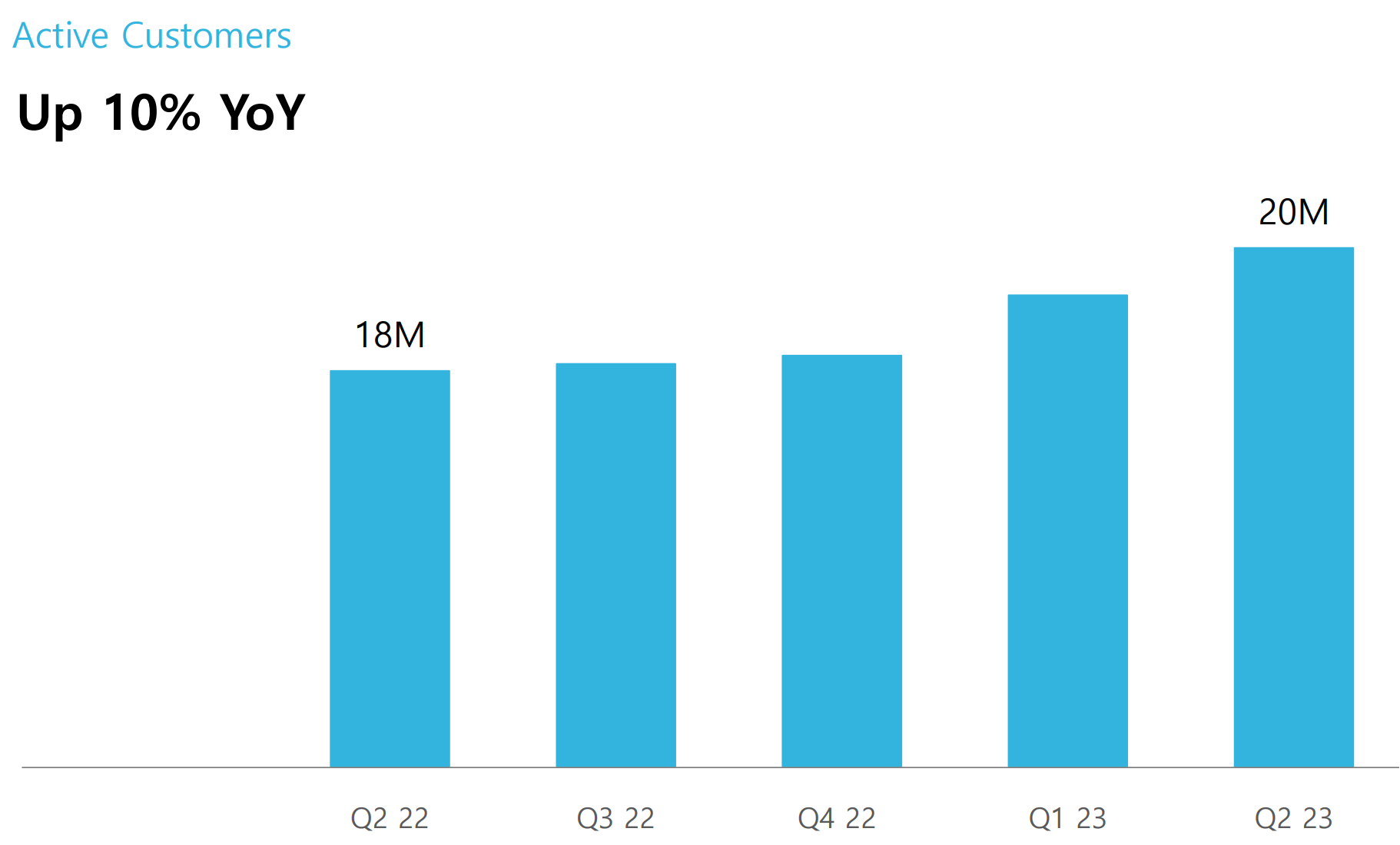

2. 客戶活躍增速:比較特別的是,Coupang本季(付費)客戶的增速提快,2022Q4、2023Q1、Q2的YoY增速分別是1%、5%、10%,季末達到1,970萬,在當前經濟減速期,這樣的成績難能可貴。

3. B端服務增速高於C端:根據公司公告,除了C端自營產品增速好,包括時尚和美容在內各C端品類的第三方產品,銷售額也都以零售市場的倍數增長;而對供應商端的商業服務,比如Coupang 的廣告、保險和物流(FLC, Fulfillment & Logistics by Coupang),增速還是整體增速的兩倍以上。

4. 加重國際化投入台灣:Coupang目前內部的新事業體有三部分:Eats(外賣)、Taiwan(台灣地區電商)和Play(訂閱式影音串流媒體),公司此前也談過認為可以複製南韓模式到台灣,本季在推遲與取消不符合內部要求的投資之際,也確立了台灣市場的優先級僅次於Eats。台灣電商目前更多的是momo(TW: 8454)與SEA旗下蝦皮(Shopee)間的巨頭競爭,Coupang與SEA目前同為300億美元量級的公司,會對台灣電商市場格局造成什麼影響,值得觀察。

----------

South Korean e-commerce Coupang (NYSE: CPNG) revealed its 2023 Q2 earnings, with both revenue and net profit reaching new highs, and a growth in the number of active users. In the e-commerce business model, besides its existing C-side products, the company has also started to promote B-side services. Additionally, in terms of international expansion, there might be escalating competition in the Taiwanese market between Coupang and SEA (NYSE: SE), both being companies valued at around $30 billion. Insights by Haize Capital:

1. Revenue/Net Profit Both Hit Historic Highs: This quarter, Coupang reported a historic high in both revenue ($5.838 billion) and net profit ($145 million). However, since the revenue showed a quarter-on-quarter growth of just under 1%, the rise in net profit can be attributed more to efficient cost management. The operating expenses this quarter were 13% lower than the same period in 2022, showing a restrained and targeted capital investment approach to growth opportunities.

2. Acceleration in Active User Growth: Notably, the growth of Coupang's (paid) users accelerated this quarter. The year-over-year growth rates for Q4 2022, Q1 2023, and Q2 2023 were 1%, 5%, and 10% respectively, with paid users reaching 19.7 million by the end of the quarter. This is an achievement, especially during the current economic slowdown.

3. B-side Services Grow Faster Than C-side: According to the company's announcement, aside from the good growth rate of C-side proprietary products, sales of third-party products in various C-side categories, including fashion and beauty, have grown at a rate multiple times that of the retail market. For services geared towards suppliers, such as Coupang's advertising, insurance, and FLC(Fulfillment & Logistics by Coupang), the growth rate is more than double the overall.

4. Increasing Investment in Taiwan for Internationalization: Currently, Coupang has three internal new business units: Eats (food delivery), Taiwan (e-commerce in the Taiwan region), and Play (video streaming media subscription). The company has previously discussed its belief in replicating the South Korean model in Taiwan. This quarter, while delaying and canceling investments that don't meet internal requirements, the company has also determined Taiwan's market priority just behind Eats. Taiwan's e-commerce scene is currently dominated by competition between momo (TW: 8454) and SEA's Shopee. With both Coupang and SEA being companies valued at around 30 billion USD, their impact on Taiwan's e-commerce market is worth observing.

----------

한국 전자상거래 업체인 쿠팡(Coupang, NYSE: CPNG)은 2023년 2분기 재무 실적을 발표했다. 영업수익과 순이익이 모두 최고치를 기록했고, 활성 사용자 수도 증가했다. 전자상거래 비즈니스 모델에서 기존의 C단 제품 외에 회사도 B단(공급업체) 서비스를 출시하기 시작했다. 또한 국제 확장의 경우 타이완 시장에서 쿠팡과 SEA(NYSE: SE)의 경쟁이 심화 될 수 있다. 이 두 회사의 평가액은 모두 300억 달러 정도이다. 다음은 하이저 캐피털의 견해다.

1. 영업수익/순이익 모두 사상 최고치를 기록했다. 이번 분기 쿠팡은 영업수익(58억3,800만달러)과 순이익(1억4,500만달러) 모두 사상 최대를 기록했다. 그러나 수익의 QoQ 성장률이 1%를 약간 밑돌기 때문에 순이익의 증가는 효과적인 원가 관리에 더 많이 기인할 수 있다. 이번 분기 운영비는 2022년 같은 기간보다 13% 하락했다. 이는 성장 기회에 대한 쿠팡의 보수적이고 맞춤형 자본 투자 방식을 보여준다.

2. 활성 사용자 증가가 가속화했다. 특히 이번 분기에는 쿠팡의 (유료)가입자 증가가 가속화했다. 2022년 4분기, 2023년 1분기, 2023년 2분기의 YoY 성장률은 각각 1%, 5%, 10%이며, 이번 분기 말 현재 유료 가입자는 1,970만명에 달한다. 현재 경제가 둔화되는 상황에서 이것은 매우 어렵게 달성한 실적이다.

3. B단 서비스의 증가 속도가 C단보다 빠르다. 회사의 공고에 따르면, C단 전유 제품의 증가 속도가 양호한 것 외에, 패션과 뷰티를 포함한 C단 각 품목의 제3자 제품의 판매 증가 속도는 소매 시장의 증가 속도의 몇 배이다. 쿠팡의 광고·보험·물류 (FLC, Fulfillment & Logistics by 쿠팡)와 같은 공급자 대상 서비스의 경우 증가율이 전체 증가율의 두 배 이상이었다.

4. 타이완에 대한 투자를 늘려 국제화를 실현한다. 현재 쿠팡은 내부적으로 Eats(배달), Taiwan(타이완 지역 전자상거래), Play(동영상 스트리밍 구독) 등 3개 사업부를 신설했다. 이 회사는 앞서 타이완에서 한국 모델을 복제하려는 아이디어를 논의한 바 있다. 이번 분기에는 내부 요구에 부합하지 않는 투자를 연기하고 취소하는 동시에 타이완 시장의 우선순위도 Eats에 버금가는 것으로 확정했다. 타이완의 전자상거래 분야는 현재 momo(TW: 8454) 와 SEA 산하의 쇼피(Shopee) 간의 경쟁이 주도하고 있다. 쿠팡과 SEA는 모두 300억 달러 안팎으로 평가되는 회사로 타이완 전자상거래 시장에 미치는 영향은 지켜볼 만하다.

文章鏈接 Hyperlink:https://ir.aboutcoupang.com/English/financials/quarterly-results/default.aspx

資料來源 Resource:Coupang

標籤 Label:South Korea E-commerce CPNG SE Taiwan