登錄

選單

登錄

海擇短評 Haize Comment:

美團(HK: 3690)近期公告2023Q3財報,公司在各項財務收入與運營相關指標,大體仍能創下新高,但成本與費用的增速高於收入增速,則影響了盈利能力,可以看出似有威脅潛伏之感。財報後美團市值從低點下挫,創下2020年4月以來新低,看來更像是部分投資人對美團的定位從成長股改變為價值股。海擇資本的部分觀察與思考如下:

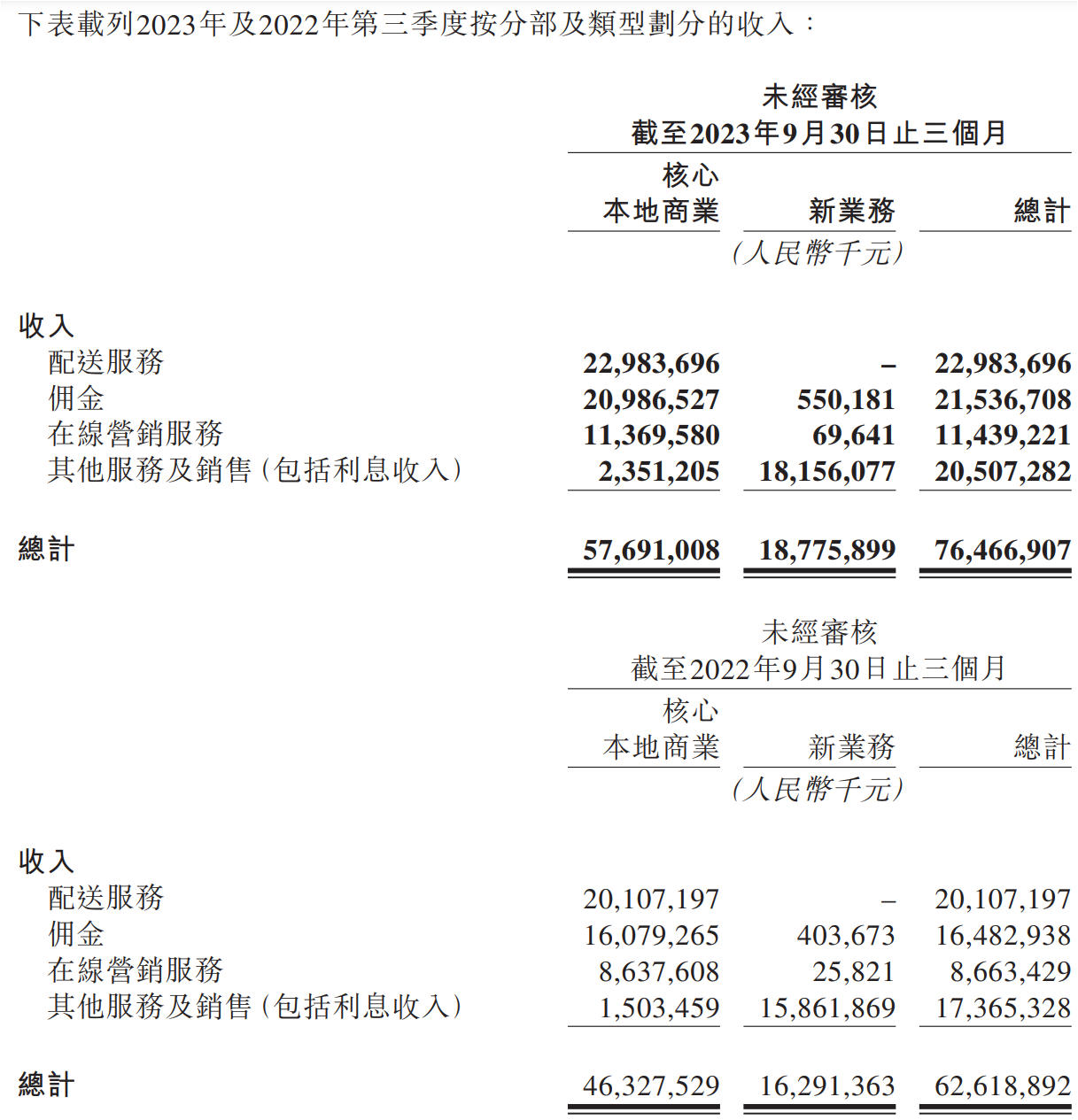

1. 收入增長依舊強勁:美團Q3總收入為765億人民幣,QoQ增長13%,YoY增長22%;Adjusted EBITDA為57億人民幣, QoQ降低19%,YoY增長29%。雖然財務上EBITDA出現季減,但是運營指標仍然很不錯,公司的年度交易用戶數、年度活躍商家數、用戶購買頻次均創歷史新高;現金流仍處於穩健狀態,現金與約當現金總額達1,336億人民幣。

2. 抖音威脅潛伏:從美團季度超過100億美金量級的收入,各產品線的收入仍能維持兩位數的成長動能,已屬難能可貴。核心本地商務部份,本季收入577億人民幣,QoQ增長13%,YoY增長25%;新業務部分為188億人民幣, QoQ增長13%,YoY增長16%。而從各細分產品線來看,Q3餐飲外賣單日訂單量峰值達7,800萬單,美團閃購的單日峰值達1,300萬單,都創歷史新高,規模上也可觀。值得注意的是,本季美團的多個產品線在直播上也做了投入,比如餐飲相關的"神搶手"活動、酒旅事業的直播促銷,既培養消費者在美團觀看直播的習慣,也協助供應商品牌露出,公司公告的數據是-直播對話量增長3倍。但這也意味著抖音必定侵蝕了美團部分產品線的邊界,美團並沒有透露在直播的投入金額及抖音對定價/訂單的影響,但可以參考的是,Q3核心本地商務部份收入QoQ增長13%,而對應的成本及費用則QoQ增長19%,超過收入增長。

3. 酒旅或有潛在衝擊:海擇資本觀察到,近期抖音的住宿產品,在不同價位都有一批獨佔式的低價產品,其中不乏高星連鎖酒店品牌。雖然抖音僅從價格層面獲取市場,相對全中國數十萬家酒店數,其覆蓋的佔比也極小,但這表示其流量已能讓酒店願意冒著攜程(NASDAQ: TCOM)、美團雙強禁流的風險與之合作,不無可能在紅海中殺出一條血路。面對競爭,攜程能用國際化(Trip.com)分散風險,美團的版圖看來似乎更容易被抖音侵蝕,後續板塊變動值得觀察。

4. 估值可能面臨重修:本季財報公告後四天,美團市值從6,781億港幣(約868億美元)下挫至5,488億港幣(約702億美元),跌幅約19%,董事會也公告授權以10億美元回購股票。其實美團的盈利能力與運營效率仍執中國牛耳,但投資人拋售導致的市值崩壞,可能意味著部份投資人已逐漸將其視為價值型公司,而非成長型公司。

----------

Meituan (HK: 3690) reported its financial results for Q3 2023. The company generally reached new highs in various financial and operational metrics. However, the growth of costs and expenses exceeded that of revenue, impacting its profitability and suggesting an underlying threat to its financial stability. Following the financial report, Meituan's market value fell from its low point, reaching a new low since April 2020. It appears that investors are starting to view the company as a value stock rather than a growth stock.

1. Strong Revenue Growth: Meituan's total revenue for Q3 was 76.5 billion RMB, a 13% increase quarter-over-quarter (QoQ) and a 22% increase year-over-year (YoY). The Adjusted EBITDA was 5.7 billion RMB, a 19% decrease QoQ but a 29% increase YoY. Despite a QoQ decrease in EBITDA, operational metrics remained strong. The company's annual number of transaction users, annual active merchants, and user purchase frequency all reached historic highs. Cash flow remained robust, with cash and cash equivalents totaling 133.6 billion RMB.

2. Hidden Threat from Douyin: Meituan's revenue exceeding 10 billion USD for the quarter, with each product line maintaining double-digit growth momentum, is commendable. The core local commerce segment generated revenue of 57.7 billion RMB, increasing 13% QoQ and 25% YoY. The new business segment brought in 18.8 billion RMB, up 13% QoQ and 16% YoY. Notably, Meituan invested in several product lines for live streaming this quarter, such as the "ShenQiangShou" event for catering and live stream promotions for its hotel and travel business. The company announced that dialogue volume in live streams increased threefold. However, this also implies that Douyin has encroached on some of Meituan's market share. Meituan has not disclosed the investment amount in live streaming and the impact of Douyin on pricing/orders. But it's worth noting that Q3's core local commerce revenue increased 13%, while the corresponding costs and expenses for this segment increased by 19%, surpassing the revenue growth.

3. Potential Impact on Hotel and Travel Segment: Haize Capital observed that recently, Douyin's accommodation products include a range of uniquely priced low-cost offerings, featuring high-star chain hotel brands. Although Douyin currently captures market share primarily through pricing and its coverage is relatively small compared to China's tens of thousands of hotels, its traffic made hotels willing to risk offending major players like Ctrip (NASDAQ: TCOM) and Meituan. This suggests Douyin could carve a niche in the competitive market. In response to this competition, Ctrip can leverage its international platform (Trip.com) to diversify risks. However, Meituan's domain appears more susceptible to encroachment by Douyin, making the future dynamics of this segment worth monitoring.

4. Valuation May Undergo Revision: Following the announcement of this quarter's financial report, Meituan's market value plummeted from 678.1 billion Hong Kong dollars (approximately 86.8 billion USD) to 548.8 billion Hong Kong dollars (approximately 70.2 billion USD) in just four days, a drop of about 19%. The board of directors announced the authorization of a 1 billion USD stock buyback. Despite Meituan still holding a strong position in terms of profitability and operational efficiency in China, the sell-off by investors leading to this market value collapse could indicate that some investors are starting to see it more as a value company rather than a growth company.

----------

메이퇀(HK: 3690)은 2023년 3분기 재무실적을 발표했다. 이 회사는 각종 재무와 운영 지표에서 전반적으로 최고치를 기록했다. 그러나 원가와 비용의 증가는 수익의 증가를 초과하고 수익성에 영향을 미치며 재정적 안정에 잠재적 위협이 된다. 실적 발표 후 메이퇀의 시가총액은 저점에서 하락해 2020년 4월 이후 최저치를 기록했다. 투자자들은 이 회사를 성장주가 아닌 가치주로 보기 시작한 것 같다.

1. 영업수익 성장 강력: 메이퇀의 3분기 총 영업수익은 765억 위안으로 분기 대비 13%, 전년 동기 대비 22% 증가했다. Adjusted EBITDA는 57억 위안으로 분기 대비 19%, 전년 동기 대비 29% 증가했다. EBITDA의 분기 대비 감소에도 불구하고 운영 지표는 여전히 강하다. 회사의 연간 거래 사용자 수, 연간 활성 상인, 사용자 구매 빈도는 모두 사상 최고치를 기록했다. 현금 흐름은 안정세를 유지하고 있으며, 현금 및 현금 등가물 총액은 1,336억 위안이다.

2. 더우인(抖音)의 경쟁 위협: 메이퇀의 이번 분기 영업수익은 100억 달러를 돌파했고, 각 제품 라인은 두 자릿수 성장세를 유지하고 있어 칭찬할 만하다. 핵심적인 현지 상업은 577억 위안의 수익을 창출하여 분기 대비 13%, 전년 동기 대비 25% 증가했다. 새로운 업무로 인한 수익은 188억 위안으로 분기 대비 13%, 전년 동기 대비 16% 증가했다. 세분화된 제품 라인별로 보면 3분기 음식 배달 하루 주문량 최고치는 7,800만 건, '메이퇀플래시 구매'의 하루 최고치는 1,300만 건으로 모두 사상 최고치를 기록했으며 규모도 상당했다. 주목할 만한 것은 메이퇀이 이번 분기에 몇 개의 생방송 제품 라인에 투자했는데, 예를 들면 음식의 "ShenQiangShou"활동 및 호텔과 관광 업무의 생방송 판촉이다. 이 회사는 생방송 중 대화량이 3배 증가했다고 발표했다. 그러나 이는 더우인이 이미 메이퇀의 일부 시장 점유율을 침범했다는 것을 의미한다. 메이퇀은 생방송 분야에 대한 투자 금액과 더우인이 가격/주문에 미치는 영향을 공개하지 않았다. 그러나 3분기 핵심 로컬 비즈니스 영업수익은 13% 증가한 반면 그에 상응하는 원가와 비용은 19% 증가해 수익 증가를 앞질렀다는 점에 주목할 필요가 있다.

3. 호텔과 관광 세분화 시장에 대한 잠재적 영향: 하이저 캐피털은 최근 더우인의 숙박 상품이 다양한 가격대에서 일련의 독특한 저가 제품이 있으며, 그 중에는 심지어 고성급 호텔 체인 브랜드도 있다는 것을 관찰했다. 더우인은 현재 주로 가격 책정을 통해 시장 점유율을 얻고 있지만, 중국의 수만 개 호텔에 비해 상대적으로 커버리지가 작다. 그러나 더우인의 트래픽은 호텔들로 하여금 씨트립(NASDAQ: TCOM)과 메이퇀과 같은 주요 경쟁사들을 미워할 위험을 무릅쓰고 더우인과 협력하게 했다. 이는 더우인이 경쟁이 치열한 시장에서 한 자리를 차지할 수 있음을 보여준다. 이에 대응하기 위해 씨트립은 글로벌 플랫폼(Trip.com)을 활용해 리스크를 분산할 수 있다. 하지만 메이퇀의 기존 시장은 더우인의 경쟁 위협에 더 취약해 보인다. 이것은 이 분야의 미래 동태를 주목할 만하게 한다.

4. 시가평가 조정 가능성: 이번 분기 실적 발표 후 메이퇀의 시가총액은 불과 4일 만에 6,781억 홍콩달러(약 868억 달러)에서 5,488억 홍콩달러(약 702억 달러)로 약 19% 폭락했다. 이사회는 10억 달러의 주식 환매 권한을 부여한다고 발표했다. 비록 메이퇀이 중국의 수익성과 운영 효율 면에서 여전히 강세를 보이고 있지만, 투자자들의 매도로 시가총액이 폭락한 것은 일부 투자자들이 이를 성장형 회사가 아니라 가치 회사로 더 많이 보기 시작했다는 것을 보여줄 수 있다.

文章鏈接 Hyperlink:https://www.meituan.com/en-US/investor-relations

資料來源 Resource:Meituan

標籤 Label: Meituan HK: 3690 Douyin ByteDance Travel Hotel