登錄

選單

登錄

海擇短評 Haize Comment:

時值Q4年末,主要國家的景氣持續下滑,而主要國家的動能會影響全球。雖說從銀行的消費數據看,旅遊業與餐飲業可能是弱經濟時期受衝擊較小的行業,不過覆巢之下無完卵,在旅遊/餐飲的細分行業中,優存劣敗會變得更嚴格,上市公司的本益比也會降低。

此前海擇觀點談過美國,我們在看美國時,考慮到美國是金融+軍工複合體的消費大國,更關心的是美國人在消費的可持續性,所以會更關注加息對美國政府"赤字施政"的影響,進而留意政府/企業/個人的利息支出、企業破產數的現況。

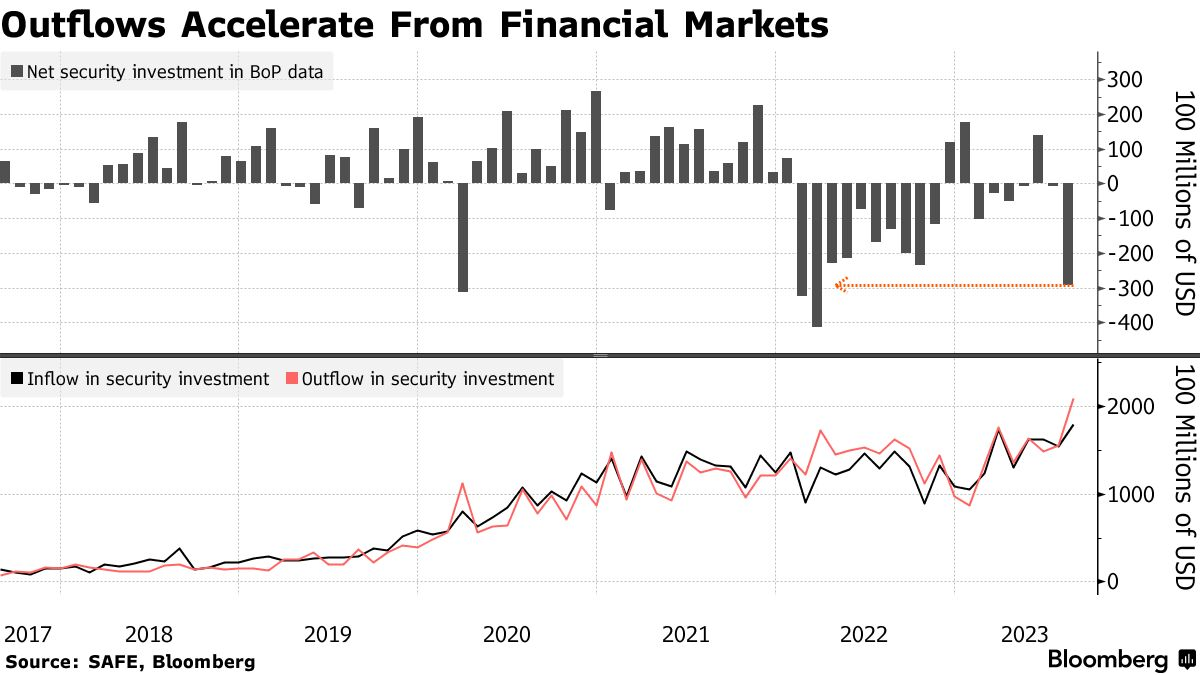

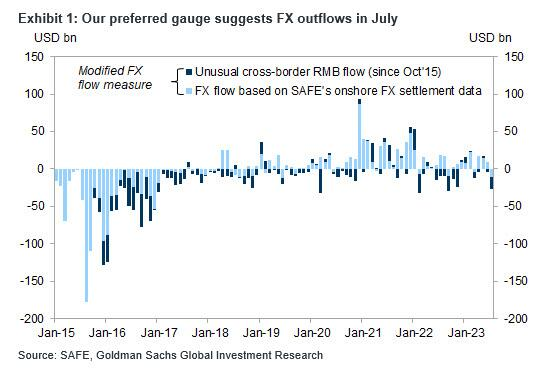

這次我們來談中國。中國是貿易大國,截至2022年底,是全球198個國家中128個國家的最大貿易夥伴(貿易夥伴的定義依進口貿易額+出口貿易額總值計算),貿易的可延展性與投資(特別是外資)息息相關,因此我們會更專注資本帳戶投資額的流入流出現況。美國數據固然每況愈下,但中國的數據也並不好。Bloomberg依照美國國家外匯管理局(SAFE, The State Administration of Foreign Exchange)統計,給到了一些值得注意的公開數據:

1. 7月中國資本外流達490億美金,創2023年以來新高點。

2. 8月債市資本淨流出近300億美金,創2022年3月以來新高點。

3. 8月股市資本淨流出超150億美金,創2022年6月以來新高點。

4. 8月外資直接投資外流160億美金,創2016年3月以來新高點。

5. 8月服務貿易逆差約130億美金,創2020年2月以來新高點。

創新低不代表無力翻轉,目前看來中國9月的數據有所回溫,8月是長期底部還是短期底部,則需要再觀察。可以確定的是,雖然疫情已過,但全球發展未見坦途;中美經濟陷於低谷,加諸兩國原有的地緣政治風險未停,城門失火殃及池魚,第三地被兩國爭端延燒的可能性不低,2024應仍是險中求存的一年。

----------

As we approach the end of Q4, major countries are experiencing a continuous economic downturn, and the momentum of these nations can influence the globe. Consumer data from banks suggest that the travel and catering industries might be less impacted during a weak economic period, but 'When the nest is overturned, no egg remains unbroken'. Within the sub-sectors of travel and dining, competition is getting stricter, and the price-to-earnings ratios of listed companies will also decrease.

Haize Capital mentioned the scenario of US earlier, we take into account that it is a large consumer nation of financial and military-industrial complexes. What concerns us more is the sustainability of American consumption, hence more attention is given to the impact of interest rate hikes on the U.S. government's "deficit governance", and consequently, attention is paid to the interest expenditures of government/corporations/individuals and the current situation of corporate bankruptcies.

This time let's talk about China, a major trading nation. As of the end of 2022, it is the largest trading partner(calculated by the total value of import and export trade volumes) for 128 out of 198 countries worldwide. The trade malleability and investments (especially foreign money) are closely related, so we pay more attention to the inflow and outflow of investment amounts. While the data from the United States is increasingly worrisome, China's data is also not positive. Based on statistics from the State Administration of Foreign Exchange (SAFE), Bloomberg has provided some noteworthy public data:

1. "In July, China's capital outflow reached 49 billion USD, hitting a new high since 2023."

2. "In August, the net outflow from the bond market was nearly 30 billion USD, marking a new high since March 2022."

3. "In August, the net outflow from the stock market exceeded 15 billion USD, reaching a new peak since June 2022."

4. "In August, the outflow of foreign direct investment was 16 billion USD, hitting a new high since March 2016."

5. "In August, the trade deficit in services was approximately 13 billion USD, setting a new record since February 2020."

Reaching a new low does not mean incapable of rebounding. At present, it seems that China's data for September has warmed slightly. Whether August represents a long-term or short-term bottom requires further observation. What can be affirmed is that, although the pandemic has passed, a smooth path for global development is not yet visible; the economies of both China and the United States are mired in a trough, and with the pre-existing geopolitical risks of the two countries not ceasing, the likelihood that third places will be embroiled in their disputes is not low. 2024 is still likely to be a year of seeking survival amidst dangers.

----------

4분기 말 현재 주요 국가들은 지속적인 경기 침체를 겪고 있으며 이들 국가의 경기 추세는 전 세계에 영향을 미칠 수 있다. 은행의 소비자 데이터에 따르면 경기 침체기에 여행업과 요식업이 받을 수 있는 영향은 비교적 적다. 그러나 "복소지하무완란(覆巢之下無完卵)", 여행, 음식 등 세분화된 업종내에서 경쟁이 날로 치렬해지고 있으며 상장회사의 시장수익률도 내려갈 것이다.

하이저 캐피털은 앞서 미국의 상황을 언급했다. 금융 및 군사 산업 복합체의 대형 소비국이라는 점을 고려하여, 우리는 미국 소비의 지속 가능성에 관심을 가지고 있으며, 이로부터 금리 인상이 미국 정부의 "적자 시정"에 미치는 영향에 더욱 관심을 기울임으로써 정부/기업/개인의 이자 지출과 기업 파산의 현황에 더욱 관심을 기울인다.

이번에는 주요 무역 국가인 중국에 대해 이야기해 본다. 2022년 말 현재 전 세계 198개국 중 중국은 128개국의 최대 무역 파트너(수출입 무역 총액 기준)다. 무역 확장성과 투자(특히 외자)는 밀접한 관련이 있기 때문에 우리는 투자 금액의 유입과 유출에 더욱 관심을 기울인다. 미국의 수치가 갈수록 우려되고 있지만 중국의 수치도 낙관적이지 않다. 미국 국가외환관리국(SAFE)의 통계에 따르면 블룸버그 통신은 몇 가지 주목할 만한 공개 데이터를 제공했다.

1. 7월 중국 자본 유출은 490억 달러로 2023년 이후 최고치를 기록했다.

2. 8월 채권시장 자본 순유출은 거의 300억 달러로 2022년 3월 이후 최고치를 기록했다.

3. 8월 증시 자본 순유출은 150억 달러를 넘어 2022년 6월 이후 최고치를 기록했다.

4. 8월 외국인 직접투자는 160억 달러가 유출되어 2016년 3월 이후 최고치를 기록했다.

5. 8월 서비스 무역 적자는 약 130억 달러로 2020년 2월 이후 최고치를 기록했다.

자본이 대량으로 유출된다고 해서 반등할 능력이 없는 것은 아니다. 현재로서는 중국의 9월 수치가 약간 회복된 것 같다. 8월이 장기 바닥을 대표하는지, 단기 바닥을 대표하는지는 더 지켜봐야 한다. 분명한 것은 코로나가 지나갔지만 세계 경제 발전이 순탄하지 않다는 점이다. 중미 양국 경제가 모두 바닥을 치고 양국의 지연정치학적 위험이 지속되고 있어 제3국이 양국 분쟁에 휘말릴 가능성이 낮지 않다. 2024년은 여전히 위험 속에서 생존을 모색하는 한 해가 될 것이다.

文章鏈接 Hyperlink:https://www.bloomberg.com/news/articles/2023-09-19/china-s-worst-capital-outflow-in-years-spells-more-yuan-pressure

資料來源 Resource:Bloomberg

標籤 Label: China Capital Outflow 2024