登錄

選單

登錄

海擇短評 Haize Comment:

嘉年華郵輪集團(NYSE: CCL)近期公告2023Q3財報,季淨利超過10億美金,打臉此前Morgan Stanley分析師認定其價值為零的預期。在資本支出的選擇中,嘉年華選擇清償10億美金量級的債務,而非全力導入新運力,雖然降低了未來的盈利可能,但也降低了債務風險。唯Q4逆風再起,國際燃油費用增加,庫存售罄也影響淨利再攀高峰的機會,如果美國沒有重燃硬著陸風險,我們認為郵輪的投資價值還能承載玩樂體驗元素。海擇資本解讀嘉年華本季財報如下:

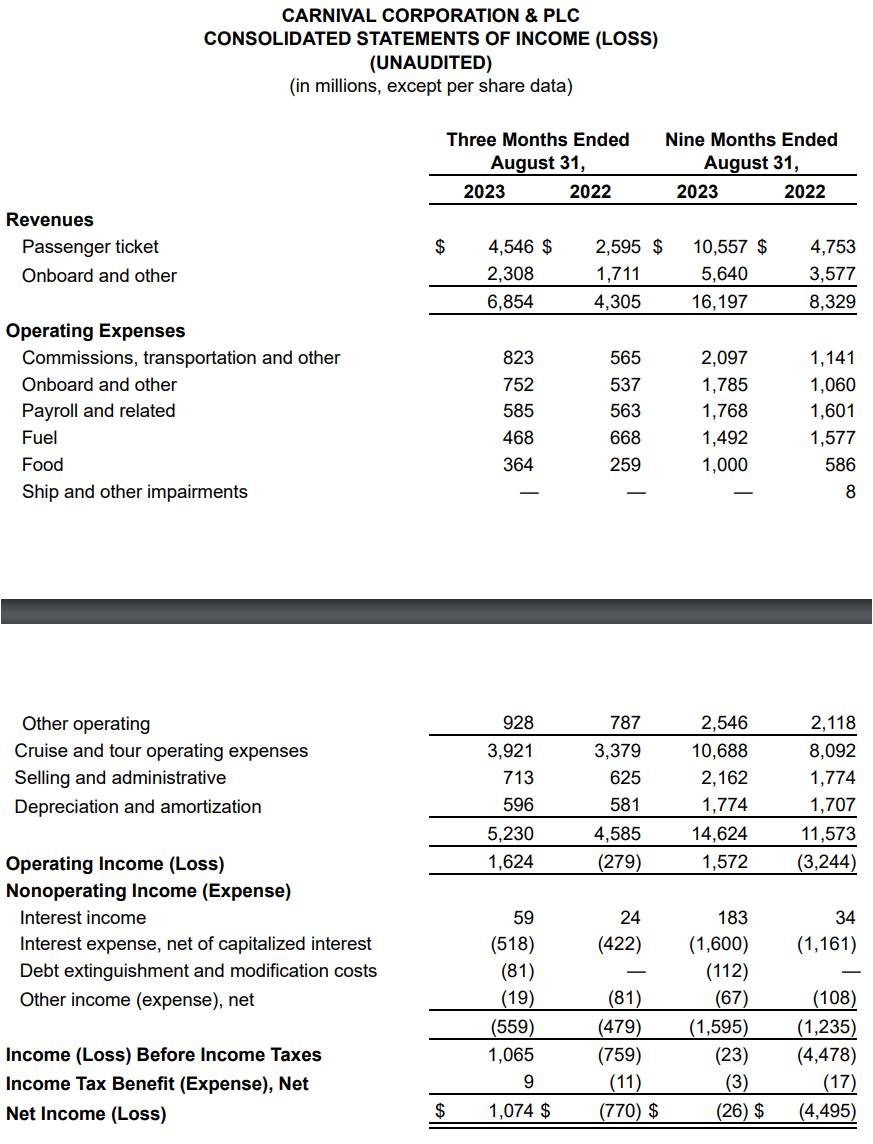

1. 淨利恢復疫前60%:嘉年華Q3收入68.5億美元創歷史新高,運營利潤16.2億美元已達2019Q3的86%;而已扣除龐大利息後的淨利為10.7億美元,已達2019Q3的60%;值得注意的是,Q3薪資5.9億美元比Q2的6.0億美元還略低,表示公司還在儘可能的降本增效。

2. 需求由北美和歐洲帶動:根據財報,嘉年華本季ALBD(Average lower berth day, 可理解為佔床間夜數)為2,370萬,較2019Q3高出4%;強勁需求由北美和歐洲市場推動。如果從固定匯率看(不需考慮債務因素的)EBITDA,嘉年華Q1達到2019年同期的59%,Q2達到了73%,Q3達到了90%,算是在疫情後走入穩定。

3. 成為還債機器:此前海擇觀點也談過,目前EBITDA無法用來衡量郵輪集團的盈利能力,因為疫情間貸入了過多高利率債務與過度稀釋股本;關於前者,嘉年華也在快速處理問題,債務餘額已從Q1的350億美元降低到Q3的310億美元,兩季間償還近40億美元,年底應該可以控制在略高於300億美元。

4. 風險與增長同行:公司CEO兼總裁Joshua Weinstein談到近期飆升的燃油價格,說明收入增加足以抵銷近期燃油價格飆升(The higher revenue alone more than offset the recent spike in fuel prices),但這句話反過來解讀也是一樣的,不愧是CEO級別的話術。不過公司對Q4仍給到EBITDA盈利8億美元至9億美元的預期,整體來看,即便依較嚴苛的GAAP會計準則看,應仍能維持淨利,盈利能力介於Q2與Q3之間;而2024年由於新增運力不多,庫存也大體銷售殆盡,相對於今年再有爆炸性增長的機會就不高了。

----------

Carnival Cruise Line (NYSE: CCL) released its 2023 Q3 financial results, with a quarterly net profit exceeding $1 billion, crashing the previous prediction of Morgan Stanley analysts that the company values zero. As for capital expenditure, Carnival chose to repay debts in the ballpark of $1 billion instead of aggressively adding new capacity. Although this might limit future earnings potential, it also reduces the risk associated with debt. However, headwinds are expected in Q4, with international fuel costs on the rise and sold-out inventory, which might affect the opportunity for further increases in net profit. Assuming the U.S. doesn't face a hard landing risk, we believe the investment value of the cruise industry lies in the industry's capability of offering experience and activities. Haize Capital interprets Carnival's financial report for this quarter as follows:

1. Net profit recovers to 60% of pre-pandemic levels: Carnival's Q3 revenue reached a historic high of $6.85 billion, with an operating profit of $1.62 billion, which is 86% of that in Q3 2019. The net profit, after deducting significant interest expenses, was $1.07 billion, reaching 60% of Q3 2019. Notably, Q3 wages of $590 million were slightly lower than the $600 million in Q2, indicating that the company is still striving to reduce costs and increase efficiency.

2. Demand driven by North America and Europe: According to the financial report, Carnival's ALBD (Average Lower Berth Day) for this quarter was 23.7 million, a 4% increase compared to Q3 2019. The robust demand was propelled by the North American and European markets. When viewing the EBITDA at constant currency rates (without considering debt factors), Carnival reached 59% of the same period in 2019 in Q1, 73% in Q2, and 90% in Q3, indicating stabilization post-pandemic.

3. Heavy debt burden: As Haize Capital previously pointed out, the current EBITDA cannot be used to measure the profitability of cruise groups, because during the pandemic, excessive high-interest rate debt was taken on and there was an over-dilution of equity. Regarding the former, Carnival is rapidly addressing the problem, the debt balance has decreased from $35 billion in Q1 to $31 billion in Q3, repaying nearly $4 billion over two quarters. By year-end, it should likely be controlled slightly above $30 billion.

4. Risks and growth go hand in hand: The company's CEO and President, Joshua Weinstein, commented on the recent surge in fuel prices, noting that the higher revenue alone more than offset the recent spike in fuel prices. However, we can interpret it in the opposite way, it's just the CEO's art of language. Nevertheless, the company still projects an EBITDA profit of $800 million to $900 million for Q4. Overall, even when viewed under the stricter GAAP accounting standards, net profit should still be maintained, with profitability lying between Q2 and Q3. As for 2024, with limited additional capacity and most of the inventory already sold out, the chance for explosive growth compared to this year is not high.

----------

카니발 크루즈(NYSE: CCL)는 2023 년 3 분기 실적을 발표했다. 분기 순이익은 10억 달러를 넘었다. 이것은 모건스탠리 애널리스트들이 그동안 이 회사의 평가액이 0일 것이라는 전망을 깼다. 자본 지출에서 카니발은 새로운 생산 능력을 대거 늘리는 대신 약 10억 달러의 부채를 상환하기로 선택했다. 이는 미래의 수익 잠재력을 제한할 수 있지만 부채와 관련된 위험도 낮출 수 있다. 그러나 국제 연료비 상승과 재고 매진으로 4분기 '역풍'이 예상된다. 이는 순이익이 더 늘어날 수 있는 기회에 영향을 미칠 수 있다. 미국이 더 이상 경착륙의 위험을 무릅쓰지 않는다고 가정하면, 우리는 크루즈 산업의 투자 가치가 그 산업이 경험과 활동을 제공하는 능력에 있다고 생각한다. 하이저 캐피털은 카니발의 이번 분기 재무 실적에 대해 다음과 같이 해석했다.

1. 순이익은 코로나 발생 전 수준의 60%를 회복했다. 카니발의 3분기 수입은 68억5,000만 달러로 사상 최고치를 기록했다. 영업이익은 16억2,000만 달러로 2019년 3분기의 86%였다. 이자 지출을 뺀 순이익은 10억7,000만 달러로 2019년 3분기의 60%에 달했다. 특히 3분기 5억9,000만 달러의 임금은 2분기 6억 달러를 약간 밑돌았다. 이것은 회사가 여전히 비용을 절감하고 효율성을 높이기 위해 노력하고 있음을 보여준다.

2. 북미와 유럽이 시장의 수요를 구동한다. 재무 실적에 따르면 이번 분기 카니발의 ALBD(Average lower berth day)는 2,370만으로 2019년 3분기보다 4% 증가했다. 강력한 수요는 북미와 유럽 시장에 의해 추진된다. EBITDA를 고정환율(채무요인 제외)로 계산하면 카니발은 1분기 2019년 같은 기간의 59%, 2분기 73%, 3분기 90%를 기록했다. 이는 시장이 코로나 발생 후 안정에 접어들었음을 보여준다.

3. 무거운 부채 부담: 하이저 캐피털이 이전에 지적했듯이, 현재의 EBITDA는 크루즈 그룹의 수익성을 측정하는 데 사용할 수 없다. 코로나 사태 때 크루즈그룹이 고금리 채무를 너무 많이 부담했고 지분이 과도하게 희석됐기 때문이다. 전자에 대해 카니발은 신속하게 문제를 해결하고 있다. 카니발은 채무 잔액을 1분기 350억 달러에서 3분기 310억 달러로 낮춰 두 분기 만에 40억 달러 가까이 상환했다. 연말이 되면 카니발은 300억 달러 이상으로 억제될 수도 있다.

4. 위험과 성장은 상부상조한다. 이 회사의 CEO 겸 회장 인 Joshua Weinstein은 최근 연료 가격의 급등에 대해 언급하면서 수익 증가가 최근 급등 한 연료 가격을 상쇄할 수 있다고 지적했다. 우리는 CEO의 언어 예술일 뿐이라는 또 다른 상반된 해석을 사용할 수도 있다. 그럼에도 불구하고 이 회사는 4분기 EBITDA 이익을 8억~9억 달러로 예상하고 있다. 총체적으로 말하면 더욱 엄격한 공인회계준칙(GAAP)으로 보더라도 순리윤은 여전히 변하지 말아야 하며 리윤능력은 2분기와 3분기 사이에 있어야 한다. 2024년의 경우 신규 생산능력이 제한돼 대부분의 재고가 매진돼 올해와 비교해 폭발적인 성장 가능성은 높지 않다.

文章鏈接 Hyperlink:https://www.carnivalcorp.com/news-releases/news-release-details/carnival-corporation-plc-reports-all-time-record-revenue-and

資料來源 Resource:CarnivalCorp

標籤 Label: Cruise Carnival CCL Debt NCLH RCL Fuel price