登錄

選單

登錄

海擇短評 Haize Comment:

途牛(NASDAQ:TOUR)近期公告史上首次轉盈財報,在中國境內的抖音直播銷售也頗有所成,不過規模相對於2019已快速縮小,市值要恢復往日榮光並不容易。海擇資本分析如下:

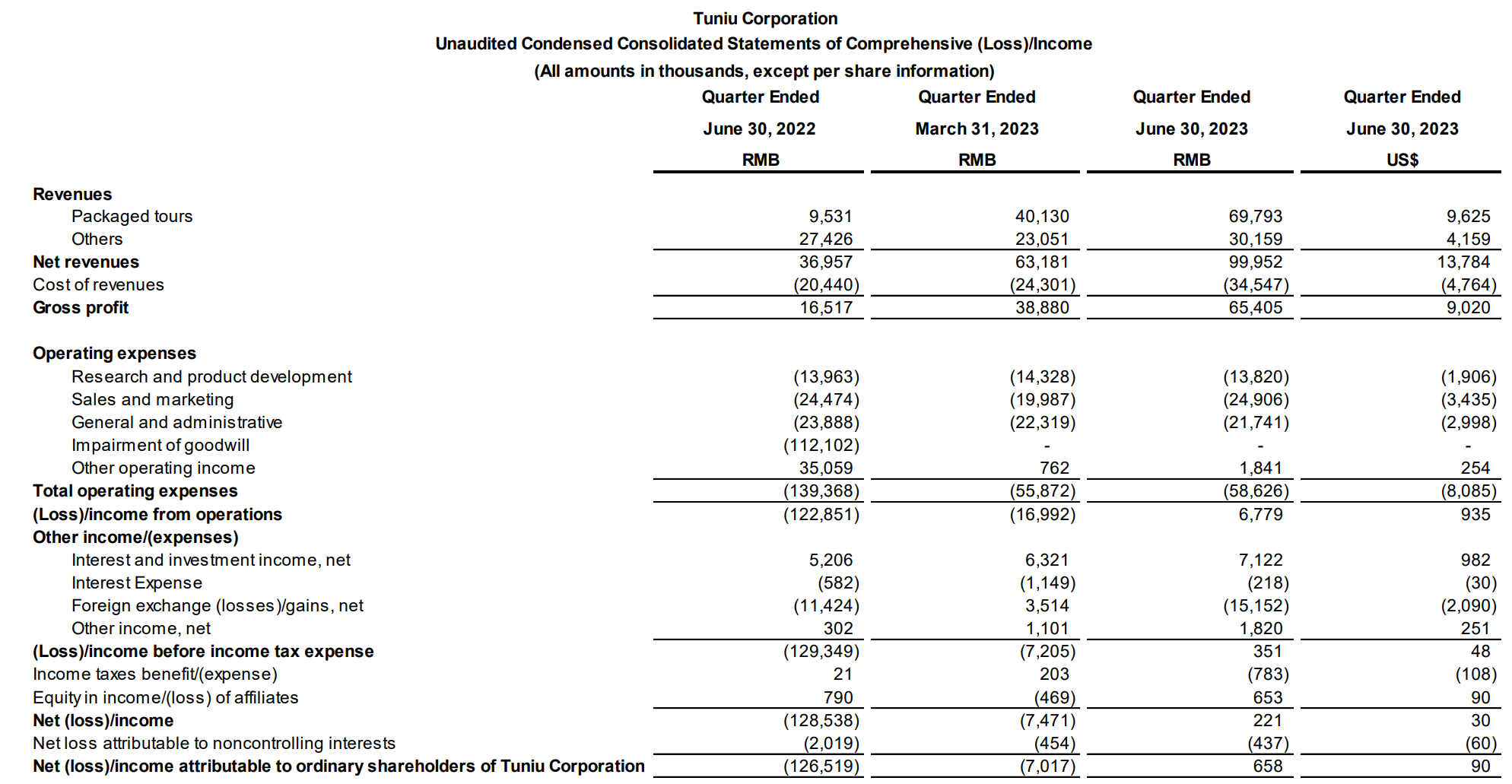

1. 首次營業利潤轉正:在連續兩個季度保持運營現金流為正後,途牛Q2首次轉盈。依公告本季收入9,995萬人民幣,YoY增長170%;營業利潤678萬人民幣轉虧為盈;其中團隊遊收入增速632%, 優於其他收入增速,而其他收入的主要增長來自於保險服務費。

2. 收入規模難比2019:相對於2019年團隊遊收入4.29億人民幣,本季團隊遊約恢復至當年的19%;2019年其他收入為9,085萬人民幣,本季約恢復至當年的33%。目前看來,如果公司的產品結構沒有大幅改變,收入規模要恢復2019年的規模並不容易。

3. 抖音為新主要銷售通路:根據公司說明,Q2途牛在抖音的直播帳號,為酒旅品類銷量全國前三;不過並未公告銷售額、成本與退貨率。

4. Q3收入預期優於Q2:公司預期Q3收入YoY增長110%至120%,亦即將超過1.64億人民幣,MoM增長將超過64%;不過由於盈利結構尚未穩定,尚難推斷盈利能否持續放大。

----------

Tuniu (NASDAQ: TOUR) recently announced its first-ever profitable financial report. While its Douyin live sales within China have achieved some results, the scale has rapidly decreased compared to 2019. Regaining its former market value glory will not be easy. Haize Capital's analysis is as follows:

1. First-time positive operating profit: After maintaining a positive operating cash flow for two consecutive quarters, Tuniu turned profitable in Q2. According to the announcement, the revenue for this quarter was 99.95 million RMB, a YoY increase of 170%; operating profit of 6.78 million RMB turned from loss to profit. Group tour revenue grew at a rate of 632%, outpacing other revenue growth. The primary growth in other revenues came from insurance service fees.

2. Revenue scale challenging to match 2019: Compared to the group tour revenue of 429 million RMB in 2019, this quarter's group tour revenue has only recovered to about 19% of that year. In 2019, other revenues amounted to 90.85 million RMB, and this quarter it has approximately recovered to 33% of that year. At present, if the company's product structure does not undergo significant changes, it won't be easy to restore the revenue scale to 2019 levels.

3. Douyin as the new primary sales channel: According to the company's statement, Tuniu's live streaming account on Douyin ranked among the top three in sales for the hotel and tour category nationwide in Q2. However, they did not disclose sales figures, costs, or return rates.

4. Q3 revenue forecasted to surpass Q2: The company expects Q3 revenue to grow YoY by 110% to 120%, meaning it will exceed 164 million RMB, with a MoM growth surpassing 64%. However, since the profit structure is not yet stable, it's hard to predict whether profitability can continue to scale up.

----------

Tuniu(途牛, NASDAQ: TOUR)는 최근 첫 흑자를 낸 재무실적 보고서를 발표했다. 틱톡 중국판인 Douyin의 중국 생방송 판매는 일부 성과를 거두었지만 2019년에 비해 규모가 빠르게 축소됐다. 시가는 예전의 영광을 회복하기는 쉽지 않다. 다음은 하이저 캐피털의 분석이다.

1. 처음으로 영업이익을 실현하다. Tuniu는 2분기 연속 경영성 현금 흐름을 플러스로 유지한 뒤 2분기에 흑자를 냈다. 공고에 따르면 이번 분기의 영업수익은 9,995만위안으로 전년 동기 대비 170% 증가되였다. 영업이익은 678만위안으로 흑자로 돌아섰다. 단체여행의 영업수익은 632%의 속도로 증가해 기타 수익의 증가를 앞질렀다. 기타 수익의 주요 증가는 보험 서비스 비용에서 나온다.

2. 수익 규모는 2019년과 비교하기 어렵다. 2019년 4억2,900만위안의 단체여행 영업수익과 비교하면 이번 분기 단체여행 영업수익은 그해 19%가량으로 회복하는 데 그쳤다. 2019년 기타수익은 9,085만위안으로 이번 분기에 이미 당년의 33% 좌우로 회복되였다. 현재 회사의 제품 구조에 큰 변화가 없다면 수익 규모를 2019년 수준으로 회복하는 것은 쉽지 않다.

3. Douyin은 새로운 주요 판매 채널이되었다. 이 회사의 성명에 따르면 Tuniu의 Douyin 생방송 계정은 2분기 전국 호텔과 여행 매출액 중 1~3위를 차지했다. 그러나 이들은 구체적인 매출액, 원가 또는 반품률을 밝히지 않았다.

4. 3분기의 영업수익은 2분기를 넘어설 것으로 예상된다. 회사는 3분기의 영업수익이 전년 동기 대비 110%~120% 증가할 것으로 예상하고 있다. 이는 3분기의 영업수익이 1억 6,400만위안을 초과할 것이고, MoM이 64% 이상으로 증가할 것이라는 것을 의미한다. 그러나 이익 구조가 아직 불안정하기 때문에 수익이 계속 확대될 수 있을지 예측하기 어렵다.

文章鏈接 Hyperlink:https://ir.tuniu.com/press-releases

資料來源 Resource:Tuniu

標籤 Label: Tuniu TOUR Channel Douyin