登錄

選單

登錄

海擇短評 Haize Comment:

同程旅行(HK: 0780)近期公告2023Q2財報。在一季度Adjusted EBITDA已經超過7億人民幣的基礎上,Q2交易額與Adjusted EBITDA再創歷史新高,其中在低線城市的布局深入程度優於其國際化布局;從這個角度看,近期日本核污水事件衝擊中國出境遊,也許這對同程來說未必是壞事。海擇資本部分觀點如下:

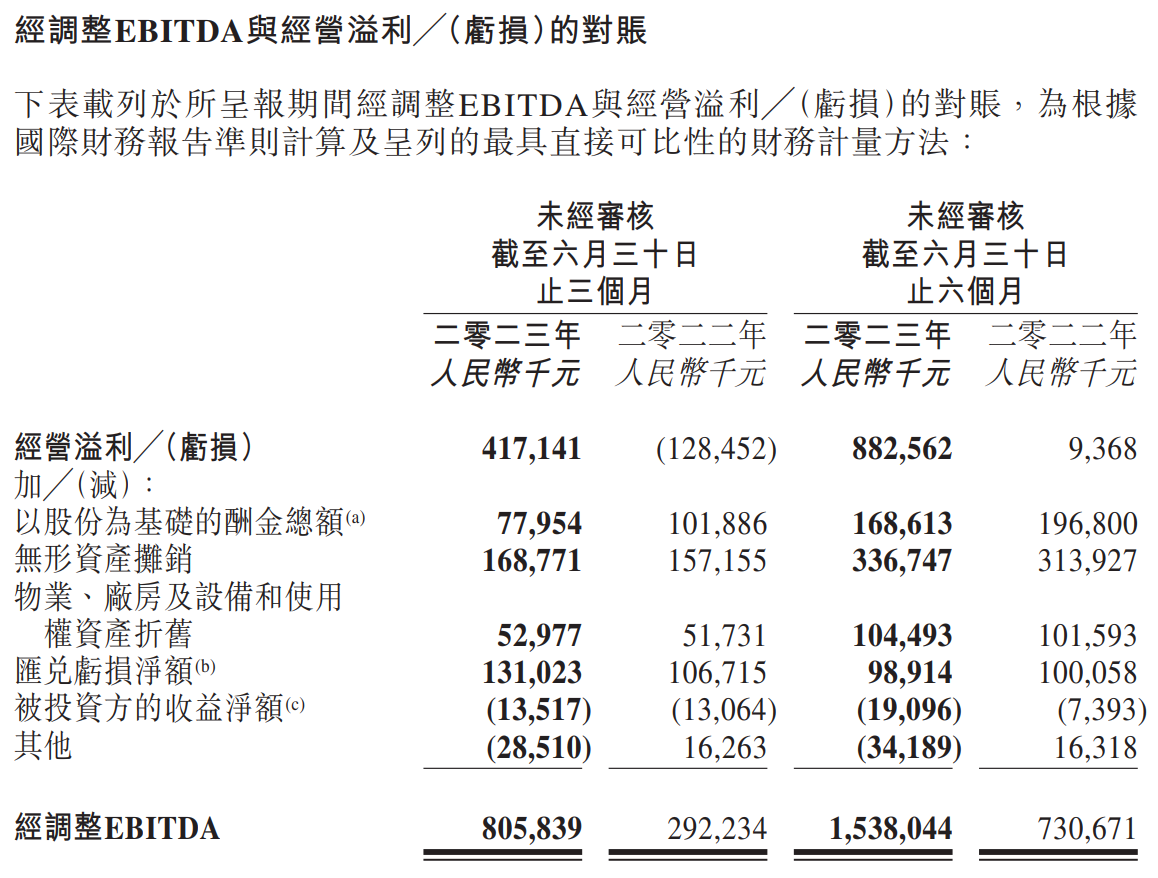

1. 財務表現創歷史新高:本季同程總交易額597億人民幣,YoY增長146%,QoQ增長4%,較2019年同期增長45%;Adjusted EBITDA為8.06億人民幣,YoY增長176%,QoQ增長10%,較2019年同期增長83%。大體來說,YoY增長高是因為去年基期低,QoQ增長小表示新的增長點尚未明確,這也是同程良好現況中的小隱憂。

2. 住宿增速優於交通:與2019Q1相比,同程本季住宿預訂服務收10.6億人民幣,QoQ增速12%,優於交通票務收入14.9億人民幣所對應的8%增速。同程在酒店的增長,我們認為與其圍繞酒店住宿的各種場景探索需求、交叉銷售策略,以及進入從低星至高星酒店管理事業有關,這部分算漸有所成。

3. QoQ運營利潤下滑:同程本季Adjusted EBITDA雖然創下歷史新高,但從運營利潤的角度看,本季來自本業的運營利潤4.17億人民幣,較Q1低10%;EBITDA結算會超過Q1的原因,在於Q2認了一筆1.31億的業外匯兌收入。本業下滑是我們認為同程逐漸發生的小隱患,亦即,雖然交易額變大、付費用戶增加,但實際上得用更大的邊際成本才能維繫住這批用戶在國內消費,這部分隨著出境遊復甦,也許更好的境外布局能改善這個風險。

4. AI進展還待明確:本季同程也重申了從在線旅遊平台轉型為智能出行管家的定位,並加入生成式AI的元素。不過,雖說公司說明優化"慧行系統",提升客戶服務的自動化程度,將標準化問題交由AI驅動的機器人處理;不過,關於所提到的在各產品線中應用人工智能生成內容(AIGC, Artificial Intelligence-Generated Content),由於暫時還看不出明顯的典範或成果,這視為探索中可能更正確。

----------

Tongcheng Travel (HK: 0780) released its financial results for the second quarter of 2023. Following the Q1's Adjusted EBITDA of more than 700 million RMB, the Q2's GMV and Adjusted EBITDA reached a new historical high. Notably, its penetration in lower-tier cities was better than its international expansion. From this perspective, the impact of the Japanese nuclear contaminated water incident on China's outbound tourism may not necessarily be a bad thing for Tongcheng. Some views of Haize Capital:

1. Financial performance hits a new historical high: This quarter, Tongchen's total GMV reached 59.7 billion RMB, a year-on-year increase of 146%, a quarter-on-quarter increase of 4%, and a 45% increase compared to the same period in 2019. The Adjusted EBITDA was 806 million RMB, a year-on-year increase of 176%, a quarter-on-quarter increase of 10%, and an 83% increase compared to the same period in 2019. Generally speaking, the high year-on-year growth is due to the low base last year, and the small quarter-on-quarter growth indicates that new growth points are not yet clear, which is a minor concern amid Tongcheng's current good situation.

2. Accommodation growth better than transportation: Tongcheng's hotel booking revenue was 1.06 billion RMB this quarter, with a quarter-on-quarter growth of 12%, better than the 8% growth of the transportation ticketing revenue (1.49 billion RMB). We believe that Tongcheng's growth in the hotel sector is related to its exploration of various scenarios surrounding hotels, cross-selling strategies, and entering the hotel management business from low-star to high-star hotels. This part is gradually being successful.

3. QoQ Operating Profit Decline: Although Tongcheng's Adjusted EBITDA for this quarter has reached a historic high, its operating profit from core businesses this quarter was 417 million RMB, 10% lower than Q1; the EBITDA settlement exceeding Q1 is due to a 131 million non-operating revenue recognized in Q2. The decline in core business is a hidden danger, that is, although the GMV and paying users have increased, in fact, a higher marginal cost is required to maintain its domestic business. The outbound tourism will return in the future, perhaps better overseas layout can mitigate this risk.

4. AI Progress Still Unclear: This quarter, Tongcheng also reaffirmed its position as transforming from an online travel platform to an intelligent travel steward, and added elements of generative AI. However, although the company stated that it optimized the "Huixing System", increased the automation level of customer service, and handed over standardized questions to AI-driven robots; however, regarding the mentioned application of Artificial Intelligence-Generated Content (AIGC) in various product lines, since there is no obvious results temporarily, it may be more appropriate to consider this as exploratory.

----------

퉁청여행(同程旅行, HK: 0780)은 2023년 2분기 재무 실적을 발표했다. 1분기 Adjusted EBITDA가 7억 위안을 넘어선 데 이어 2분기 GMV와 Adjusted EBITDA가 사상 최고치를 경신했다. 주목할 만한 것은 저선 도시에서의 배치가 국제 시장보다 더 깊다는 것이다. 이런 관점에서 볼 때, 일본의 핵 오염수 사건이 중국의 해외여행에 미치는 영향은 퉁청여행에 있어서 반드시 나쁜 것은 아니다. 이에 대해 하이저 캐피털의 일부 관점은 다음과 같다.

1. 재무실적 다시 사상 최고치에 기록했다. 이번 분기에 퉁청여행의 총 GMV는 597억 위안에 달해 YoY는 146%, QoQ는 4% 증가했다. 이는 2019년 동기 대비 45% 증가했다. Adjusted EBITDA는 8억600만 위안으로 YoY는 176%, QoQ는 10% 증가했다. 이는 2019년 동기 대비 83% 증가했다. 전체적으로 YoY 증가폭이 큰 것은 지난해 기수가 낮기 때문이다.QoQ 성장폭이 작은 것은 아직 새로운 성장점이 명확하지 않기 때문이다. 퉁청여행의 현재 양호한 형세 하에서, 이것은 작은 문제만이다.

2. 숙박사업의 실적 증가는 교통사업보다 낫다. 퉁청여행의 이번 분기 호텔 예약 영업수익은 10억6,000만 위안으로 QoQ는 12% 증가했다. 호텔사업 실적의 증가 속도는 교통 티켓 사업(영업수익 14억9,000만 위안, 8% 증가)보다 낫다. 우리는 퉁청여행이 호텔 분야에서의 성장은 호텔 주변의 각종 업무 장면에 대한 탐색, 교차 판매 전략, 저성급 호텔에서 고성급 호텔로 호텔 관리 업무에 진출하는 것과 관련이 있다고 생각한다. 이 부분 사업은 점차 성공을 거두고 있다.

3. QoQ 영업이익이 감소했다. 퉁청여행은 이번 분기 Adjusted EBITDA가 사상 최고치를 기록했지만 이번 분기 핵심 사업 영업이익은 4억1,700만 위안으로 1분기보다 10% 감소했다. EBITDA 결제액이 1분기를 넘어선 것은 2분기에 1억3,100만 위안의 영업외수익이 확인됐기 때문이다. 핵심 사업의 하락은 GMV와 유료 사용자가 증가했지만 실제로 국내 사업을 유지하는 데 더 높은 한계 비용이 필요하다는 퉁청여행의 잠재적 위험이다. 해외여행 사업이 회복됨에 따라 더 나은 해외 배치가 이런 위험을 완화시킬 수 있을 것이다.

4. 인공지능의 진전은 아직 불투명하다. 이번 분기에 퉁청여행은 온라인 여행 플랫폼에서 스마트 여행 집사로 전환하는 포지셔닝을 재확인하고 생성식 인공지능의 요소를 추가했다. 그러나 이 회사는 'Huixing 시스템(慧行系統)'을 최적화하고 고객 서비스의 자동화 수준을 높였으며 표준화 문제를 인공 지능으로 구동되는 로봇에 맡겼다고 밝혔지만 위의 인공 지능 생성 콘텐츠(AIGC, Artificial Intelligence-Generated Content) 의 각 제품 라인에서의 적용은 일시적으로 뚜렷한 효과가 없기 때문에 '여전히 탐색 중'으로 보는 것이 더 적합할 수 있다.

文章鏈接 Hyperlink:https://www.tongchengir.com/cn/investor-relations/announcements-circulars/

資料來源 Resource:Tongcheng

標籤 Label:Tongcheng 0780 China Accommodation Ticketing